Financial institutions (FIs) are working during the pandemic to provide speedy digital services while fighting off the rise in fraud attempts. Small- to medium-sized business (SMB) customers need rapid access to loans as they attempt to stay afloat, and FIs must be able to quickly vet borrowers to ensure funds do not accidentally go to fraudsters.

Some players in the space are now suggesting that open banking could be a tool to help FIs accelerate the know your customer (KYC) processes. FIs that enable open banking make application program interfaces (APIs) available to third parties, which can then use the APIs to seamlessly draw on customer data. Such easy data flow could help when SMBs are seeking loans that their current banks do not offer. The lenders integrate with APIs from the customers’ home banks to quickly access information that would help in verifying applicants’ identities and making approval decisions.

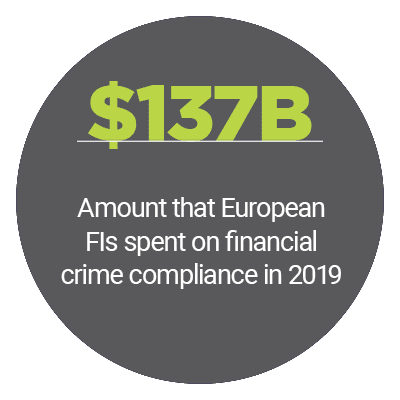

The June “AML/KYC Tracker®” explores these and other methods that financial services companies are adopting as they work to make their security efforts both faster and more accurate.

FIs have long provided digital services, but many have designed these experiences for the customer demographics that most prefer online and mobile channels. The pandemic has now pushed brick-and-mortar customers to turn to digital, too, and FIs must ensure their virtual KYC processes are easily accessible to this new group. FIs must consider whether digital newcomers will find it easy to understand how to conduct video KYC processes, for example, said Zac Cohen, chief operating officer of global identity verification solutions provider Trulioo, in a recent PYMNTS interview.

Some customers may prefer to avoid mobile interfaces entirely and simply dial in to call centers for their needs. That means that FIs must be able to quickly confirm which callers are legitimate customers and which are fraudsters pretending to be. One company that provides fraud-fighting solutions to FIs recently began offering voice-based authentication to help banks verify customers based on their vocal pitches and rhythms.

Smartphone natives, meanwhile, may prefer to access all their services via mobile channels, and eCommerce merchants can leverage this consumer group to help them detect bad actors. Jon Prideaux, CEO of payment solutions provider Boku, recently told PYMNTS that companies receiving mobile orders work with telecommunication firms to confirm that identities being presented by the online shoppers match those of the individuals known to own the mobile devices. This can help merchants feel more confident that the customer is legitimate and not a fraudster.

FIs know that open banking can enable new services that customers want, but they also realize that offering them must not come at the expense of security. Many FIs are concerned about whether opening their APIs to FinTechs would result in criminals abusing open banking-powered payment apps to launder money, for example.

FinTechs that can prove they have robust security measures in place to prevent such problems are likely to win over FIs and help advance the open banking movement. In this month’s Feature Story, Andrew Davies, vice president of global market strategy and financial crime risk management at financial services company Fiserv, discusses the anti-money laundering (AML) and KYC security methods FinTechs are adopting to keep their services safe and encourage FIs to partner with them.

FIs that are interested in open banking are also taking measures to make themselves more secure should anything happen to compromise their FinTech partners. Third parties with weak defenses could fall victim to hackers that then can use the links between them and API-connected FIs to steal bank customer data, or consumers might be tricked into handing over sensitive bank login information to fraudsters pretending to be legitimate FinTechs.

This month’s Deep Dive digs into the issue to examine key fraud risks that come with open banking and how FIs can combat them.

The “AML/KYC Tracker®,” a PYMNTS and Trulioo collaboration, provides an in-depth examination of current efforts to stop money laundering, fight fraud and improve customer identity authentication in the financial services space.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More