According to a recent report by PYMNTS Intelligence and LendingClub, “The Paycheck-to-Paycheck Report: The Seasonal Financial Distress Deep Dive Edition,”60% of consumers in the United States are still living paycheck to paycheck as of August, a share that remains unchanged from the same time last year. Despite the stability of that figure, many of these consumers are living on the edge, as an unexpected $500 bill would give 1 in 4 consumers significant financial difficulty.

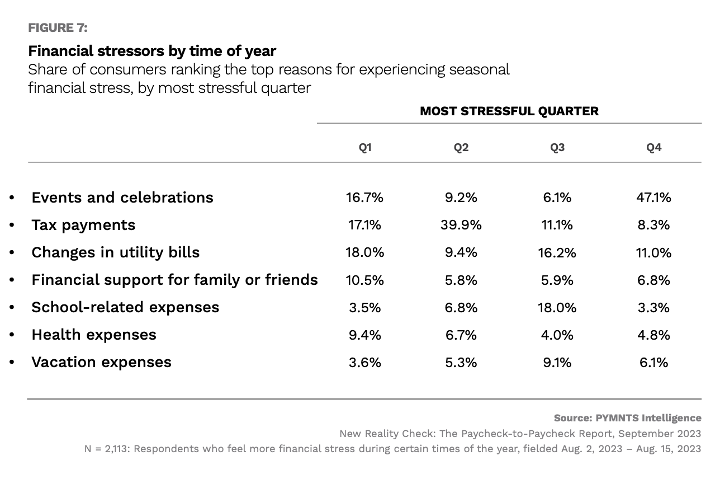

A number of seasonal factors can alter consumers’ financial stability, such as fluctuating utility bills, tax payments, school expenses or special events, among many others. The reasons behind seasonal financial distress by year’s end may vary throughout the year, but one common thread remains: events and celebrations, which are cited as the top Q4 financial stressor by 47% of consumers.

One major contributor to this is holiday spending. With the last-minute pressure to buy gifts and host gatherings, 36% of consumers identify December as the month of the highest seasonal financial distress.

Birthdays, weddings and other special occasions can put a significant strain on consumers’ wallets. With the added pressure to keep up with societal expectations, it’s no wonder that many Americans who live paycheck to paycheck find themselves struggling to pay their bills and make ends meet. This is happening across all income groups, including 45% of consumers who earn $100,000 or more annually.

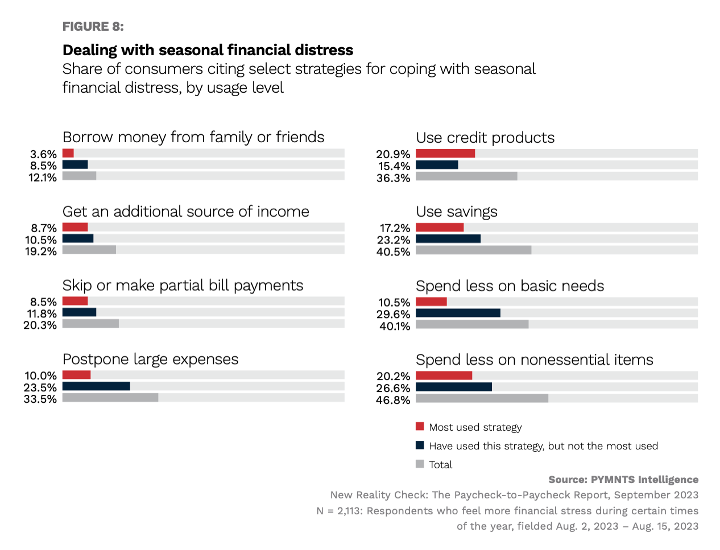

To cope with these seasonal financial challenges, consumers are employing a variety of strategies. Over a third of consumers turn to credit products to manage their finances, while 21% of them utilize it as their top strategy.

Those who don’t live paycheck to paycheck are more likely to rely on their savings or cut back on nonessential spending. On the other hand, those who are struggling to pay their bills often resort to skipping or making partial payments and reducing spending on basic necessities.

Using credit products to cover expenses in financially difficult times can negatively impact consumers’ financial standing, and this is happening with 3 in 4 consumers opting for this strategy. Shoppers should only rely on credit as a financial management tool instead of a way to stay afloat.

Seasonal financial distress only adds fuel to the fire, making it even more challenging for individuals to break free from this cycle. As the cost of living continues to rise, there is less money available for savings or discretionary spending. When faced with reduced hours or temporary unemployment, many individuals find themselves relying on credit or loans to make ends meet.

Breaking free from the paycheck-to-paycheck cycle requires careful financial planning and budgeting. It means prioritizing saving and seeking additional sources of income, but also exploring credit products that help individuals bring more stability to their finances over the course of the year.