Buy now, pay later (BNPL) has emerged as a popular credit option, enabling consumers to make purchases immediately but pay for them in smaller installments over time.

This flexibility has revolutionized shopping experiences, offering convenience and greater control over spending.

In “The Credit Accessibility Series: BNPL’s Wide-Ranging Impact on Consumers and Merchants” report, PYMNTS Intelligence drew on a survey of over 3,100 consumers to assess the rising popularity of BNPL products as a credit option, consumers’ reasons for choosing to use it, and the potential of BNPL to improve their credit profiles.

The survey results indicated that BNPL has garnered a broad appeal, with consistent use across various demographic groups. In early May, 16% of consumers overall used the product, while an additional 12% had used it in the past.

The data showed that BNPL adoption varies across demographics, with millennials at 20% use and baby boomers at 11%. This potentially reflects the latter group’s more prudent spending habits, notably among those on fixed incomes. Additionally, this contrast might be attributed to the nature of interest-free loans, acting as a bet on the borrower’s future financial capacity. Millennials, being in their peak earning phase, might be more inclined toward BNPL, unlike baby boomers and seniors who are not in the same earning stage.

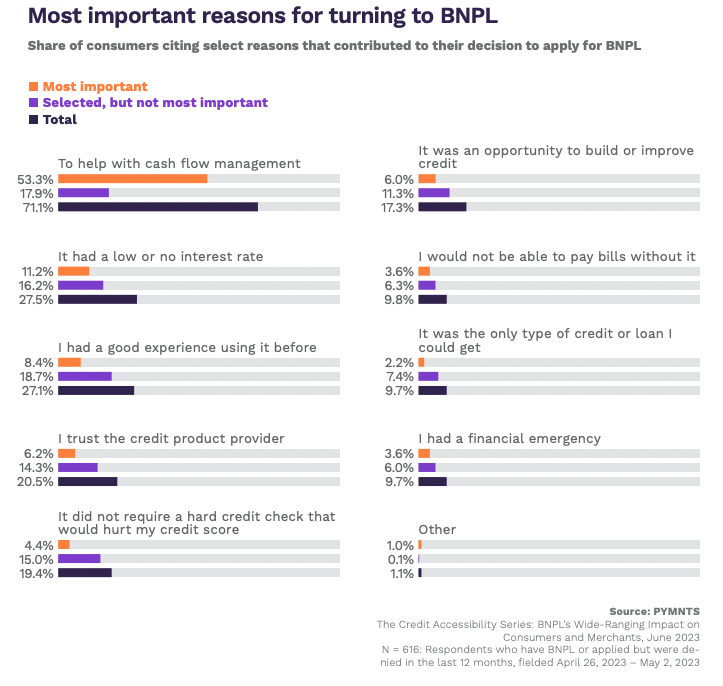

When it comes to important reasons for using BNPL, preserving cash and effectively managing credit lines are top priorities. More than 50% of respondents said managing their cash flow efficiently was the most important reason they opted for BNPL, while an additional 18% acknowledged it as a significant factor, although not the primary one.

Breaking down payments into affordable installments gives consumers control over the timing of their expenses while maintaining a cash buffer and access to credit lines.

“In an uncertain economic environment with high inflation, accessing credit payment options that most effectively preserve cash is likely to become increasingly important for consumers, especially those who live paycheck to paycheck,” the study explained.

The opportunity to enhance credit scores also serves as a motivating factor for some consumers to opt for BNPL. As the study revealed, one-third of BNPL users believed that using this payment method positively influenced their credit scores, although BNPL transactions are not directly factored into credit scoring models.

Moreover, nearly 30% of survey respondents indicated that the low or nonexistent interest rates contributed to their decision to apply for BNPL. Another 19.4% pointed to its lack of impact on their credit score, as it didn’t necessitate a hard credit check, as a motivating factor. Additionally, approximately 10% each cited reasons such as the inability to cover bills without this payment method, it being the sole accessible credit option, and encountering a financial emergency as contributing factors influencing their decision to opt for BNPL.

Nearly half of respondents stated that they would either postpone or cancel a purchase or opt for a cheaper alternative if BNPL were not available, highlighting the significance of merchants offering BNPL as a payment option to prevent cart abandonment and encourage customer spending, especially on higher-priced items.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More