Today, that major market validation got both deeper and broader. The Montreal-based contactless payments platform announced that its Samsung Venture Investment Corporation has officially joined the round, bringing its total to roughly $20 million.

Maxime de Nanclas, co-CEO and co-founder of Mobeewave, told Karen Webster that this news is another example of Samsung’s investments in innovators, with new tech capable of disrupting existing players.

“We think that supporting new types of services like Mobeewave can be a key differentiator for Samsung, by giving consumers and merchants a new way to pay and be paid, using the one device that is now an inseparable part of their life: their smartphone,” Nanclas remarked. “Just like they did when they acquired LoopPay in 2015 to jumpstart Samsung Pay.”

What Samsung’s Scale Unlocks

Samsung sells more handsets than any other OEM worldwide, with a little under a third of the share of the global handset market; it is second in the North American market, with roughly a 25 percent share. All told, there are more than 900 million Samsung phones in the market.

That’s a massive amount of reach, as well as a massive amount of untapped capacity to use those handsets, and Mobeewave technology, to redefine the mPOS market, du Haÿs noted.

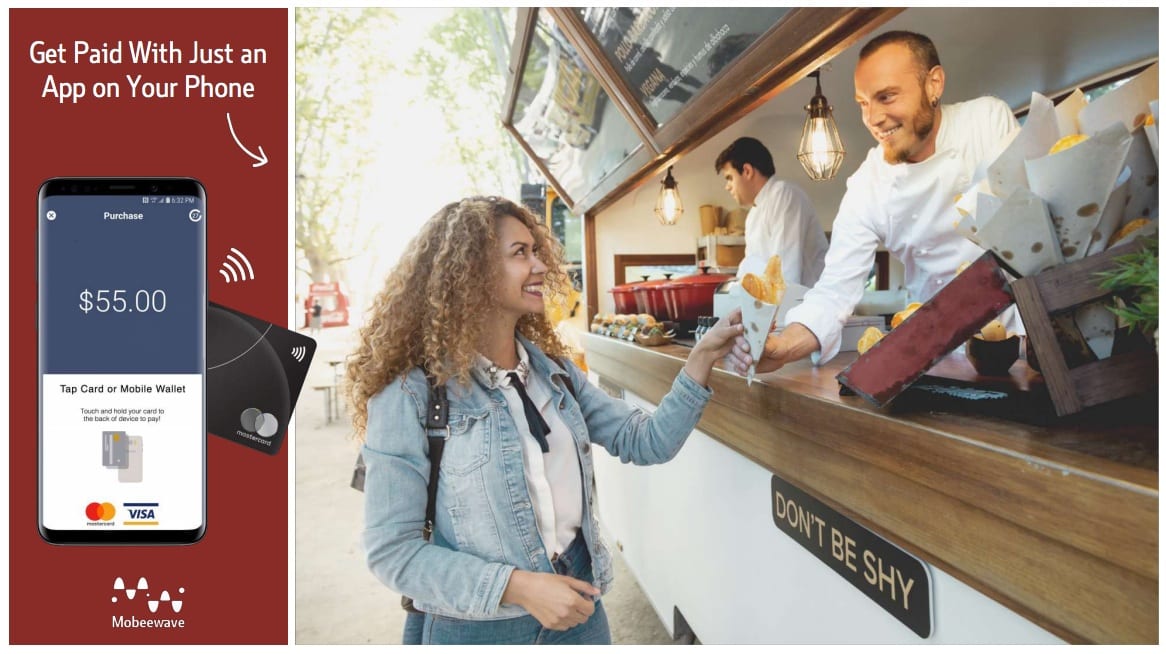

Turning handsets with NFC chips into a contactless point-of-sale device will disrupt mPOS as we know it, he pointed out, by using software and the contactless cards that consumers have today in their physical and mobile wallets to ignite a new mobile POS experience for consumers and merchants.

And du Haÿs added that Mobeewave’s seven-year skate to where the mobile payments innovation puck is going has the potential to unlock an entirely new revenue model for Samsung, by jumpstarting this new, software-based mPOS payments ecosystem.

Nanclas emphasized that the use cases for testing this hypothesis are limited only by one’s imagination, and by the capacity to scale – something that he said Samsung and Mobeewave are now well-positioned to explore together.

For instance, consumers who want to split the check or give a tip to their hairdresser need only produce a card and tap the receiver’s phone. Micro merchants who want to grow their sales by ditching cash for digital can more easily do that – all they will need is their own phone and a consumer with a contactless card.

Perhaps most compelling, du Haÿs remarked, are the charity use cases, in which fundraisers of all kinds can more easily operate in a world in which cash is an increasingly scarce and inaccessible resource, and where cards and mobile devices capable of enabling an NFC transaction are prevalent.

Tapping Into the Changing Market

Mobeewave’s last fundraising round was in early 2015, according to its co-founders – four years ago in real time, but two centuries ago in tech time. Then, it seemed like it might be forever until the contactless card market would catch up with them, particularly in the U.S.

Part of that slow roll to contactless, du Haÿs noted, is that the U.S. bet a lot of the contactless payments farm on mobile wallets. Those may have been the “pet project” for a lot of industry players for the last four years or so, but mobile wallets flatlined after an initial flurry of activity from the earliest of early adopters. Mobile contactless didn’t end up igniting contactless in the U.S. – and didn’t even get remotely close.

“People don’t need to use their phones to pay for things [in the store],” Nanclas added. “They have plastic cards, and they are actually fine with using them. They are happy to use them.”

But every merchant or person, for that matter, needs a way to accept a payment, he noted. What’s more, there are “a lot of merchants who don’t consider themselves merchants today because they can only take cash payments.”

Using the smartphone as a one-stop shop solves for those merchants, he said. And, he added, with the recent big advances in contactless card issuance announced in the U.S. – like Chase’s choice to transition its entire Visa portfolio to contactless – there is a lot more movement in the market, and many more places where the ability to tap a contactless card will become a highly relevant payment transacting capability.

It’s already happening in markets around the world, Nanclas pointed out.

In Canada, for example, the number of contactless transactions jumped to 3.2 billion – worth $104 billion total – a 55 percent increase over the previous year in terms of both volume and value. Additionally, contactless grew to account for about 29 percent of all POS card payments in Canada in 2017, up from 7 percent in 2014. Canadian consumers seem to prefer using contactless at grocery stores, pharmacies, gas stations, coffees shops and QSRs. Mobile contactless cards have also seen much faster uptake among Canadians than mobile wallets, which have only been used by 4 percent of consumers.

Meanwhile, in the U.K., according to Worldpay, 52 percent of in-store card transactions were contactless as of July 2018, increasing by about 30 percent between 2017 and 2018. That growth came despite the £30 cap on contactless.

For Mobeewave, that means that the pace to win this new mPOS race will only get faster. As Nanclas and du Haÿs told Webster, the focus going forward will be about excellence in execution, with the Mobeewave team committed to running faster than everyone else, so they can capitalize on the opportunity that sits at the intersection of contactless cards, software and handset innovation.

Momentum is key now, they emphasized, since without it all of the money and all of team efforts won’t much matter.

That, said du Haÿs, should have the incumbent players who took “30 years to get 60 million terminals” into the market more than a bit nervous. With Samsung, he said, Mobeewave can turn on hundreds of millions of smartphones as terminals in a fraction of the time.

At least, that’s the plan.

“The devices that are emerging and the U.S. coming online with contactless cards is going to make a big, big difference in how mobile point of sale will be defined going forward, and how people and businesses will think about it,” he said. “It will be a very different dynamic, and we are pleased to be part of that transition.”