Rising interest rates are making consumer credit card debt an increasingly expensive burden to carry.

With the macroclimate already eating away at their purchasing power and overall financial confidence, consumers are taking steps to adjust their spending behavior and properly and effectively meet the growing challenges of the current economic environment.

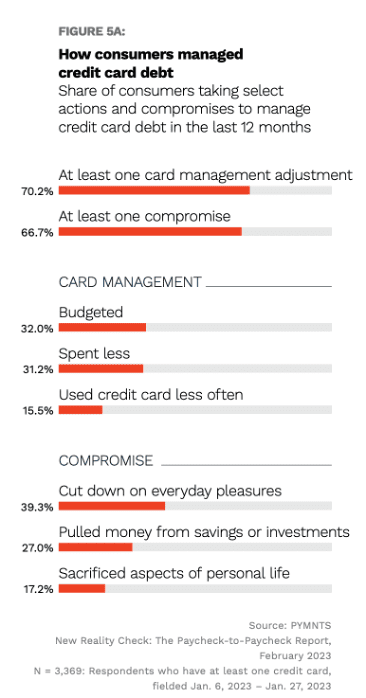

That’s according to 2023 research findings in the PYMNTS report, “New Reality Check: The Paycheck-to-Paycheck Report,” a collaboration with LendingClub, which reveals that roughly 7 in 10 consumers have made at least one card management adjustment (70%), or at least one compromise (67%), to mitigate their credit card debt load in the last 12 months.

Popular card management strategies include taking steps to budget more, which nearly 1 in 3 consumers (32%) tell PYMNTS they’ve done, while separately, 31% say they are spending less.

When it comes to compromises consumers are making in order to reign back their card debt load, nearly 4 in 10 (39%) have cut down on certain everyday pleasures in order to recoup a little financial flexibility, while more than 1 in 4 consumers (27%) have tapped their savings or investments for extra money to manage credit card debts.

The percentage of cardholders reducing everyday pleasures to deal with rising card balances jumps to half (50%) among consumers living paycheck to paycheck who have issues paying bills; and sits at 42% among those living paycheck to paycheck without any issues paying their bills.

Per the report, consumers continue to expect higher-than-average inflation to last until August 2024, making it critical for them to find ways to adjust their behavior to lessen inflation’s impact.

More than 1 in 10 consumers (13%) say the 2022 holiday season increased their debt burden in a way that was either “very” or “extremely” significant.

Still, PYMNTS data shows that fewer consumers expect their financial standing to worsen, an indication that consumers have settled into the new economic environment by adjusting their spending behavior to lessen the impact on bottom lines.

This incremental increase in consumer optimism comes at the expense of discretionary spending.

To learn more about the impact of U.S. consumers’ spending on their credit card debt, and to discover what discretionary items are getting cut in the year ahead as consumers look to change their daily behaviors to stay financially solvent, download PYMNTS’ free 2023 report, “New Reality Check: The Paycheck-to-Paycheck Report.”