Buy now, pay later (BNPL) has gained popularity in recent years among consumers and merchants alike.

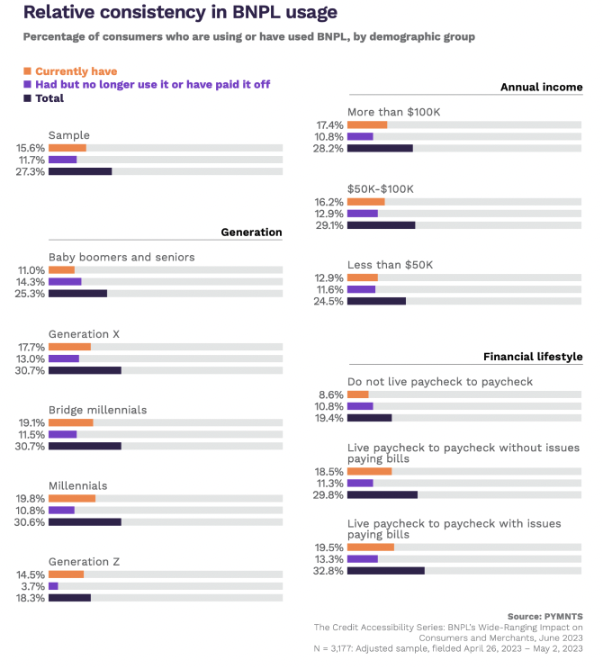

The payment method allows consumers to obtain goods and services upfront through short-term loans, often without any interest. Given its convenience, accessibility and affordability, BNPL is not limited to a specific demographic. Even high-income individuals earning over $100,000 annually and young consumers living paycheck-to-paycheck have embraced BNPL.

Credit solutions providers ranging from merchants to specialty players offer the payment method.

“The Credit Accessibility Series: BNPL’s Wide-Ranging Impact on Consumers and Merchants,” a PYMNTS Intelligence and Sezzle collaboration, assessed the rising popularity of BNPL products as a credit option and consumers’ reasons for using it.

The study found that 16% of consumers — or 40.5 million people — in the United States used BNPL for at least one payment in April. To these consumers, BNPL eased the acquisition of certain products or services they could not afford otherwise. Forty-three percent of BNPL users revealed they would have either delayed a purchase or opted for a cheaper product if BNPL was not available.

Additionally, the availability of BNPL can increase the likelihood of securing sales for higher-value products. The findings highlighted the importance for merchants to offer BNPL as a payment option to avoid lost sales.

Many consumers opt for this credit alternative when shopping, but how often do they use it? On average, 16% of BNPL users made purchases using the product at least weekly, and another 25% did so monthly, per the study. This means that nearly 4 out of 10 U.S. consumers used BNPL products at least once a month. This frequency was higher among millennials and bridge millennials, with nearly half of this segment using BNPL at least once a month.

Many consumers opt for this credit alternative when shopping, but how often do they use it? On average, 16% of BNPL users made purchases using the product at least weekly, and another 25% did so monthly, per the study. This means that nearly 4 out of 10 U.S. consumers used BNPL products at least once a month. This frequency was higher among millennials and bridge millennials, with nearly half of this segment using BNPL at least once a month.

The study found that Afterpay was the BNPL provider preferred by U.S. consumers, with 42% of respondents using it, followed by Affirm with 37% and Klarna with 34%. PayPal Pay in 4 was not the most used system, but it was the most well-known solution, as 46% of consumers were aware of it.

Meanwhile, Sezzle, Splitit and Four were strong among bridge millennials, while Shop Pay Installments and Quadpay had a prevalent position among Generation Z consumers.

Preserving cash and lines of credit is the primary reason for most BNPL users to choose this payment method. Consumers’ willingness to buy products in installments is increasing over time, and the use of BNPL is evolving in parallel. Retailers must know that the unavailability of this credit option in certain products may result in potential sales losses.