The steady share of consumers living paycheck to paycheck despite continued economic headwinds is a testament to their fortitude.

Month after month, headlines reaffirm what consumers already know: Inflation on essentials such as food has been straining wallets across income demographics. No one seems safe these days, as over half of earners making over $100,000 per year now report living paycheck to paycheck (although they tend to fare better than other income brackets). Perhaps reflecting this reality, consumer sentiment has slipped, primarily attributed to consistently high prices on everyday goods.

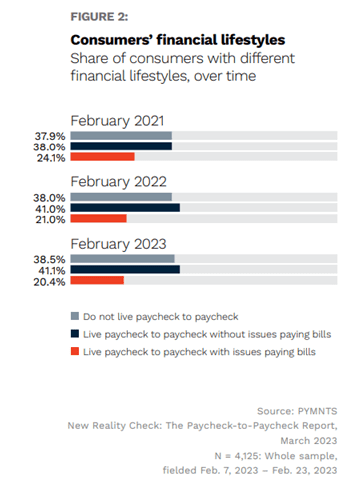

So when the latest PYMNTS collaboration with LendingClub, “New Reality Check: The Paycheck-to-Paycheck Report,” exhibited the ratio of consumers with each of three financial lifestyles, the consistency stood out.

While there is some variability in exact numbers of those living paycheck-to-paycheck, both with and without issues paying bills, the percentages haven’t shifted nearly as much as one might expect. The most notable slight tweak is positive: The share of consumers living paycheck-to-paycheck with issues paying bills has dropped nearly 4 percentage points between 2021 and 2023, raising the rate of those without bill pay issues almost accordingly.

The burning question, then, is how are consumers managing? After all, 60% of surveyed renters say high housing costs are negatively affecting their financial health, and retailers are scrambling as consumer spending sinks. The answer, overall: resourcefully.

Essentials have been prioritized as consumers realign their budgets to meet the current economic reality. When it comes to big-ticket items such as furniture, many are waiting for deals and promotional financing or purchasing using installment plans such as buy now, pay later. Alternately, consumers are delaying large purchases altogether. Electronic sales have dropped 3% year-over-year, car sales are at their lowest levels in over a decade and global smartphone purchases have plummeted.

For everyday purchases, consumers across income brackets and financial lifestyles are cutting out extras wherever possible. When it comes to restaurant takeout, 48% of surveyed consumers opt to pick up meals instead of incurring delivery fees. When eating out, 42% of restaurant patrons are trading their go-to spots for eateries offering discounts. As for grocery shopping, 69% of consumers have made changes to their shopping lists in response to rising prices, including embracing private label goods and coupons.

To pay for items big and small as interest rates remain sky high, consumers are pulling back on using credit cards and dipping into their savings to pay bills. Roughly 70% have made compromises on what gets charged, such as cutting out everyday pleasures. When an emergency arises, record numbers are cashing their 401(k) accounts. Over one-quarter of struggling consumers are simply taking on more debt, leading to higher delinquency rates among younger consumers.

This system is not expected to remain as-is indefinitely. Interest rates are expected to level or perhaps decrease, and the cost of essentials may go down as shipping costs drop. As relief could nearly be in sight, consumers and retailers alike may need to be patient just a while longer.