Split-payment plans, or installment plans as they are more popularly called, have gained momentum in the consumer commerce space in recent years.

These plans — not only general-purpose card plans but also split-payment plans that use merchant or store cards and buy now, pay later (BNPL) — have become increasingly popular as customers look for more convenient and flexible payment choices.

This has not only changed how people handle their finances, but it has also led to a major change in the strategies employed by merchants, who have had to work to meet increasing consumer demand for a range of installment plans.

The PYMNTS Intelligence study “Unpacking Merchant Strategies and Consumer Demand for Flexible Payment Plans” drew from a survey of 100 merchants and 50 firms to examine merchants’ current support of, and interest in, offering various installment plans and the challenges merchants face in a rapidly evolving retail landscape.

According to the study, 6 in 10 consumers used an installment plan last year, with the majority favoring plans linked to general-purpose credit cards provided by various banks. Around one-third of merchants accommodated these consumer preferences by offering some form of installment plan in their checkout process.

The study also revealed that merchants offering installment plans reported higher consumer satisfaction, with rates for general-purpose credit cards hitting 44% and BNPL plans reaching 55%. About half of retailers also reported that accepting both kinds of payments boosted sales.

Additionally, more than 60% of merchants said payment processing was more transparent when using general-purpose credit card installment plans, and 56% reported that delinquencies decreased. These findings imply that split-payment schemes are not just contributing to business growth but enhancing customer loyalty and operational security.

According to 48% of retailers, providing general-purpose credit card payment plans further reduced declined transactions by 39%, while 48% said it had a similar effect on BNPL offerings.

“Overall, merchants see almost six benefits from offering general-purpose split-payment plans, compared to 2.4 inhibitors — not all that much more than the 2.1 inhibitors reported by those offering BNPL for the same number of benefits,” the study noted.

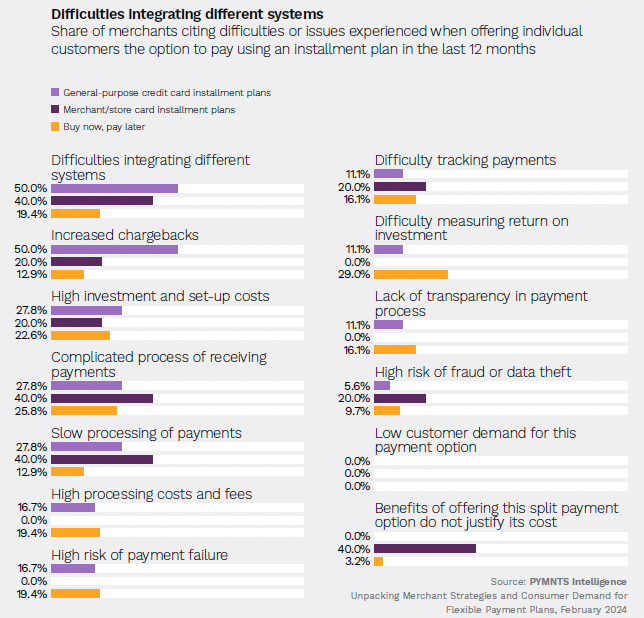

But while merchants largely recognized the advantages of offering split payment plans, the data revealed that might have faced various challenges when implementing these options.

Half of surveyed merchants reported that general-purpose card installment plans led to increased chargebacks, directly impacting their costs. Similarly, other split-payment alternatives, including merchant or store card plans and BNPL options, also contributed to additional chargebacks, albeit less prominently, with rates of 20% and 13%, respectively.

Difficulties integrating different systems was another challenge for 50% of merchants offering general-purpose card installment plans. Fewer merchants reported this problem with merchant or store card plans and BNPL, at 40% and 19%, respectively.

Furthermore, 40% of merchants highlighted the complex payment-receiving process and slow processing associated with merchant or store card installment plans, whereas merchants offering BNPL cited challenges of measuring return on investment as their primary concern.

As consumers continue to embrace flexible payment solutions, the study suggested that “proactive data utilization — especially in apparel, where more than 70% of retailers report customers have used installment plans in the last 12 months — will enable firms to anticipate and meet evolving consumer needs effectively.”