“You can’t always get what you want” are both lyrics made famous by Mick Jagger in the 1968 rock classic by the same name and very likely the most frequently spoken words by parents everywhere.

It also happens to be a fitting commentary on the working capital needs of a category of companies called Growth Corporates — most typically referred to as the middle market — and the solutions available to support their cashflow requirements.

This is one of several important insights from the 2023-2024 Growth Corporates Working Capital Index (Growth Corporates WCI), the Visa report released yesterday examining the operational efficiency of 873 CFOs in 23 countries and five highly dynamic industry sectors: Fleet/Mobility, Healthcare, Marketplaces, B2B Travel, and Agriculture. Visa commissioned PYMNTS Intelligence to conduct the research and construct the Index.

The Index measures the operational efficiency of Growth Corporate businesses using the Days Payable Outstanding (DPO) metric, and it makes sense. A business with a mastery of its own cashflow forecasting and management can pay its bills on time, take advantage of favorable pricing or supply opportunistically, and negotiate discounts for early payment. Growth Corporates that can optimize their use of working capital can add as much as $3.3 million annually to their bottom line.

This calculated use of working capital solutions to fund strategic growth initiatives has the knock-on effect of creating a financially healthy supply chain and growth corporate ecosystem — a benefit that 69% of Growth Corporates say is a key priority, as supplier relationships have become an important source of competitive advantage. Growth Corporate CFOs who use working capital solutions to fund scheduled business growth initiatives and who have 90% of suppliers integrated into their payment system have a 67% higher probability of seeing improvements to their DPO than their counterparts who don’t.

However, Index performance suggests that the working capital solutions used by Growth Corporates may not deliver the operational efficiencies or the optimal working capital ROI needed to support their growth, particularly if they are not available in a timeframe that’s relevant for the business.

One of the biggest impediments facing Growth Corporates is the speed to decision — traditional providers of working capital solutions have traditional (and lengthy) risk management parameters, along with credit limits, that impede the nimble financing of initiatives.

The unintended consequence of undue cash flow pressures on these dynamic businesses in today’s increasingly constrained and expensive corporate credit market can mute their growth prospects.

It’s time for solution providers to think beyond the status quo to cultivate relationships with the next generation of industry leaders powering the digital economy.

Creating Operational Efficiencies

Growth Corporates are the middle children of the business world: too big for small business solutions, and too small for the sophisticated working capital solutions of giant multinationals. With annual revenues of between $50 million and $1 billion, these companies, globally, account collectively for $50 trillion in sales, operating in industry verticals undergoing their own rapid shift to digital.

Whether it is the agricultural sector moving from paper invoices and checks to electronic buying and selling, healthcare providers and claims processors using digital to improve the patient/provider experience, or fleet operators and mobility platforms navigating the shift to EV, secular and competitive pressures compel these businesses to seek capital to invest for strategic growth. And to have working capital solutions available — on demand — as the needs of these dynamic businesses arise.

The good news coming out of this report is that many Growth Corporates have access to working capital solutions. Across the companies and sectors studied, 71% reported accessing external sources of working capital over the last 12 months.

Two-thirds of Growth Corporate CFOs who used external sources of working capital in that period did so to support a variety of strategic business needs. Use cases ranged from covering planned cash flow gaps associated with predictable business cycles to funding systems upgrades, buying inventory at discounted pricing, and making investments in business infrastructure to support product development and innovation. These CFOs are expected to see a 33% increase in improved DPO efficiencies compared to those who use external financing only for emergencies and unplanned cash flow shortages.

Top Index performers — those with an Index score of 70 — also have 14 days shorter cash conversion cycles (CCC) and 9 fewer days in inventory outstanding (DIO). Lower DPOs, lower DIOs and shorter cash conversion cycles increase investor confidence and fuel growth initiatives such as expanding product lines, entering new markets, or increasing production capacity — without extended waiting periods for cash to be generated organically. The efficient use of working capital can pay big dividends beyond what’s borrowed.

Why the Index Matters

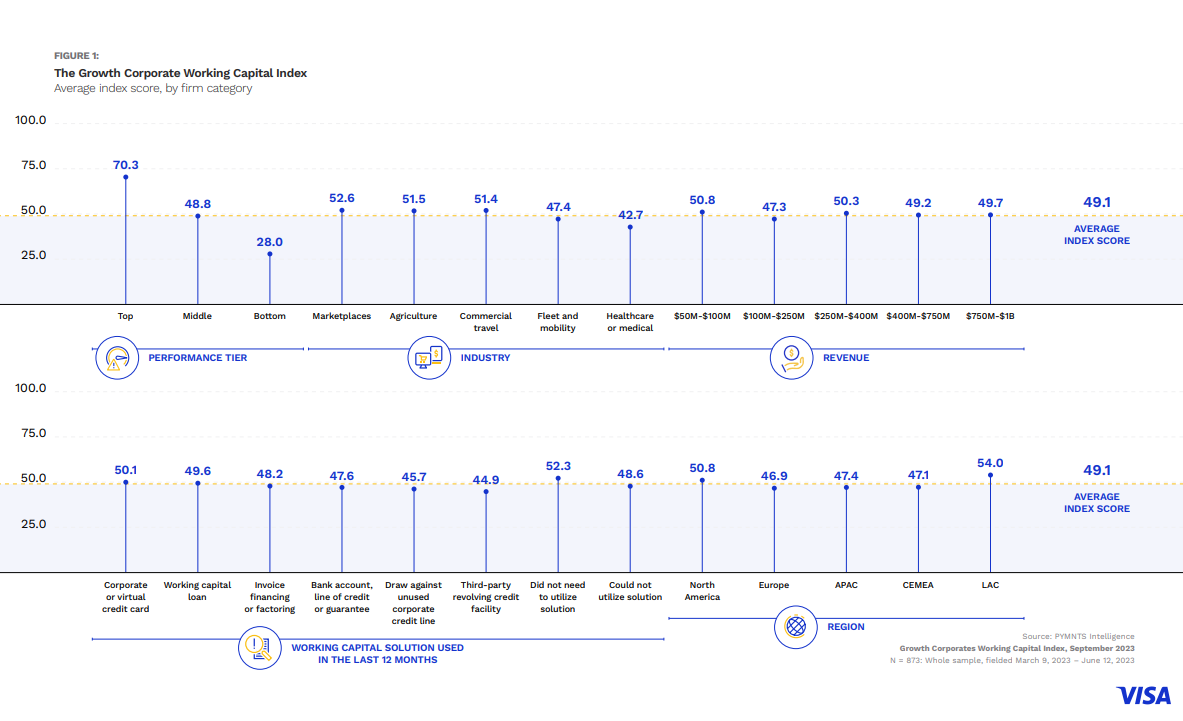

The Growth Corporates Working Capital Index takes a fresh look at the impact of working capital access to the financial performance of the category of businesses forging new paths across the digital economy. The Index ranks firms on a scale from 0 to 100, with 100 representing the perfect ratio of operational efficiency with the use of working capital solutions. The average score for the companies across the sectors and geographies studied was slightly below the halfway mark, at 49, suggesting room for improvement and hinting at a broader misalignment of the needs of these dynamic businesses with the working capital options available to them.

The Index finds that the most widely used external working capital solutions by Growth Corporates are also the more traditional sources of external working capital — the things banks have offered for decades and what their internal underwriting and risk models support.

Forty percent of Growth Corporate CFOs use working capital loans and bank lines of credit as their go-to financing options, though many Growth Corporates say they will reduce their reliance on them next year. Interestingly, only 14% of those who plan to use working capital loans as their go-to solution next year are top performers, and only 15% of those planning to use primarily overdrafts are in this tier.

Working capital loans and overdrafts from corporate bank accounts are most used by nearly 50% of firms in the EU. Similarly, Letters of Credit and invoice factoring are most used by Growth Corporates in LAC. Growth Corporates in need of working capital to fund unplanned or unexpected cash flow gaps used solutions such as bank overdrafts or lines of credit due to the nature of their need and the lack of other timely sources of external capital in the last 12 months. Growth Corporates in the smaller revenue range — those between $50M to $250M — most often used bank lines of credit, third-party revolving credit facilities and invoice financing/factoring.

The Index finds that 18 percent of Growth Corporate CFOs sub-optimize their use of working capital, either through lack of access or a misalignment of the working capital solution to their sector-specific needs. Growth Corporates in need of working capital to fund unplanned or unexpected cash flow gaps used solutions such as bank overdrafts or established lines of credit due to the lack of other timely sources of external capital in the last 12 months.

The Need to Mind the Gap

The gap between Growth Corporate working capital solution relevance and working capital solution usage is an opportunity for solution providers to create a more diverse and accessible portfolio of solutions that can align with the needs of the needs of the businesses operating in these sectors around the world.

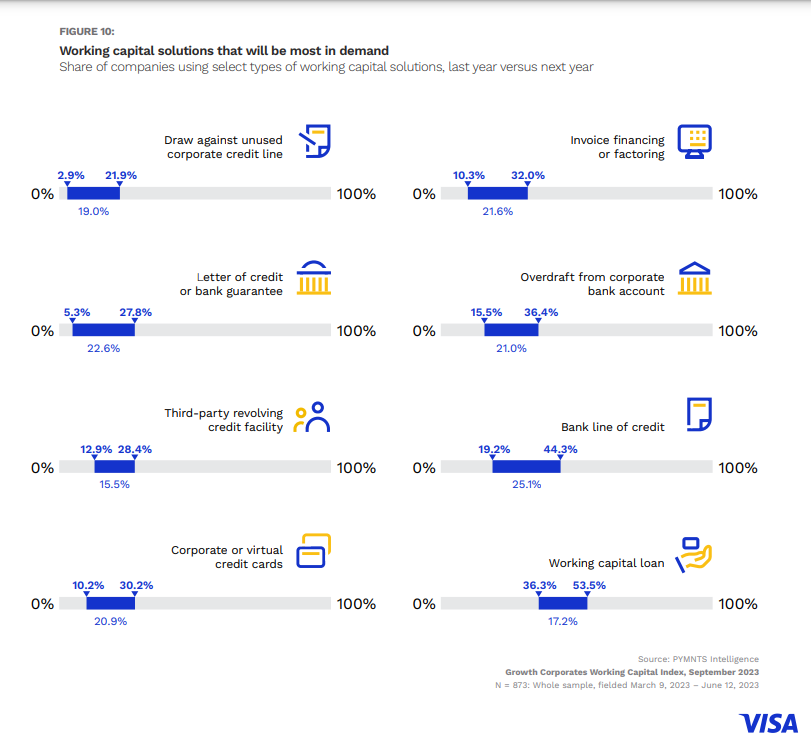

Nearly all — 92% — of Growth Corporates say they will seek external sources of working capital in the next 12 months; the use of less traditional financing options is being explored by many. The need to tap real-time, on-demand access to credit will increase the use of virtual cards by +196%, and the pooling of credit card lines across their organizations by +655%, particularly in the marketplaces and commercial travel industries, and in CEMEA and Latin America and the Caribbean.

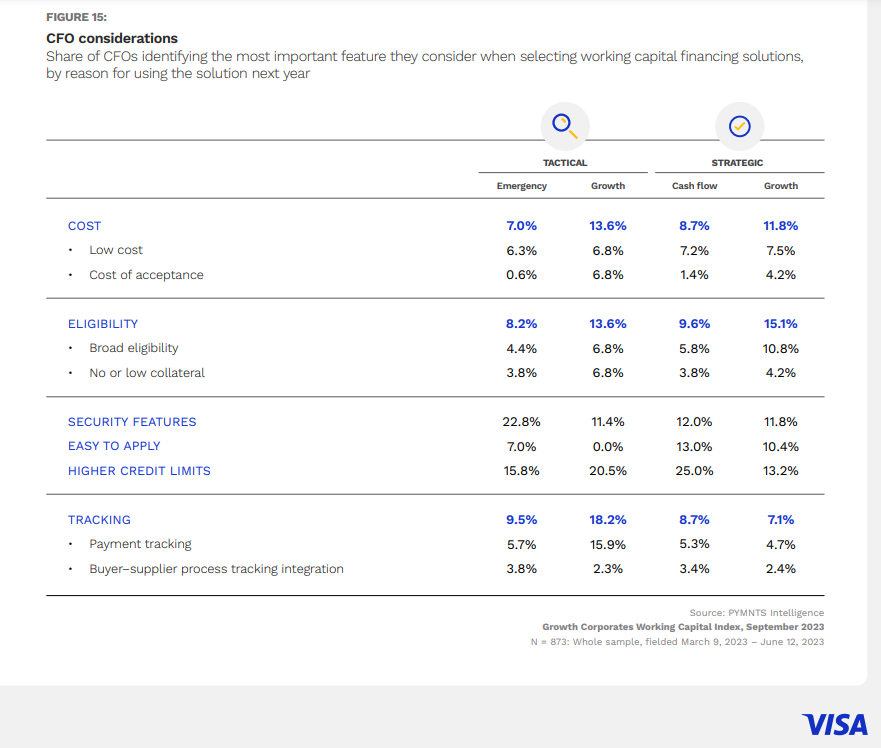

Growth Corporates are also looking beyond the more traditional sources of working capital solutions for advice and products that best fit their needs. Although their banker or a bank remains the leading choice for many Growth Corporates in the marketplaces and commercial travel sectors — and in Asia Pacific and Latin America and the Caribbean geographies — FinTechs and card networks have emerged as sources of working capital given the speed of decision making, acceptable financing terms and borrowing limits.

Because just like Mick said: If you try sometimes, you just might find, you get what you need.