In today’s challenging economic environment, understanding how consumers use credit cards is important.

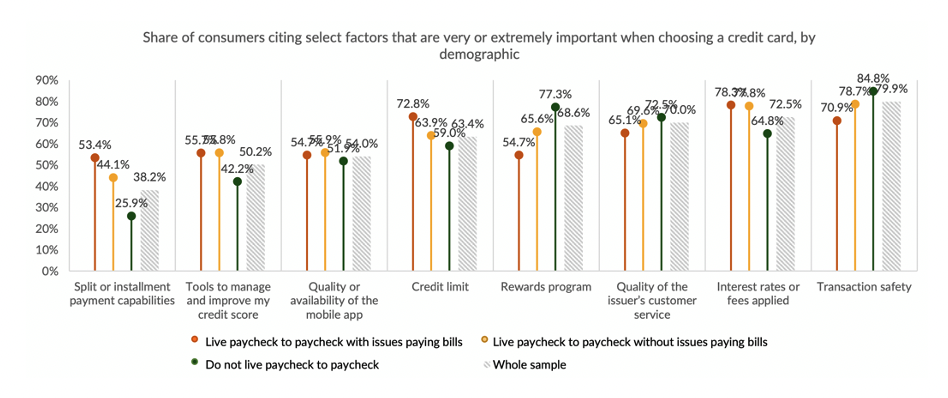

While struggling consumers tend to use credit cards to better manage their cash and personal finances, consumers living in a healthier financial situation value more security and rewards options. These more affluent consumers use credit cards as another payment method. To be more precise, 77% of consumers who do not live paycheck to paycheck chose their credit cards because of the benefits of rewards programs, while 85% did so for security reasons.

These are some of the findings detailed in the PYMNTS Intelligence report “The Credit Card Use Deep Dive Edition: Nearly Two-Thirds of Struggling Consumers Revolve Credit Card Balances.” The report examined the financial lifestyles of U.S. consumers and explored how they use credit cards to manage their cash flows.

Nearly 43% of credit cards are held by consumers not living paycheck to paycheck, according to the study. This consumer cohort values different aspects when choosing credit cards than consumers with difficulties making ends meet.

Amber Carroll, senior vice president of membership and lifecycle at LendingClub, told PYMNTS in an interview posted in December that consumers who are not living paycheck to paycheck focus more on rewards and may not take advantage of flexible repayment programs as frequently as struggling consumers do.

By contrast, struggling paycheck-to-paycheck consumers are more likely to cite interest rates and credit limits as important reasons when choosing a credit card. This consumer segment holds 57% of all credit cards in the U.S.

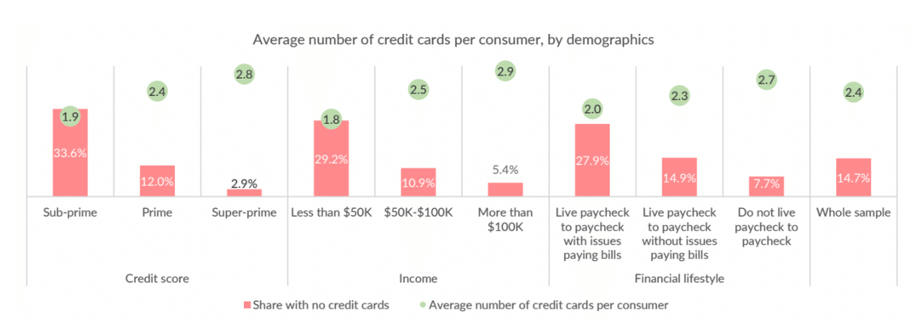

The study also revealed an apparent inverse correlation between financial distress and possession of credit cards. Consumers with more difficulties making ends meet or with a worse credit score hold fewer credit cards than those who live in a healthier financial situation or those who have higher credit scores.

Nearly 92% of consumers not living paycheck to paycheck hold a credit card, versus 73% of those living paycheck to paycheck with issues paying bills. On average, the former group holds 2.7 credit cards, in comparison to 2 for the latter.

Struggling consumers hold fewer credit cards and turn to them not only for daily purchases but also to cover emergency expenses by paying in installments. In this sense, higher interest rates may impact them more.

“It will be really important to look at what happens with interest rates over the months ahead,” Carroll told PYMNTS. “An interest rate cut could mean lower monthly payments. And that’s a trend that will certainly help those who are living paycheck to paycheck and using the revolving capabilities on credit cards.”