Small- to medium-sized businesses (SMBs) on Main Street are finding a dearth of options when it comes to getting the money they need to stay in business.

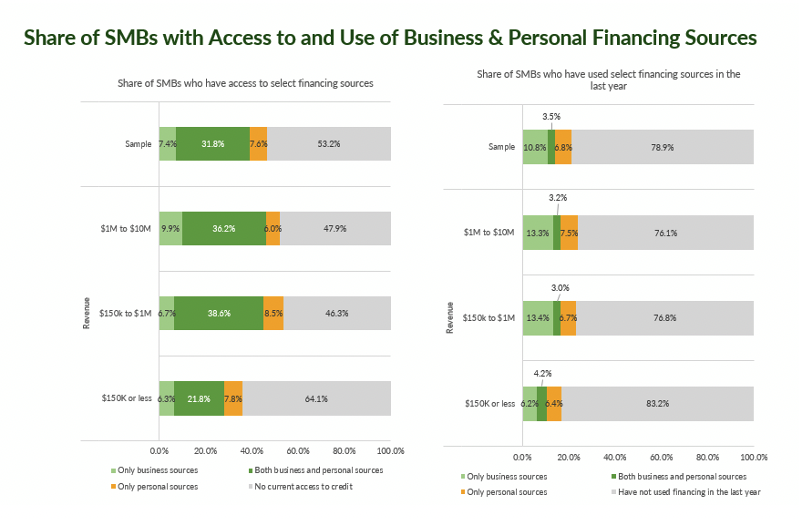

PYMNTS Intelligence found that more than half of SMBs — 53% to be exact — have “no current access to credit.” The percentage is even more starkly seen among the smallest companies surveyed, with $150,000 or less in annual revenue.

Having no access means that these SMBs must rely on the funding sources that are on hand. Only about a third of the more than 500 SMB owners surveyed said they had access to both business and personal funds.

Drill down a bit, and the dry powder is in place, at least for now, as roughly 79% of all SMBs haven’t had to tap those financing sources in the past year.

But the dry powder is finite. And for at least some of these companies — the 7.6% that have access to only personal sources of funding, for example — the pressure may be considerable.

But the dry powder is finite. And for at least some of these companies — the 7.6% that have access to only personal sources of funding, for example — the pressure may be considerable.

Personal finances are in a precarious state. The string of PYMNTS’ paycheck-to-paycheck economy reports showed that about 60% of individuals live paycheck to paycheck. Pandemic-era savings have been largely exhausted. One-third of consumers owe more than $250,000 in debt, and 3 in 10 consumers have overdue payments with which they need to grapple.

It follows, then, that for the smallest companies, especially sole proprietorships that may be wholly dependent on the fortunes and liquidity of one person or a household, options may limited in the months ahead. Roughly a third of SMBs have been using personal credit cards to keep things going. With rising rates and more than $1 trillion in credit card debt being shouldered by consumers, and 22% of SMBs using monies tied to personal investment assets, which are volatile at best, the options are less than optimal.

The findings that most firms do not have access to credit come as roughly half of companies on Main Street are shopping for credit. PYMNTS Intelligence found that 40% of SMBs remain more worried about inflation than one year ago. As many as 15% reported being concerned about declining revenues. Forty-eight percent of companies have “more credit” on their proverbial to-do lists.

The latest economic data on jobs creation, which came in better than expected, underscored the fact that the Federal Reserve may keep raising rates; higher rates for longer has been the maxim by which small businesses must live. And for many of them, credit is a concern, an elusive goal — and what comes next may be painful.