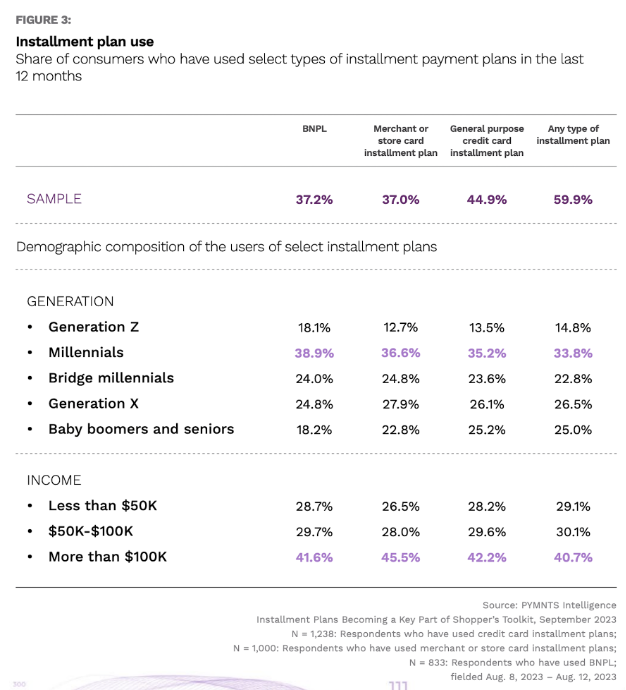

In recent years, split-pay options have gained popularity among consumers of all demographic groups looking for greater flexibility in managing their expenses. Among all consumer segments, the leading users of installment purchase plans are neither millennials nor lower-income earners but high-income consumers.

This applies for all forms of split-pay options, including those offered by general credit card issuers and buy now, pay later (BNPL) providers, although merchant and store cards are the preferred option for this cohort. This reality challenges the assumption that high-income or affluent consumers are averse to these types of credit products.

These are some of the key conclusions drawn from “Installment Plans Becoming a Key Part of Shopper’s Toolkit,” a PYMNTS Intelligence research study done in collaboration with Splitit that examines how consumers use installment plans.

According to the study, almost 46% of high-income earners — consumers making more than $100,000 annually — have used store card installment plans in the last 12 months prior to being surveyed, doing so an average of twice during that period.

High-income earners typically consider using this credit option for amounts above $2,000, regardless the type of product they want, including home furnishings, consumer electronics or even hotel expenses.

The intense usage of store card installment plans by affluent consumers is in line with their credit card penetration. Another PYMNTS Intelligence report, “New Reality Check: The Credit Card Use Deep Dive Edition,” has found that high-income earners in the U.S. hold 2.9 credit cards on average; for low-income earners, the average is 1.8 cards, and 2.5 cards are averaged for those in the mid-income bucket. The study also revealed that, unlike individuals living in financial difficulties, affluent consumers primarily focus on the benefits they can get from different reward programs when choosing to use a credit program.

The high level of adoption among affluent consumers could well be sticky, as 78% of consumers who have used store card installment plans have been very satisfied with the experience, and 42% say that they are likely to use one in the next 12 months.

The high use of split-pay options by consumers with high incomes is reshaping consumer behavior and presenting a lucrative opportunity for merchants. By adapting their offerings to meet these consumers’ preferences, merchants can capitalize on this trend and foster customer loyalty.