Retail behemoths Amazon and Walmart have become the two fiercest competitors for consumers’ retail spending. While the proliferation of mobile devices, apps and payment technologies makes online shopping ever more efficient, physical shopping seems increasingly friction-filled. As consumers seek more convenience, shopping has become a hybrid experience, blurring the lines between physical and online commerce.

Already each retail giant has moved aggressively into the other’s turf: Amazon into grocery with Whole Foods, Amazon Fresh and Amazon Subscribe & Save, and Walmart into eCommerce with the acquisition of Jet.com. Both have also expanded into retail-adjacent areas, health and wellness in particular. While Amazon and Walmart continue to establish themselves as leaders in providing easy access to daily essentials, they also compete for consumers’ discretionary income, even as inflation shrinks spending power.

These are just some of the findings detailed in The Battle for Consumer Retail Spend: Amazon Versus Walmart Q2 2022. In this report, PYMNTS provides the key takeaways from Q2 2022 consumer and retail spending trends, with a particular focus on consumers’ discretionary spend. While inflation has taken a toll on consumer spending for essentials such as groceries and healthcare products, it has certainly had an impact on discretionary spending as well.

report, PYMNTS provides the key takeaways from Q2 2022 consumer and retail spending trends, with a particular focus on consumers’ discretionary spend. While inflation has taken a toll on consumer spending for essentials such as groceries and healthcare products, it has certainly had an impact on discretionary spending as well.

More key findings from the study include:

• Amazon accounted for 6.5% of consumer retail spending and 3.1% of total consumer spending at the end of Q2 2022. With 7.1% of consumer retail spending, Walmart has slightly outperformed Amazon again this quarter, but has fallen slightly behind in total consumer spending, at 3.0%. In Q1 2019, Amazon held only 4.4% of consumer retail spending, which increased to 8.1% in Q4 2020. In Q1 2019, Walmart held 7.7% of consumer retail spending, reaching 8.4% in Q2 2020. As of Q2 2022, Walmart’s share of consumer retail spending has slipped below its 2019 levels of 7.1%, yet the company still holds the lead in that area.

• Amazon’s share of discretionary spending remains unchallenged, with Amazon holding 14% of this market versus only 4.9% for Walmart. Amazon continues to take the lead in all discretionary spending on sporting goods, music, hobbies, clothing and apparel, furniture and home furnishings, and electronics and appliances. In Q1 2019, Amazon held 8.7% of consumers’ discretionary spending. By Q2 2022, this share had increased to 14%. Not surprisingly, Amazon’s share reached a high of 17% during the pandemic in Q4 2020. Walmart, on the other hand, is losing ground in consumer discretionary spending — it started Q1 2019 holding a 5.6% share; by Q2 2022, it had decreased to 4.9%.

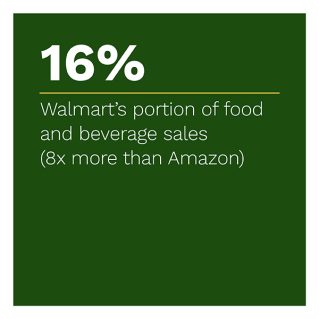

• Despite maintaining its lead in the food and beverage market, Walmart’s market share in grocery is slowly eroding, while Amazon still holds only a 2% share in Q2 2022, including its sales via Whole Foods Market. Competing for grocery market share is not as easy as it used to be, with other leaders such as Kroger, Target and Costco taking a bigger slice of sales. As of Q2 2022, Amazon’s share of the food and beverage market has not significantly changed since it acquired Whole Foods in 2017. During Q1 2019, Amazon held 1.7% of this market, meaning its share has increased by only 0.3% in the past three years. Walmart held 16.3% of the food and beverage segment in Q1 2019; as of Q2 2022, this share had fallen to 15.6%.

To learn more about how inflationary pressures have impacted employment and wages among paycheck-to-paycheck consumers, download the report.