Payment speed can be dragged down in many ways. For example, the payer company may have a convoluted invoice approval process to complete before it can compensate its SMB supplier. Additionally, an account-to-account transaction can become seriously derailed by an error like an incorrect bank account number. A remittance process that requires a consumer to trek to a money transfer company’s physical location and manually fill out paperwork introduces even more frictions.

Payment speed can be dragged down in many ways. For example, the payer company may have a convoluted invoice approval process to complete before it can compensate its SMB supplier. Additionally, an account-to-account transaction can become seriously derailed by an error like an incorrect bank account number. A remittance process that requires a consumer to trek to a money transfer company’s physical location and manually fill out paperwork introduces even more frictions.

In the new Smarter Payments Tracker, PYMNTS examines how the flow of money and data across borders is creating a new ecosystem in which payments data is as valuable as the funds themselves. This inaugural edition puts particular focus on the critical role of speed and cost in cross-border payments, and on how businesses are working to tackle these frictions.

Around the Smarter Payments World

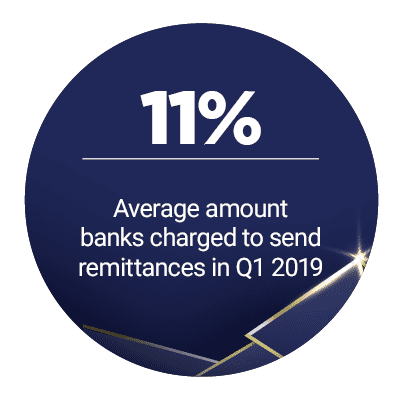

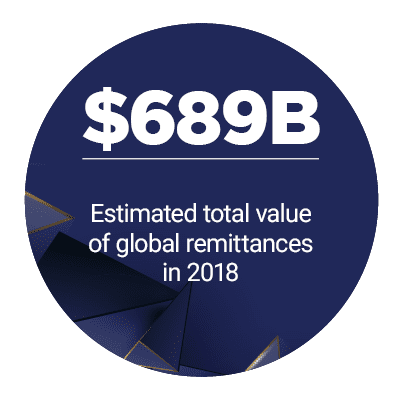

While the global remittance market is expected to reach $550 billion this year, according to a recent report, the market is still burdened by hefty transfer fees. In 2015, the United Nations established a goal of reducing remittance fees to 3 percent of the transaction value. Now, four years later, the average bank charges an 11 percent fee.

Money transfer companies are seizing this as an opportunity to offer low-cost remittances to give them a competitive edge. Xago, a South African money transfer operator, is among the latest companies to take up that strategy. The company is now leveraging Ripple’s technology in an effort to provide streamlined remittances at a lower price.

Xago isn’t the only company angling for a greater share of the African remittance market. Tech startup BeepTool is aiming to win a larger role in helping to transfer the $24 billion that Nigerians send home each year. To do so, the company launched a new app that can send remittances to recipients’ mobile wallets, bank accounts or into billing systems on their behalf, without card fees.

Find the rest of the latest headlines in the Tracker.

Deep Dive: A Need for Speed and Security Pushes Push Payments

For any commercial system to run smoothly, merchants must be assured that their customers will pay them the promised funds in a timely manner, and customers must trust that the merchants will keep their payment and personal data secure. Push payments are increasingly being upheld as a way to provide both parties with greater confidence in the transaction.

This month’s Deep Dive investigates the growing interest in push payments, and its potential to streamline and secure consumer payments, B2B supplier payments, and B2C payroll and loans.

Faster Payments Deliver ‘Instant Gratification’ for India’s Migrant Workers

Speaking of payroll, migrant workers in India are 100 million strong, and make up a sizable share of the nation’s labor market. For many of these workers, sending remittances home to family members involves handing over money to couriers or postal services, and hoping it arrives safely. This arrangement can be anxiety-inducing, as migrants wait days to find out if their money was delivered to the intended recipient. Yet, these fears could soon become a thing of the past, according to YES BANK’s Chief Digital Officer Ritesh Pai.

In the April feature story, Pai explained how the emergence of India’s faster payment systems, including IMPS and UPI, are putting common money transfer fears to rest, and why fast remittance confirmation is as important as the speed of the remittance itself.

To get the full scoop, download the Tracker.

About the Tracker

The monthly Smarter Payments Tracker, a PYMNTS and InstaReM collaboration, is the go-to resource for staying up to date on the development of a new global payments landscape, in which transmission of the data is as valuable as transmission of the currency it accompanies. The Tracker explores how the smooth flow of payments data can improve existing payment ecosystems, including enabling improved speed, security and insights.

For small and medium-sized businesses (SMBs) and consumers, payments that arrive promptly are worth far more than payments of the same dollar value that trickle in after weeks of delays. After all, money on hand can be used immediately to pay bills, invest or make purchases — to grow a business or put a family on firmer financial standing.

For small and medium-sized businesses (SMBs) and consumers, payments that arrive promptly are worth far more than payments of the same dollar value that trickle in after weeks of delays. After all, money on hand can be used immediately to pay bills, invest or make purchases — to grow a business or put a family on firmer financial standing.