In “SMB Borrowing Dynamics: Trends, Tools and Decision Drivers” — a PYMNTS Intelligence and U.S. Bank report — we identified several factors that help business owners decide which funding options make sense. Chief among them are annual revenues.

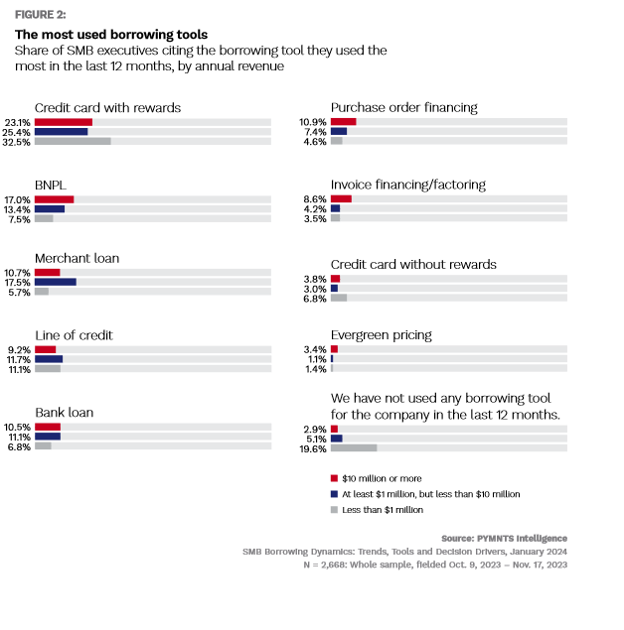

The report — which reflects feedback from 2,668 SMB executives — revealed low-revenue SMBs tend to prioritize immediate capital needs and financial stability over what their higher-revenue SMB counterparts consider. This might explain why, given last year’s bumpy economic run, nearly 20% of low-revenue SMBs (defined in the study as those earning less than $1M annually) declined to leverage any borrowing tools during that time.

But, for nearly one-third of low-revenue SMBs, reward-earning credit cards were the funding resource of choice last year. The reason? The report determined reward-earning credit cards appeal to this segment of SMBs because they offer “immediate benefits that provide tangible value.”

Reward credit cards, in fact, were the most popular funding source for all SMBs during the last 12 months. Twenty-three percent of high-revenue SMBs (those earning between $10M and $25M annually) used reward-bearing credit cards as their first line of defense borrowing tool. Meanwhile, 17% of the high-revenue segment used BNPL funding options, a tool less than 8% of low-earning SMBs used.

More than 25% of SMBs in the center (revenue between $1M and $10M) preferred reward credit cards, while about 13% of them used BNPL funding to cover their bills.

It remains to be seen how the latest inflation numbers will impact SMBs, but this variance in the data suggests that financial institutions (FIs) hoping to serve this market should focus on providing a diverse range of borrowing tools — especially reward-earning credit cards and BNPL which appeal to SMBs.

FIs seeking to connect with lower-revenue SMBs should know this segment is especially cautious — but that caution may be overcome by developing and marketing products that address concerns smaller SMBs hold.