Consumers are more security-savvy than ever, especially when it comes to fraud prevention in banking. They also have more choice in primary financial institutions (FIs) than ever, from traditional banks to full-on FinTechs — and may be willing to switch if their security and other needs go unmet.

Over one-third of banking customers want their FIs to offer more visible security measures requiring a user to act, such as entering a password or using biometric authentication for high-risk financial activities. Another 27% would like the same for routine transactions. While consumer preference may vary on methods to accomplish this, it’s clear that the long reign of passwords as the favored online identity authentication method may be ending. The array of preferred authentication method choice by consumers is illustrated in the PYMNTS collaboration with Entersekt, “Visible and Invisible Security: Perceptions in Digital Banking.”

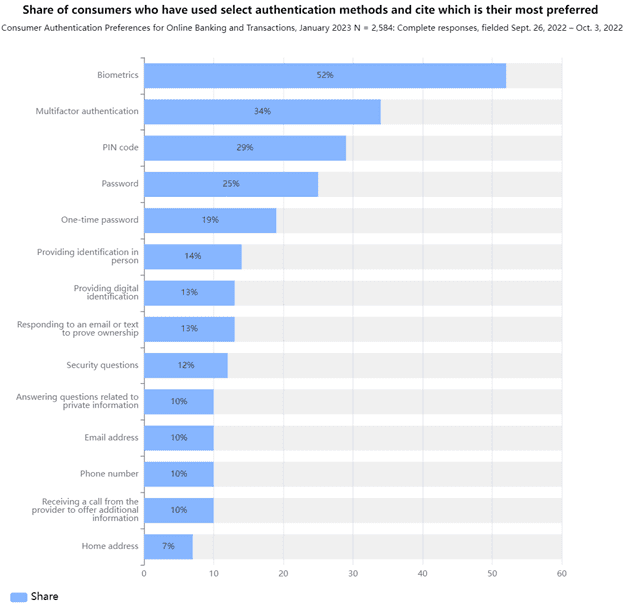

Biometrics is far and away the favorite choice among surveyed consumers, with 52% citing the authentication method as their most preferred. However, despite biometrics’ promise as the next generation of authentication, its use is not yet widely adopted. However, the somewhat distant second most cited response, multifactor authentication (MFA), is now a commonly used protocol. It is also well-trusted, as 62% of those who chose MFA as their preferred authentication method did so because of its perceived stronger security. Given its rate of consumer acceptance and fraud-fighting abilities, both straddling between passwords and biometrics’ utility, MFA may be the natural “transitionary” protocol until biometrics is widely adopted.

In an interview with PYMNTS, senior director of operations for fraud tech at First Tech, Seth Rudin, explains how MFA fits into his organization’s greater security strategy. “We look at the full life cycle of an individual’s engagement with their financial institution by ensuring that our members have strong security hygiene, that they’re using the right kind of passwords, that they’ve got multifactor authentication options that suit their lifestyles and that we have the right kind of fraud [prevention] tools that provide the right kind of alerts that the member can engage with specifically.”

Passwords’ fraud-fighting ability has long faded and biometrics has not yet reached table-stakes acceptance levels. Until that transition is complete, MFA may be the authentication method to beat — for now.