Bank-issued credit cards, owned by nearly 200 million individuals in the United States, have become an essential financial tool amid inflation and rising costs, providing relief to households navigating a challenging economic environment.

“Credit Card Use During Economic Turbulence,” a PYMNTS Intelligence and Elan collaboration, used insights gathered from a survey of over 2,200 U.S. consumers to identify patterns related to the spike in credit card use, the reasons consumers choose certain card features, and how higher inflation has influenced this behavior.

Findings detailed in the report showed that one-third of cardholders increased their credit card spending in the six months before the study. The surge can be linked to inflation and escalating expenses, which are driving consumers to rely on credit cards to meet their financial needs.

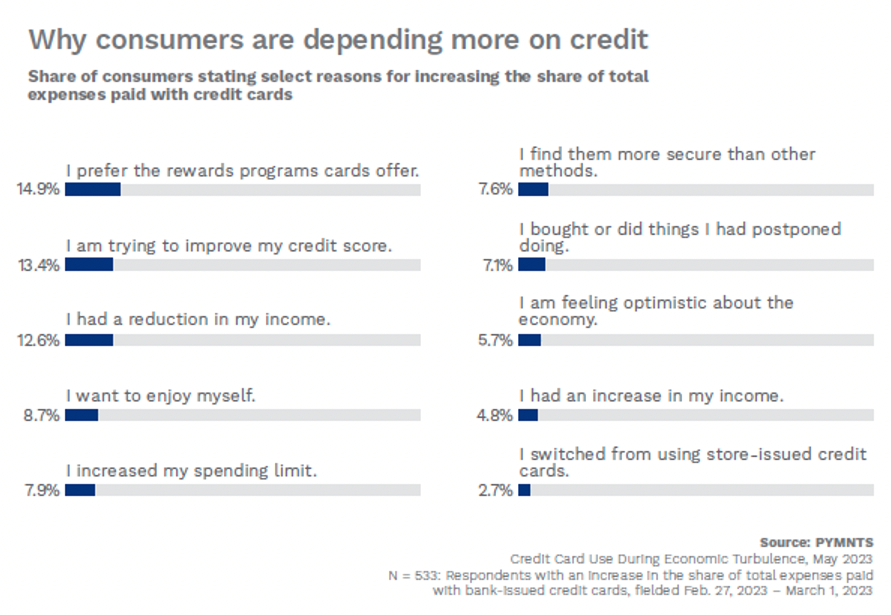

Among the primary factors behind the increase were credit card rewards programs, cited by 15% of cardholders, which suggests that consumers are actively seeking value-added features that can enhance their financial situation and help them better manage their finances. Following were efforts to improve credit scores and a decrease in income, both cited by 13% of cardholders as top drivers behind the increased reliance on credit cards.

Specifically, among consumers impacted by inflation, PYMNTS Intelligence found that a decline in income emerged as the top reason driving their increased use of credit cards.

“Similarly, consumers who revolve their balances — both high- and low-spending revolvers — were much more likely than non-revolvers to cite reduced income as the top reason for increasing their credit card spending,” the study found.

The study’s findings also shed light on the various payment habits and preferences among different cardholder types. Low-income consumers were more likely to carry balances, while high-income cardholders were less likely to do so. Additionally, younger generations were found to be more inclined toward increasing their reliance on credit cards compared to older generations.

The study underscored the increasing dependence on credit card spending among consumers as inflation continues to impact their purchasing power. With rewards and cash-back programs playing a role in driving this trend, credit card issuers should prioritize providing value-added features that can attract and retain customers in an increasingly competitive market.

These customers include boomers and seniors, who do not necessarily rely on credit cards due to financial hardships but instead are drawn to the benefits of rewards programs (as confirmed by 7 in 10 respondents), separate PYMNTS Intelligence research showed. This contrasts with younger individuals who primarily use credit to help manage their expenses.

Moreover, this older demographic, half of whom own more than two cards that they use interchangeably, spends less and promptly clears their balances as soon as possible. Their approach reflects a spending-conscious and practical mindset, one that leverages multiple cards to control spending and maximize rewards.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More