Advice on planning for the financial future may be of use to more than just younger generations.

As some baby boomers and others getting ready to leave the workplace are unfortunately finding out, retirement is just a concept without the funds to back the lifestyle up. Pensions in the U.S. are largely a thing of the past, and 401(k)s are having a rocky moment as the markets shift wildly in response to inflation, crypto scandals and bank meltdowns. And while Social Security seems solid for the time being, it was never meant to be more than supplemental income for retirees and should not be counted on for principal support.

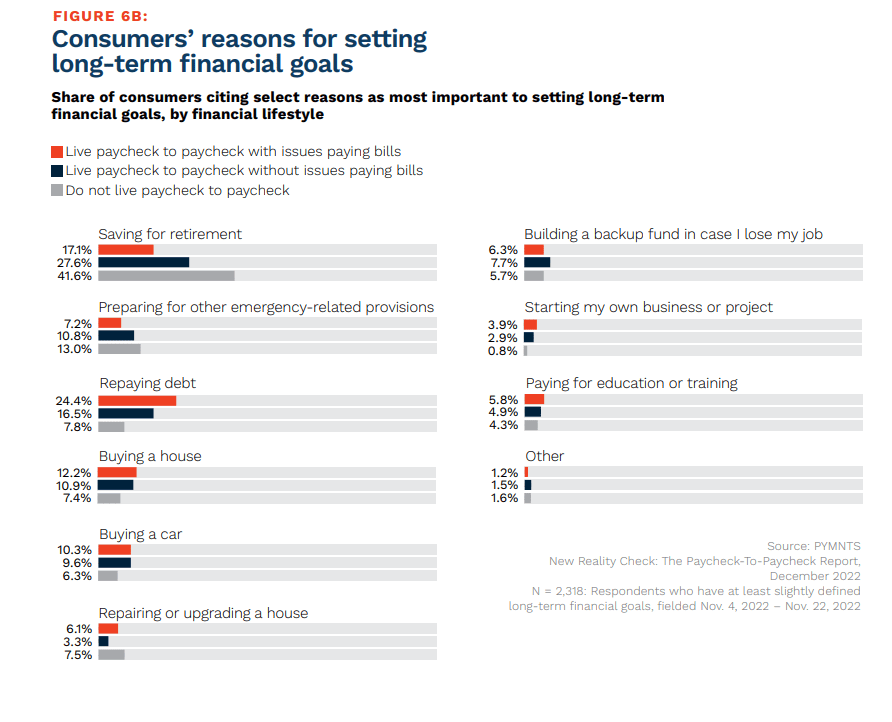

PYMNTS’ research found disparities in retirement planning by consumers with differing financial lifestyles in its collaboration with LendingClub, “New Reality Check: The Paycheck-To-Paycheck Report: The Financial Goals Edition.” Of overall surveyed consumers, 33% say saving for retirement is their most important goal, with another 27% citing retirement as an important motivation, if not the most pressing. However, these numbers dramatically shift analyzed by financial lifestyle.

Although 42% of consumers not living paycheck-to-paycheck are saving for retirement, that share drops heavily (to 28%) for those living paycheck-to-paycheck without issues paying bills. More concerningly, those numbers fall even further when it comes to paycheck-to-paycheck earners with bill pay issues, all the way to 17%.

Have the majority of paycheck-to-paycheck earners simply given up on retirement? Have they decided to delay saving for this long-term financial goal during the current economic volatility? It cannot be determined fully from hard numbers alone.

It may be reasonable, however, to assert that a portion of these consumers may simply not know how to start saving for long-term financial goals amid short-term bill pay pressures. With only 4% of Americans demonstrating basic financial literacy, it stands to reason that at least some portion of the remaining 96% may be preparing to leave the workplace. Banks and credit unions considering the loyalty benefits of providing consumers with financial literacy tools may want to ensure they include retirement planning help in their offerings.

Although all primary financial institutions have the opportunity to provide their customers with these tools, credit unions may be especially well positioned to help. With much of their growth strategy based around the pledge to support members’ financial health, credit unions have long held a reputation as beneficial sector players. The proof is in their members’ enthusiasm, with 90% of credit union members agreeing their institutions make it easy to manage their finances.

Banks and credit unions can’t wave a magic wand and fix their customers’ finances. However, offering tools intended to empower consumers in setting long-term goals that would otherwise fall by the wayside may help — no matter what those goals may be.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More