A positive credit standing can also influence insurance premiums, impact the type of apartment an individual is eligible for, and in some cases even play a role in securing a new job opportunity.

In the joint PYMNTS-Sezzle research study “How Credit Insecurity is Changing U.S. Consumers’ Borrowing Habits,” we presented nearly 2,700 consumers with examples of nine distinct credit-related actions and asked respondents to identify how those actions contributed to boosting credit scores. Consumers were then grouped into three categories — credit secure, credit marginalized and credit avoidant.

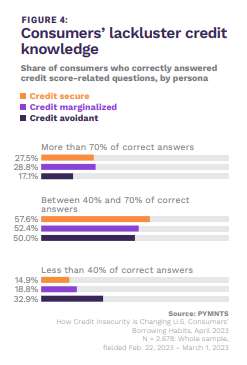

Findings captured in the report show that despite credit scores being a key financial resource, few consumers have a good understanding of how it works or how to improve their scores.

“Based on the small number of respondents that got all, or even most of, the credit score-related questions correct, it would appear that very few consumers know how to improve their credit scores and qualify for credit products,” the report noted.

Individuals who provided correct responses to 70% or more of the credit score-related inquiries were considered knowledgeable. Among them, credit-marginalized consumers, who tend to resort to high-interest payday loans and risky products to access credit, seem slightly more knowledgeable at 29% compared to credit-secure consumers at 28%.

“Credit-avoidant consumers are even less likely to fully comprehend the system, at 17%,” the report added, pointing out that “more than two-thirds of each group has a shaky understanding of the credit score system.”

Drilling down into the data further reveals that for most consumers, improving their credit scores boils down to paying bills on time, using a credit card or prudently managing their credit balances. As a result, a mere 27% of consumers are aware that utilizing a product like BNPL — where most loans have no or very low interest — could also be used to enhance their credit scores.

As the report noted, a better understanding of how credit works and how to leverage products like BNPL to their advantage can “enable credit-insecure consumers to access safer tools to cope with financial strain and even reverse some of the negative credit spiraling that is so common.”