Once card holders are made aware of how they can earn rewards by using their credit and debit cards to pay for goods and services, most are hooked.

That’s according to the PYMNTS Intelligence report “Card-Linked Offer Growth Hinges on First-Time Users,” which was based on surveys with more than 2,100 consumers. It also found that after using card-linked offers, 93% of card holders plan to come back for more, maintaining or increasing their card activity in the months to come.

The trick is educating card holders about the card-linked incentive programs, how to use them and what they can earn. Getting the uninitiated consumer up to speed on card-linked offers in the first place is key. Seventy-three percent of nonusers said they are not at all or only slightly familiar with card-linked offer programs.

Consumers require a certain level of familiarity with the concept of card-linked rewards and customized deals to be attracted to the concept. There are holdouts, however, who said they have their reasons for not taking advantage of card-linked rewards — and they are especially prominent among consumers in the low- and middle-income brackets.

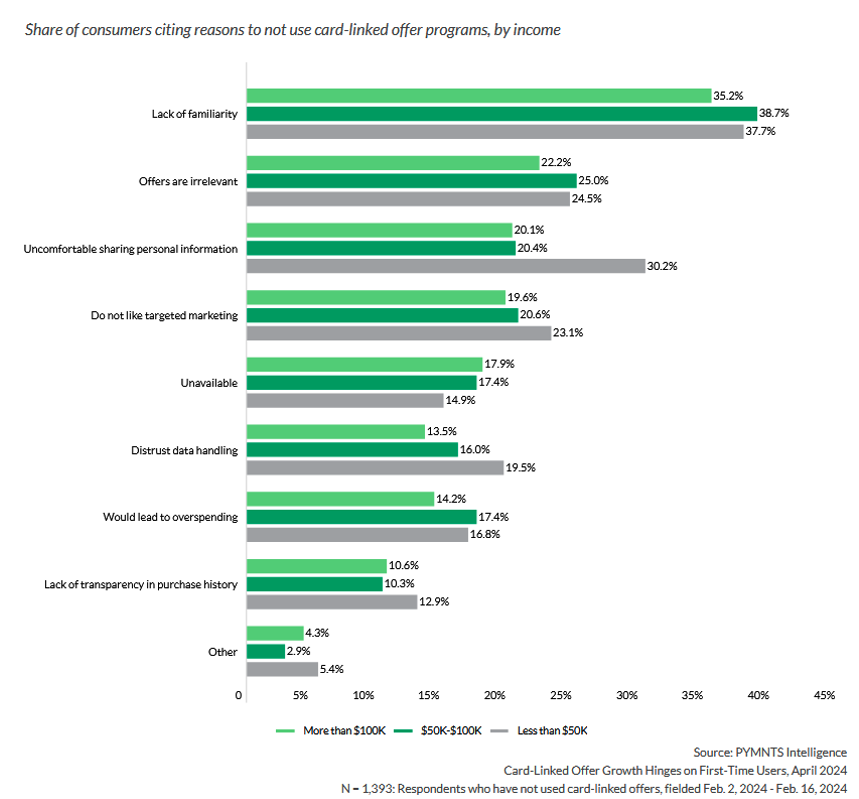

As PYMNTS Intelligence data not included in the original report showed, those reasons vary and appear shaped by income levels.

As PYMNTS Intelligence data not included in the original report showed, those reasons vary and appear shaped by income levels.

A lack of familiarity with the reward programs among card users is the top reason consumers have not taken advantage of card-linked offers, with 39% of middle-income card users (those earning between $50,000 and $100,000 annually), 38% of low-income respondents (those earning less than $50,000 annually) and 35% of high-income earners (those earning more than $100,000 annually) saying they simply didn’t know about the programs.

Thirty percent of low-income earners also take a pass on card-linked offers because they are uncomfortable sharing their personal information, while 23% of the same group said they don’t like the target marketing behind the offers. Nearly 20% of the same segment also distrust how their personal data might be used if they sign up for rewards programs.

Seventeen percent of middle-income and low-income consumers, meanwhile, decline special offers out of concerns that doing so might lead to overspending.

These findings highlight a key pattern, as card issuers or offer providers could address nearly every one of these concerns through customer education efforts aimed at broadening awareness and putting people’s minds at ease.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More