Not immune to macro headwinds materializing as inflated costs, reduced savings, and lower investment values, high-income consumers are making lifestyle changes as are others, while still standing apart in some key lifestyle areas.

We see evidence of these changes in PYMNTS data analyzing how consumers at different income levels spend, save, and work. A clear example is how consumers perceive their spending power relative to earnings.

For example, the “New Reality Check: The Paycheck-to-Paycheck Report: Economic Outlook and Sentiment Edition,” a PYMNTS and LendingClub collaboration, found that as of December 2022, over half (51%) of those earning over $100,000 annually said they are now living paycheck to paycheck.

That’s an increase of 9 percentage points from the 42% of high earners who said this in December 2021. Curiously, that same report found that ranks of middle-income consumers (earning $50,000 to $100,000 annually) and those with low-income (earning less than $50,000) did not report a similar increase over the same period, staying relatively flat at 66% and 78%, respectively, as of December 2022.

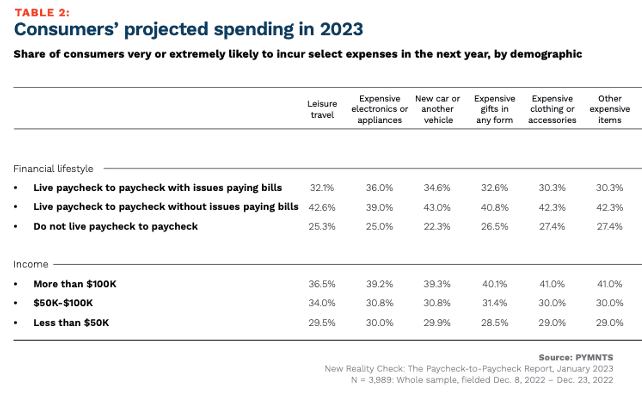

How shifting economic outlooks for earning more will affect spending in 2023 will remain open to question for now. As of this latest sounding, consumers in all income groups plan to travel, and buy home electronics and expensive apparel this year, with those not struggling with bills expecting to spend more on non-essentials like clothes and gadgets.

Our monthly tracking of consumer trends shows that high-income consumers are drivers of the connected economy, based in part on the high percentage of this group still working remotely three years after pandemic lockdowns were declared, and a year after waves of workers returned to offices, stores, and facilities requiring in-person work.

According to the February report “The ConnectedEconomy™ Monthly Report: Digitally Divided – Work, Health and the Income Gap,” high-income consumers are more engaged in the digital connected economy, partly as a byproduct of working from home: “Low-income consumers are increasingly returning to jobs requiring them to work onsite. High-income consumers are now 78% more likely than low-income consumers to have jobs they can perform from home.”

The estimated 45 million consumers still working remotely at least part of the time skew toward high earners, driving up their connected economy participating 10% year over year.

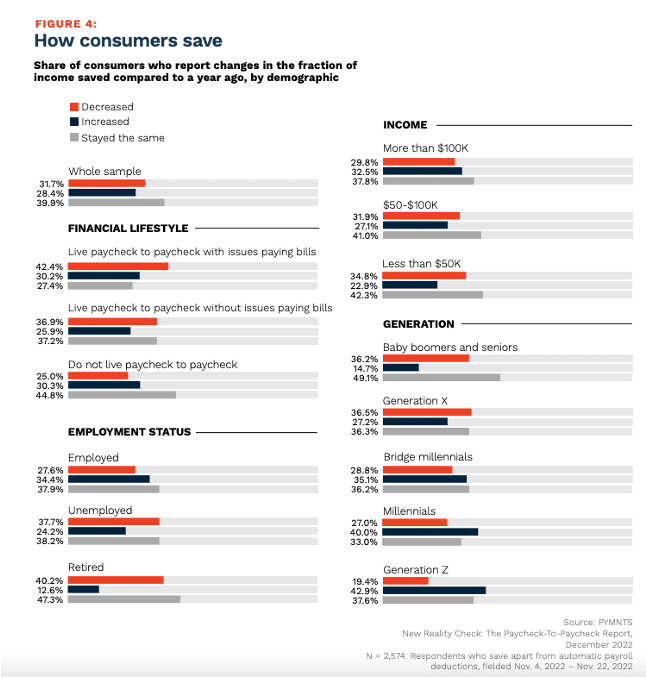

High earners are more likely to have open-to-buy on credit cards despite a year of rampant inflation and higher credit card usage in 2022, but the December edition of “New Reality Check: The Paycheck-To-Paycheck Report” noted shifts in savings patterns.

Per that report, “57% of paycheck-to-paycheck consumers think high inflation has diminished their capacity to reach their long-term financial goals. Compared to a year ago, 32% of all consumers reported a decrease in the portion of their paycheck they can save, while 42% of consumers living paycheck to paycheck with issues paying bills say the same.”

Additionally, of those living paycheck to paycheck without issues paying bills, we found that “37% do not have short-term financial objectives and 40% lack long-term goals. For those not living paycheck to paycheck, less than one-quarter lack clear short-term or long-term financial goals.”

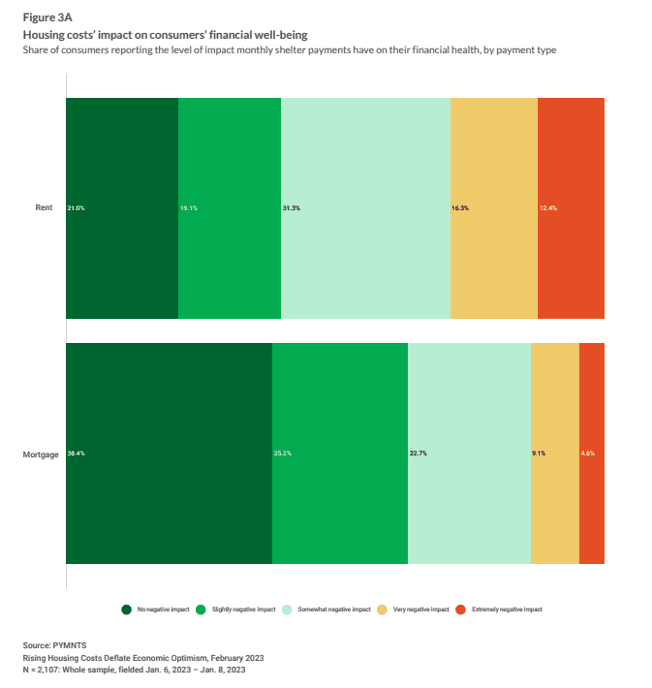

Another area where we observe strong differences between high-income consumers and others is in the impact of housing costs on the perceptions and realities of affordability.

According to PYMNTS’ February report “Consumer Inflation Sentiment: Rising Housing Costs Deflate Economic Optimism,” 60% of renters say runaway rents “negatively influence their financial health, with 29% of renters saying this influence is very or extremely negative.”

However, 63% of mortgage holders — who tend to be higher earners and more financially stable — say mortgage payments “impact their financial grounding only slightly or not at all — a sentiment with which just 40% of renters would agree. Just 11% of high-income mortgagors say housing costs’ impact on their financial well-being is highly detrimental.”

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More