Inflation may be cooling but it still pressures consumers.

And, as PYMNTS has found in recent months, individuals are turning more frequently to their credit cards to meet the demands of paying for everyday expenses.

To get a sense of the magnitude of that shift, consider the fact that one-third of United States cardholders increased their credit card spending in the last six months, with the higher cost of living fueling this trend.

But there are significant gaps between credit use and credit accessibility — namely, credit simply is not available to all who might wish to obtain it, use it responsibly and advance along their financial journeys in a virtuous cycle that benefits consumers, the businesses they frequent and lenders.

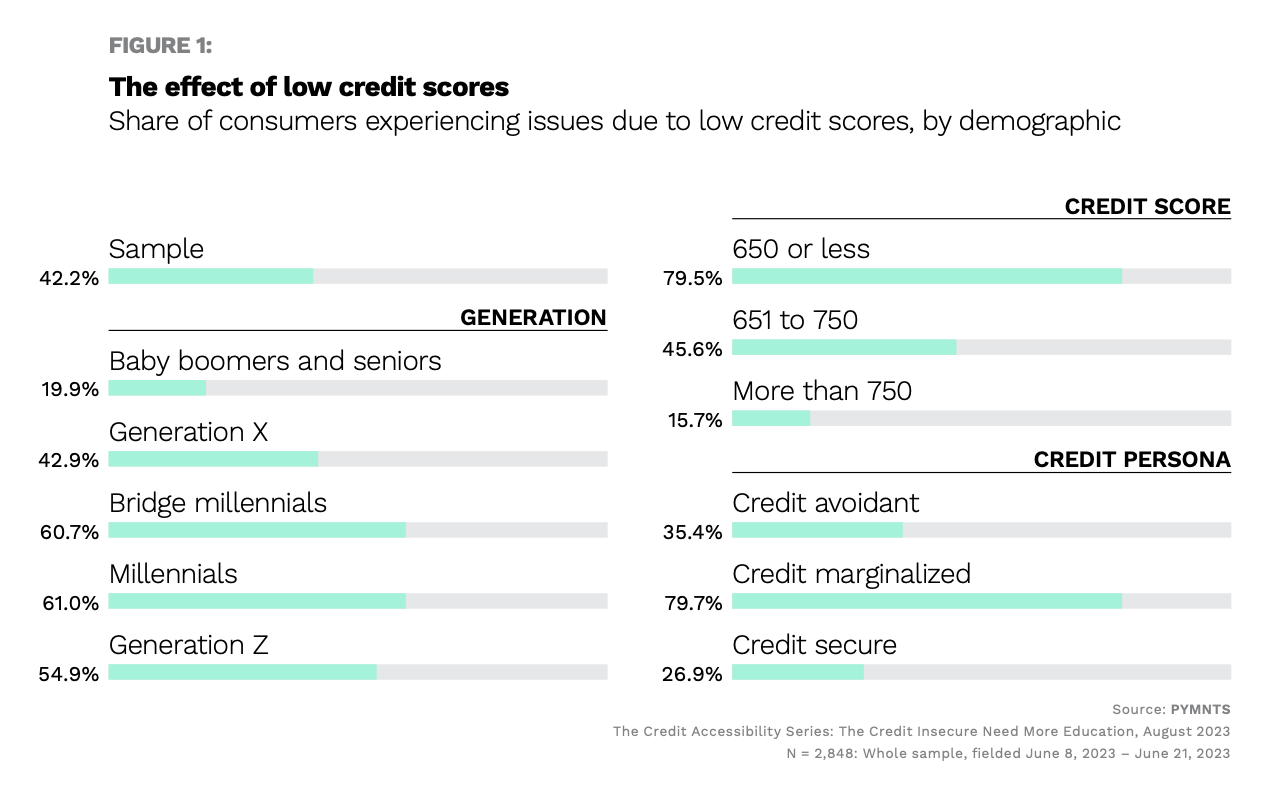

In collaborative research done between PYMNTS and Sezzle documented in “The Credit Accessibility Series: BNPL’s Wide-Ranging Impact on Consumers and Merchants,” we found that 42% of individuals surveyed said that they’d been experience issues — i.e., affording the goods and services they need — because of low credit scores. Of those surveyed, 80% said they had directly experienced financial hardship.

Positive Ripple Effects

Getting a bit more granular, as seen in the accompanying chart, of the consumers experiencing hardship, a majority, about 79%, were in possession of scores below 650 — and that credit score level is a hallmark of younger generations such as millennials and Generation Z. These demographics are the customers that merchants, financial institutions (FIs) and other enterprises will want to cement relationships with, because they conceivably have decades of spending ahead.

But a full 79% of the overall sample adversely affected by relatively low credit scores are credit marginalized, with roughly a third of the population credit avoidant — meaning they’re pretty much discouraged from applying for credit at all.