From affluent consumers to Gen Zs and baby boomers, buy now, pay later (BNPL) continues to gain popularity across markets, enabling consumers across all ages and income levels to acquire goods and services upfront through short-term, often interest-free loans.

Findings detailed in a joint study by PYMNTS Intelligence and Sezzle reveal that the product has a broad appeal across various demographic groups and has become vital to shoppers of all ages. In fact, retailers that do not offer BNPL are at risk of losing sales as nearly half of BNPL users would delay or cancel a purchase or opt for a cheaper product if a merchant did not offer it as a payment method.

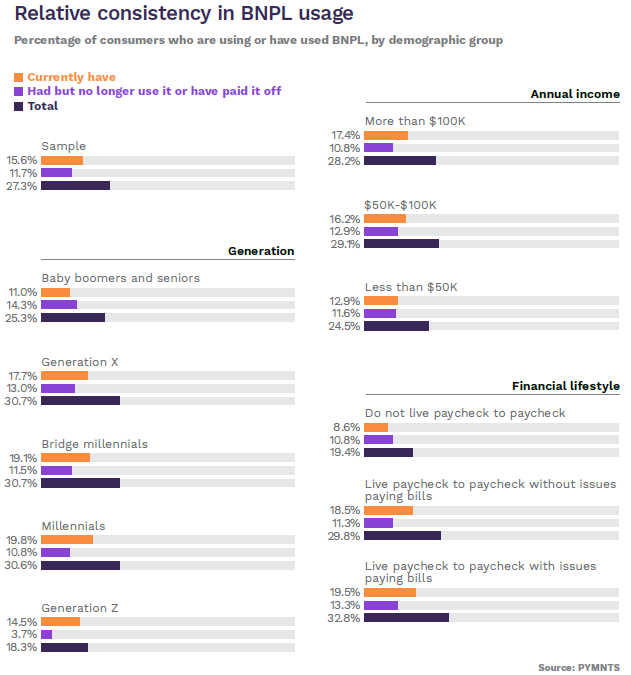

The availability of BNPL goes beyond the decision to finalize a purchase to impact consumers’ product selection. For example, 28% of bridge millennials would opt for a cheaper alternative if BNPL is not offered at checkout, the study shows, suggesting that offering BNPL can increase the chances of merchants selling higher-value products to customers who are less inclined to compromise on their desired purchase when this payment option is accessible.

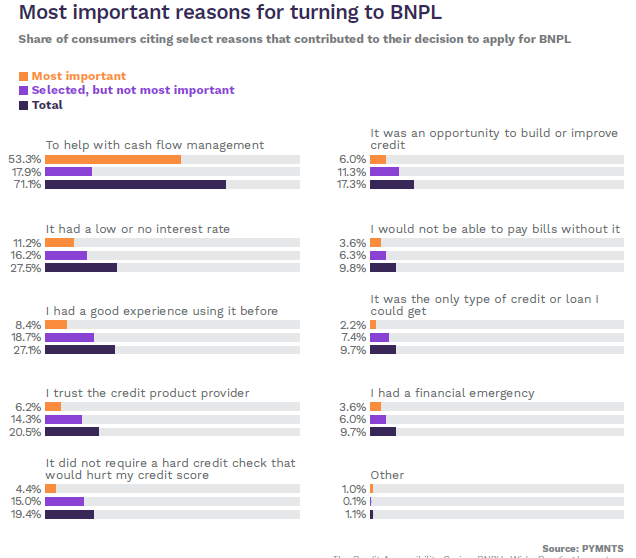

BNPL has also been instrumental in helping users manage their cash effectively — the primary reason why 53% of BNPL users choose this payment method. “Similarly, 17% of BNPL users said the most important reason for their choosing BNPL to pay for purchases was to preserve their cash cushion,” the report noted, an increasingly important option for consumers, especially the more than 60% of Americans living paycheck to paycheck.

In a recent conversation with PYMNTS, Sezzle CEO Charlie Youakim touched on this trend, explaining that BNPL now serves as a “budgeting tool,” especially for millennials, some of whom might lose 6.5% of their spending power as student loan repayments resume next month.

In today’s U.S. financial landscape, having a good credit score is critical and can often be the only thing standing in the way of being approved or denied for a mortgage, auto loan or student loan.

Here too, BNPL can provide value, especially for consumers looking to better position themselves to access lower interest rates and better borrowing terms.

Findings captured in another PYMNTS-Sezzle report show that BNPL can help consumers enhance their credit scores — an advantage not known to the more than two-thirds of consumers who have a shaky understanding of how the credit reporting system works.

As the report noted, a better understanding of how credit works and how to leverage products like BNPL to their advantage can “enable credit insecure consumers to access safer tools to cope with financial strain and even reverse some of the negative credit spiraling that is so common.”

And it seems these consumers are starting to recognize its value, according to a research study by the Federal Reserve Bank of New York, which shows that BNPL payment plans are more likely to be used by U.S. consumers with lower credit scores, per a Tuesday (Sept. 26) Bloomberg report.

Moreover, although credit scoring models do not yet use BNPL transactions, “bureaus are beginning to include BNPL in personal credit records, and it could be a matter of time before the scoring models catch up,” the PYMNTS report added.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More