Higher rates.

A bit more muted consumer sentiment.

The paycheck-to-paycheck pressures continue.

On Friday (Aug. 25), the final reading of the University of Michigan’s survey on consumer sentiment for August was released, showing that the index of consumer sentiment dipped to 69.5 from 71.6 in July.

“Consumers perceive that the rapid improvements in the economy from the past three months have moderated, particularly with inflation, and they are tentative about the outlook ahead,” Director Joanne Hsu said in a statement accompanying the release.

The survey also found that the expectations for “current” economic conditions were 75.7, down from 76.6 in July.

The outlook maybe further dampened by remarks from Federal Reserve Chair Jerome Powell, who said Friday at an economy policy symposium that “although inflation has moved down from its peak — a welcome development — it remains too high. We are prepared to raise rates further if appropriate.”

He said, too, that “12-month core inflation is still elevated, and there is substantial further ground to cover to get back to price stability…Getting inflation sustainably back down to 2% is expected to require a period of below-trend economic growth as well as some softening in labor market conditions.”

The read across here, then, is that rates are headed higher, and a softening labor market portends that wage growth might slow, job openings will slow, and employment rosters may shrink a bit.

These are hardly the types of trends that would lift consumers’ spirits at present — or in the months ahead.

No Relief in Sight for the Paycheck-to-Paycheck Economy

For the paycheck-to-paycheck economy — a designation that now encompasses a majority of consumers — Friday’s one-two punch might prove especially disquieting.

As detailed in our latest Paycheck to Paycheck report, 61% of consumers are living paycheck to paycheck, and as many as 21% of consumers have issues paying their monthly bills.

The pressures are acutely felt by households with young children under 18 years old. Those consumers are carrying credit card balances averaging around $7,200. Our data also shows that 66% of consumers with children are more likely to live paycheck to paycheck than the 59% of households without kids who also live similarly.

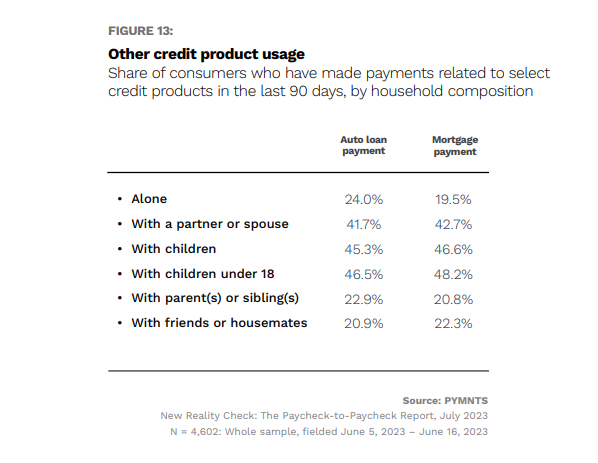

There are indications, too, that consumers — especially those who don’t live alone — are already contending with credit on the books, so to speak, that represent significant monthly obligations. The chart below details that mortgage and auto loan payments are key monthly recurring payments that must be contended with, no matter where money might be spent on other goods and services.

As a result, the middle class — defined as those earning between $50,000 to $100,000 annually — is feeling the pinch. Data shows that 73% of these consumers pulled back on retail products, and 60% pulled back on groceries.