“Paycheck to paycheck” refers to a situation where an individual or household relies on their regular paychecks to meet their expenses and financial obligations, with little or no savings left over. This means that if something unexpected happens, such as a car repair or medical emergency, they may not have the financial resources to cover the cost and may have to borrow money or go into debt to pay for it.

Living paycheck to paycheck can be stressful and make it difficult to save for the future or make long-term financial plans. It can also make it harder to weather financial setbacks, such as job loss or a reduction in income. If you find yourself living paycheck-to-paycheck, there are steps you can take to improve your financial situation and build up a cushion of savings. These might include creating a budget, reducing expenses, increasing your income, and setting aside a portion of each paycheck for savings.

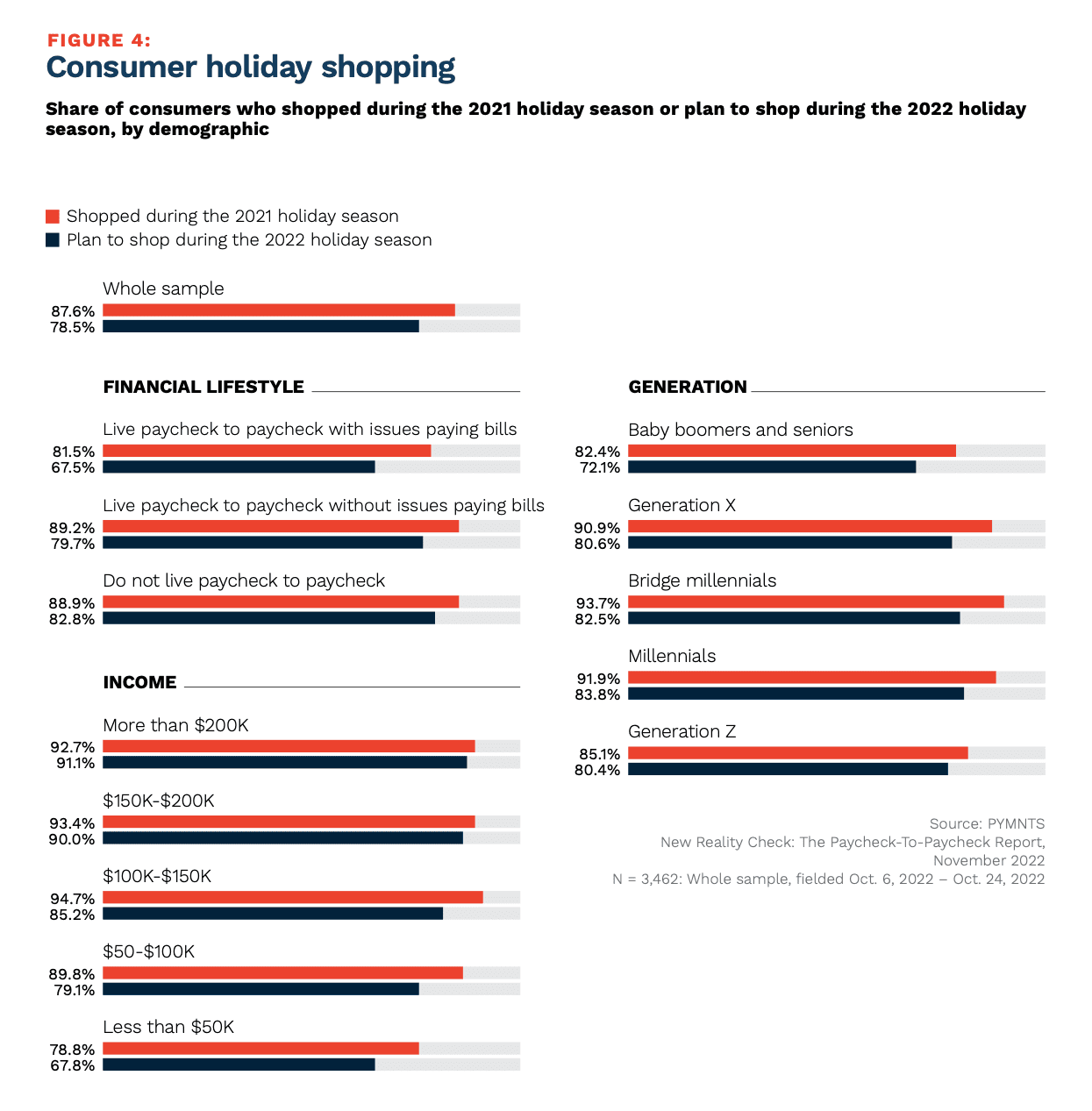

According to a survey of over 3,400 U.S. consumers for PYMNTS and LendingClub’s “New Reality Check: The Paycheck-To-Paycheck Report: Holiday Shopping Edition,” we found that as holiday shopping approached its peak, 15 million consumers who shopped for holiday gifts in 2021 did not plan to do so this year. While 79% of consumers still planned to shop for the 2022 holiday season, that figure was down about 10% from 2021.

The reality of paycheck-to-paycheck living affects differently households and consumers in vastly different ways, with those saying they are struggling to pay bills also reporting a sharp 14-percentage-point drop in plans to shop for the holidays this year. At the same time, paycheck-to-paycheck households that aren’t struggling to pay saw a 10-percentage-point drop in their shopping intentions versus a year ago.

New Reality Check: The Paycheck-To-Paycheck Report: Holiday Shopping Edition

Financial Wellness Remains Out of Reach

The latest report in the series, “New Reality Check: The Paycheck-To-Paycheck Report: Financial Goals Edition,” looks beyond holiday shopping headlines to the longer-term desire of struggling consumers to steady their economic ship.

It’s a long road for many, as the study states that “57% of paycheck-to-paycheck consumers think high inflation has diminished their capacity to reach their long-term financial goals. Compared to a year ago, 32% of all consumers reported a decrease in the portion of their paycheck they can save, while 42% of consumers living paycheck to paycheck with issues paying bills say the same.”

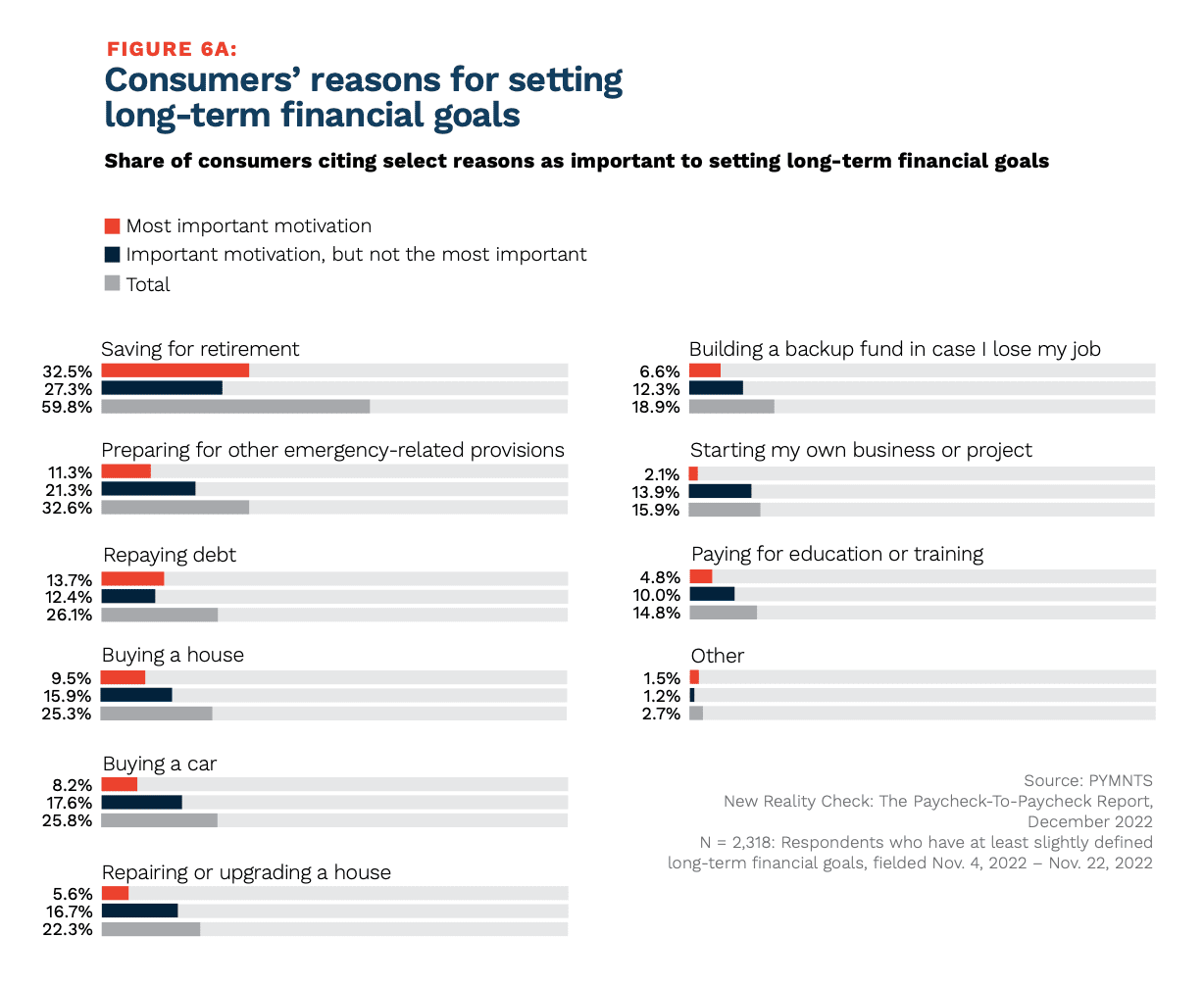

Paycheck-to-paycheck consumers tend to think in along the lines of short-term and long-term financial goals. For example, the most common motivation for setting short-term financial goals overall is paying for a trip or vacation, cited by 49% of consumers, but just 17% say it is their most important reason.

New Reality Check: The Paycheck-To-Paycheck Report: Financial Goals Edition

Trends and Implications

It is difficult to provide a specific trend for paycheck-to-paycheck consumers, as this group may encompass a wide range of individuals with different financial circumstances and habits. However, it is generally understood that living paycheck to paycheck, or having little or no financial cushion, can be a precarious financial situation. It can be difficult for individuals in this situation to save for emergencies or unexpected expenses, and they may be more vulnerable to financial setbacks such as job loss or unexpected bills. Some individuals may be able to break the cycle of living paycheck to paycheck by increasing their income, reducing their expenses, or both. Others may need to seek outside help, such as through financial counseling or government assistance programs, to improve their financial stability.

Living paycheck to paycheck and having little or no savings can have a number of economic implications, both for individuals and for the economy as a whole.

For individuals, living paycheck to paycheck can make it difficult to save for emergencies or unexpected expenses, which can lead to financial instability and vulnerability. For example, if an individual has no savings and experiences a sudden loss of income, such as through a job loss or medical emergency, they may have difficulty paying for basic necessities such as rent, food, and utility bills. This can lead to financial hardship and even poverty.

For the economy as a whole, the prevalence of paycheck-to-paycheck households with little or no savings can have negative consequences. These households may be more likely to borrow money or rely on credit to make ends meet, which can lead to debt and financial strain. This, in turn, can reduce consumer spending and potentially have a negative impact on economic growth. Additionally, the lack of a financial cushion among these households may make them more vulnerable to economic downturns or other economic shocks, which can further affect the economy.