A few words sum up the state of fraud and the challenges facing financial institutions (FIs): rising at a fast clip.

In the report “The State of Fraud and Financial Crime in the U.S.,” a PYMNTS and Featurespace collaboration, 200 executives from a range of FIs with assets of at least $5 billion revealed heightened awareness about money laundering and other financial fraud — and the need for innovation to detect and prevent it.

Ninety-five percent of AML executives said they consider it a “high priority” to use advanced technologies in those efforts. But as many as 85% of those queried also expressed some concerns about the challenges of embracing those same technologies.

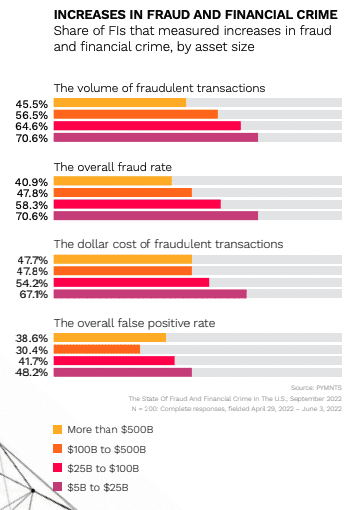

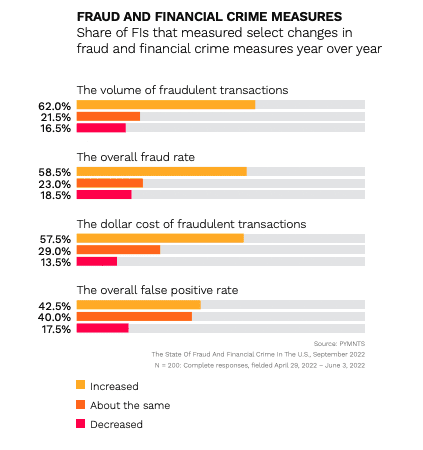

The study found that losses from fraud average about 1.29 basis points per transaction. Overall, 59% of the firms that were surveyed said they had experienced an overall increase in fraud rates in the past year. Small firms were hardest hit, with a full 71% reporting an increase. Meanwhile, only 23% of respondents said they had experienced fraud rates that were “about the same” — hardly an encouraging sign.

Dollar amounts lost to fraud — and the false positives raised by their in-place processes — are on the rise too.