Pay-by-bank payments, also known as account-to-account (A2A) payments, allow consumers to transfer funds between bank accounts in real time. These payments bypass traditional card networks and utilize intermediaries like peer-to-peer (P2P) service providers such as Venmo or PayPal.

One of the main benefits of A2A payments is their simplicity. They eliminate the need for users to share sensitive financial information, reducing the risk of fraud. Additionally, A2A payments are typically processed in real time, providing immediate funds to merchants and improving cash flow.

While these payments have been gaining traction, with 84% of users reporting being very or extremely satisfied with their most-used A2A payment platform, they have yet to fully disrupt the wider payments landscape, according to findings detailed in “Tracking the Digital Payments Takeover: Consumer Familiarity Controls Account-to-Account Payment Growth,” a PYMNTS Intelligence and AWS collaboration.

A key factor contributing to the sluggish adoption is a significant knowledge gap among consumers. More than half of the respondents acknowledged abstaining from A2A options solely due to their lack of understanding. Moreover, 24% of consumers were unaware that A2A payments were even possible, highlighting the need for comprehensive awareness campaigns to enlighten consumers about the advantages of A2A payments.

Generational preferences also play a significant role in the adoption of A2A payments. Millennials, who are more inclined to use digital platforms like PayPal and Venmo, are at the forefront of A2A adoption. On the other hand, older consumers, particularly baby boomers and seniors, show the least interest in utilizing A2A payments. And two-thirds of Gen Z consumers admit to being unaware that they could make pay-by-bank payments.

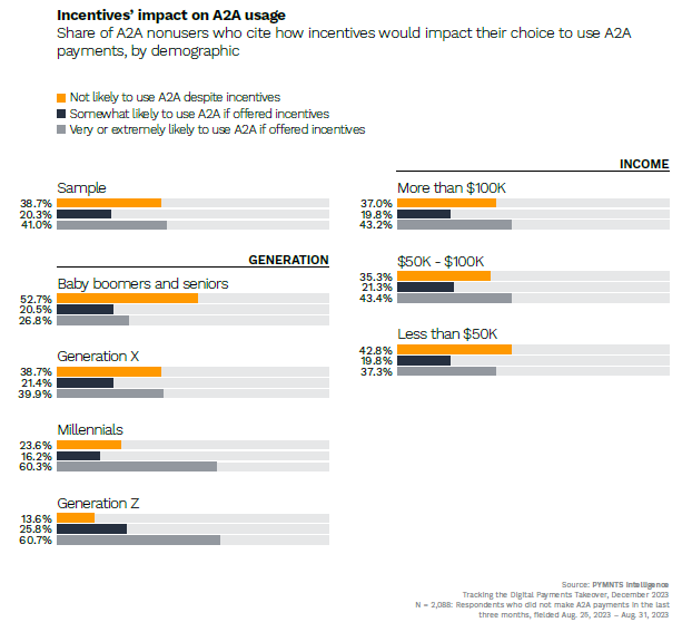

Incentives can play a role in fostering greater adoption of A2A payments. The survey indicates that 41% of consumers who have not used A2A payments in the 90 days leading up to the study expressed a willingness to switch if payment platforms introduced incentives such as cash-back offers, discounts or exclusive rewards.

“After all, when consumers feel they are gaining something unique or advantageous, they are also typically more likely to change their payment behaviors, thus providing a possible roadmap for increasing A2A market share,” the report noted.

Nevertheless, incentives alone are not enough to sway A2A payment skeptics. According to the study, 39% of U.S. consumers remain unconvinced about using these payments, even when offered financial incentives. This suggests that while incentives may draw in certain consumers to A2A transactions, they are not universally effective. Addressing the reservations of this more skeptical segment may require additional measures, such as intensified educational initiatives or feature enhancements.

Furthermore, consumers express a desire for incentives beyond monetary rewards — such as exclusive offers and early access to products. This underscores a diverse array of consumer preferences that A2A platforms need to carefully consider.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More