The drumbeat of recent announcements shows more merchants lining up to offer pay-by-bank options.

But it will be consumers who provide the momentum — and much depends on how comfortable they are with having funds pulled straight from their accounts.

In terms of the pay-by-bank mechanics (and we’re using the term interchangeably with account-to-account transactions), funds flow directly between bank accounts, without credit or debit cards in the mix.

Account-to-account (A2A) payments functionality has been firmly in place around the globe, evident in Canada with Interac Online and in Brazil with PIX.

For the merchants, there’s the opportunity to avoid interchange fees that are a hallmark of card transactions (which of course leads to lost revenues for the card-issuing banks).

As to the groundswell as retailers embrace pay-by-bank:

Earlier this year, we reported that retailers were actively seeking pay-by-bank functionality, as more than half said they would seek to partner and outsource the necessary “behind the scenes” technical flows to offer the payment option.

In an interview with PYMNTS, Craig McDonald, chief business officer at open banking FinTech Trustly, said that as faster payments and pay-by-bank options gain visibility, “any merchant is really trying to see how they can increase conversion and reduce their cost of payment acceptance.” Requests for payment, he said, are a particularly attractive option.

“In some cases, real-time rails will be fantastic, while in others, you’ll want to leverage the cost benefits of a debit network,” explained McDonald. “It’s why we believe that A2A represents a superior rail and delivers an optimal payment experience.”

More recently, and as detailed last week, JPMorgan Chase announced the availability of its Mastercard-powered pay-by-bank tool.

The offering, which combines Mastercard’s open banking technology and J.P. Morgan Payments’ ACH capabilities, lets merchants offer customers the ability to pay directly from their bank accounts. Mastercard’s Smart Payment Decisioning technology enables merchants to time transactions based on the bill payer’s transaction behavior and risk patterns, ensuring payments get made and reducing the risks of returns due to insufficient funds.

In another example, Link Money and Alternative Airlines partnered to allow customers to make payments directly from their bank accounts, integrating Link Money’s open banking payment platform into Alternative Airlines’ website.

Link Money CEO Eric Shoykhet has noted to PYMNTS separately that as the FedNow® Service and faster payments go more mainstream, we’ll see a rise in account-to-account or pay-by-bank payment options in the United States market.

The progression is a natural one, he said, noting that “in order to settle account-to-account or in a pay-by-bank context, the merchant needs to know that the customer has sufficient funds” in their accounts.

The company has built decisioning models that can guarantee the sufficiency of funds in accounts and real-time payments to the merchant, even though the payments themselves are carried over rails that aren’t instantaneous in nature.

The Comfort Factor

The fact remains, too, that as of this writing, the Federal Reserve is mulling a significant reduction in debit interchange fees, which in turn would make those transactions cheaper for merchants. Debit, then, is hardly going to go away.

The above announcements — and surely there will be more on the horizon — represent what might be the equivalent of a payments “field of dreams” moment: build it and they will come. But that’s no sure bet, given the fact that consumers are already quite comfortable with using debit as a means of, effectively, using funds on hand that are already lodged with their banks.

We note, too, that in Visa’s most recent earnings results, just this week (Oct. 24), the payments network detailed in its filings that debit payment volume growth outpaced that of credit. Debit grew 9% year on year, in constant dollars, while credit was up 8% as measured in the fiscal fourth quarter. Total cards grew 7%. But debit cards grew by 8% in the most recent quarter, handily outpacing the 4% growth in credit cards.

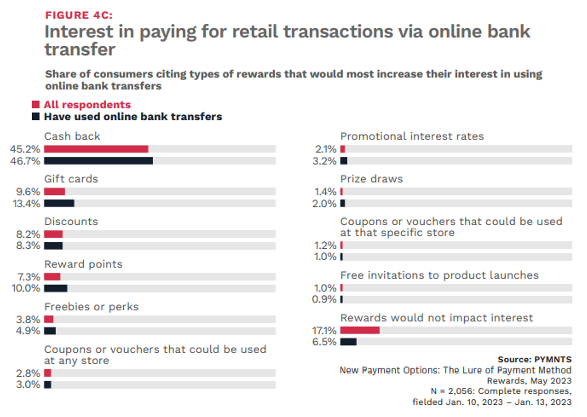

Rewards May Sweeten the Deal

PYMNTS Intelligence data found earlier this year that the uptake of pay-by-bank in retail and merchant-facing commerce may be especially desirable — for the consumers — when rewards are offered. In the report “New Payment Options: The Lure of Payment Method Rewards,” done in collaboration with Nuvei, one-quarter of consumers who tried online bank transfers, also known as pay by bank transfer, for the first time in the last year did so for a particular reason: they could earn reward points.

The accompanying chart notes the type of rewards that they’d like to get — and cash back tops the list.