Financial institutions (FIs), FinTechs and other organizations must be able to facilitate remittances while filtering out bad actors that may try to abuse the services for funding crime. Abiding by different countries’ anti-money laundering (AML) and counter-terrorist financing (CTF) laws helps these organizations fend off such fraud and avoid noncompliance fees, but FIs and FinTechs may struggle to monitor all these different laws.

FinTechs may struggle to monitor all these different laws.

The September Smarter Payments Tracker® examines cross-border money transfer organizations’ compliance challenges and how regulatory tools and strategies can help remittances providers stay up to date with relevant legislation in each country they serve and keep current as those policies are updated.

Around The Smarter Payments World

The regulatory landscape is ever-changing, and the United Kingdom’s Financial Conduct Authority (FCA) is currently weighing whether to raise its requirements on a variety of financial firms. The potentially impacted businesses include electronic money institutions, payment companies, cryptocurrency wallet providers and others — although companies that exclusively offer remittances would not be affected — and these firms would have to participate in more suspicious activity reporting if new policies are passed. The FCA is accepting feedback on its proposal through late November.

The other major regulatory change facing financial services companies that serve the U.K. is the upcoming Brexit transition, slated for Dec. 31. Companies that had previously used European electronic money institution (EMI) licenses to qualify them for serving U.K. customers are now working to get new, U.K.-specific licenses so they will be ready once the breakup goes into effect. FinTech platform Nium is one such company that recently obtained this license.

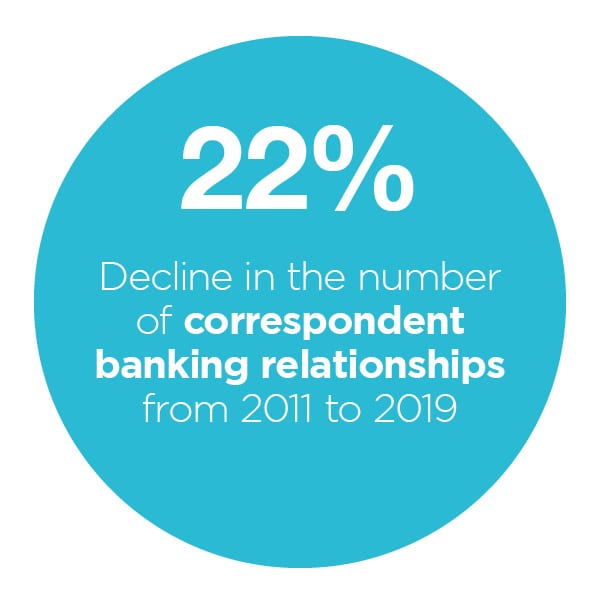

The United States is looking to make its own regulatory updates, with the federal Office Of The Comptroller of the Currency (OCC) anno uncing that it intends to update national banking regulations so that they stay current as needs and technologies change. This includes examining and issuing policies around how banks use distributed ledger technologies (DLT). Amit Sharma, DLT advocate and CEO of financial services-focused blockchain platform provider FinClusive recently released comments in response, urging the OCC to consider how DLT can be used beneficially, such as to provide payment tracking that supports regulatory oversight.

uncing that it intends to update national banking regulations so that they stay current as needs and technologies change. This includes examining and issuing policies around how banks use distributed ledger technologies (DLT). Amit Sharma, DLT advocate and CEO of financial services-focused blockchain platform provider FinClusive recently released comments in response, urging the OCC to consider how DLT can be used beneficially, such as to provide payment tracking that supports regulatory oversight.

Read more about these and all the rest of the latest headlines in the Tracker®.

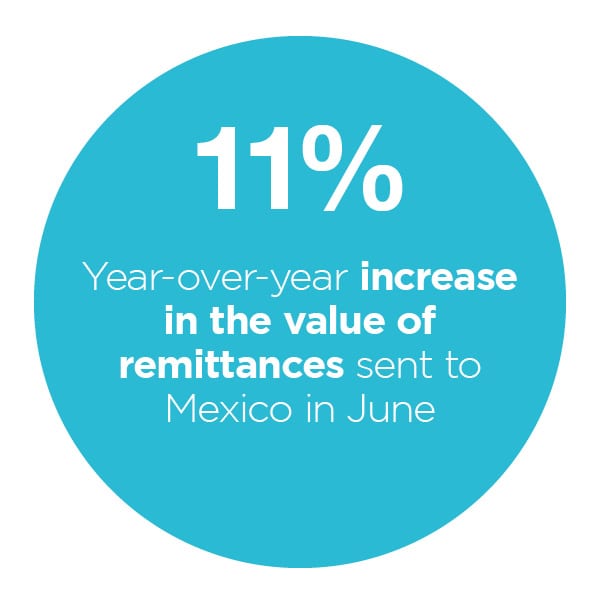

How The Pandemic Is Driving Singapore’s Foreign Workers To Adopt Digital Remittances

Migrant workers are more than 20 percent of Singapore’s population, with many coming to the country to earn money they can send back home to support family members. Government efforts to control the spread of the COVID-19 pandemic interrupted the ability to send remittances, however, with many workers confined to dormitories and unable to visit money transfer agents. Keeping remittances flowing smoothly during this time meant providing ways for workers to remotely access services — such as through mobile apps. In this month’s Feature Story, Sam Tay, CEO of FinTech Aptiv8, which provides an app designed to support Singapore’s foreign workers, and Ho Chee Wai — country head of Singapore for banking-as-a-service provider Nium — discusses the value of remittances apps and why foreign workers may keep using them after the pandemic recedes.

Download the Tracker to read the full story.

Deep Dive: How Regulatory Compliance Tools Help K eep Remittances Flowing

eep Remittances Flowing

Money transfer organizations need to stay compliant with regulations or else they will face significant fees or allow crime to spread. Banks that fail to impose sufficiently strong anti-fraud measures also may find that other FIs are unwilling to work with them on facilitating international remittances, forcing them to find more costly ways to offer the services or to forgo providing them at all. This month’s Deep Dive examines the struggles FIs face in maintaining compliance and how technology-based security strategies can help.

Find the Deep Dive in the Tracker ®.

About The Tracker

The Smarter Payments Tracker®, done in collaboration with Nium, details the latest regulatory trends and technologies impacting international remittances.

Cross-border remittances are a lifeline for many households who depend on family members working abroad to send funds home. These international money flows reached $689 billion in 2018, and ensuring funds continue to flow smoothly requires money transfer organizations to provide services that are both convenient and compliant with regulations.

Cross-border remittances are a lifeline for many households who depend on family members working abroad to send funds home. These international money flows reached $689 billion in 2018, and ensuring funds continue to flow smoothly requires money transfer organizations to provide services that are both convenient and compliant with regulations.