Small- to medium-sized businesses (SMBs) facing limited access to funding are turning to external sources to finance their operations.

However, access to credit remains a challenge, leaving them vulnerable in times of financial difficulties. This is particularly true among Main Street businesses, where nearly 34% of SMBs do not currently use credit but want to start doing so. That’s according to “Main Street Health Q2 2023: Credit’s Key Role in SMBs’ Plans,” a PYMNTS and Enigma collaboration,

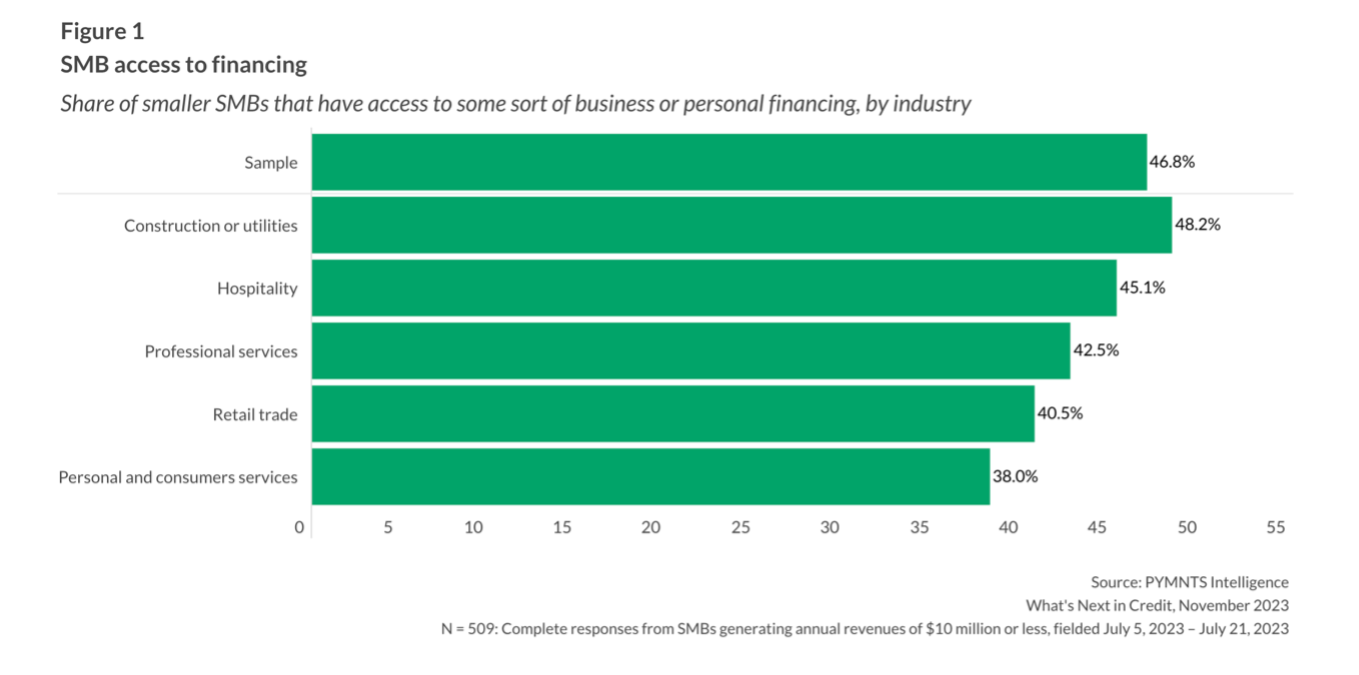

As of July 2023, only 47% of SMBs with annual revenues of $10 million or less had access to business or personal financing, according to PYMNTS Intelligence’s latest “What’s Next in Credit” report. The availability of financing varies across industries, with just 41% of SMB retailers having access, compared to 48% of construction or utility SMBs.

Having no access to credit means that these SMBs must rely on other sources of funding. For instance, PYMNTS Intelligence found that 8% of SMBs have access to only personal financing.

Businesses relying on this source of financing are in a tenuous position as personal savings are drying up. According to “Main Street Health Q2 2023: Credit’s Key Role in SMBs’ Plans,” 8.6% of retail SMBs say they are at risk of closing their doors in the near term, with that number rising to 19% for retailers with with access to less than $5,000 in cash.

To avoid business closures and position themselves for growth, many SMBs are looking to outside financing to address their business needs. Almost half of Main Street SMBs say they plan to increase the use of credit products, according to Main Street Health Q2 2023, which was created in collaboration with Enigma.

The study also reported that corporate credit cards are considered the preferred source of financing by Main Street SMBs, as they can help them to cover both expected and unexpected expenses. Over half (52%) of SMBs say they plan to use the financing tool in the next 12 months, surpassing business loans from online lenders (22%) or working capital loans from banks (21%). This indicates a growing market opportunity for card issuers.

However, PYMNTS Intelligence’s “What’s Next in Credit” report found that that only 28% have access to credit card financing, pointing to the challenges these firms may face in obtaining funding.

Corporate cards offer benefits such as low-interest access to funds and improved cash flow management for both buyers and suppliers. By easing access to credit and providing corporate cards, financial institutions can support SMBs in their business growth and help them overcome the challenges of rising costs and inflation. This, in turn, can contribute to the overall stability and success of the SMB sector.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More