By all accounts, American consumers are feeling the economic strain. More than half of Americans earning less than $50,000 annually are now living paycheck to paycheck, and even 36% of the highest earners — those making more than $100,000 a year — now fall into the paycheck-to-paycheck category. Given consumers’ plight, one would expect financial institutions (FIs) to be stepping up to help.

The reality, however, is that FIs are simply not doing enough. Despite having intimate insight into their customers’ financial situations and behaviors, most FIs are not leveraging this advantage to help distressed consumers. A survey found that 63% of consumers had not received personalized advice or specific communications from their FIs concerning the cost-of-living crisis.

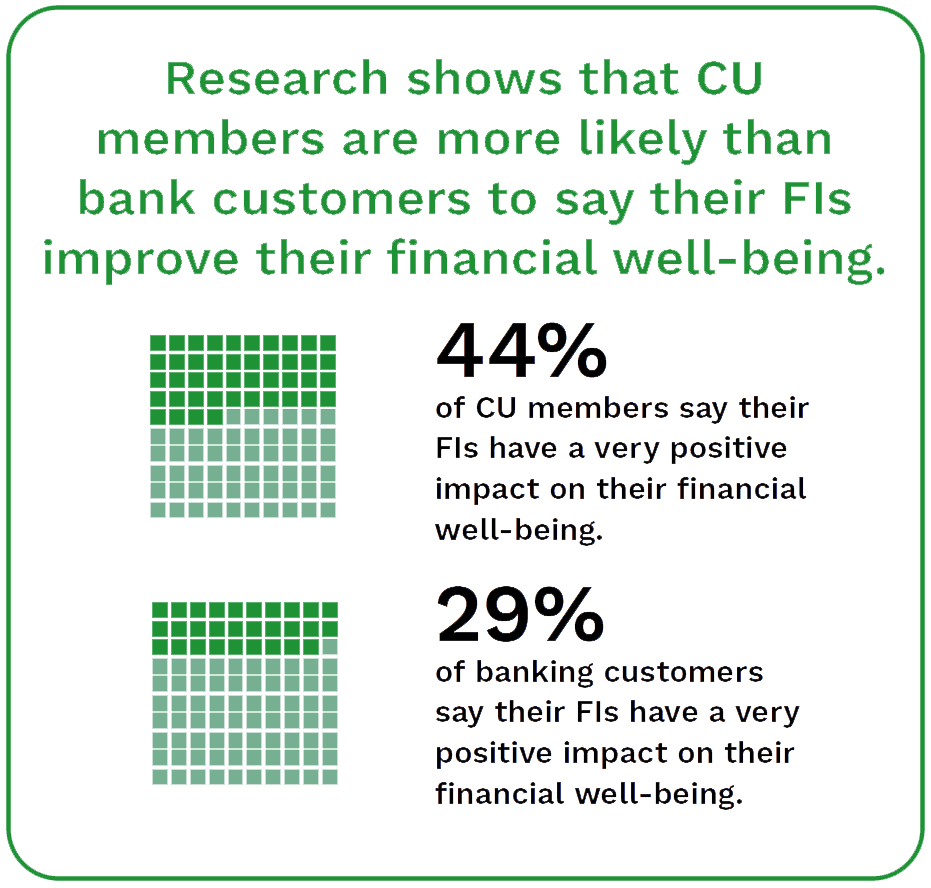

CUs Well-Positioned to Help

Although all FIs have the opportunity to step up their game, credit unions (CUs) are in an especially promising position to help. Premised on the commitment to supporting their members’ financial well-being, CUs already have established themselves as helpful actors in consumers’ lives. For example, 90% of CU members say their institutions make it easy to manage their finances.

Part of the reason CUs can offer such help is that, as noted in PSCU’s “Eye on Payments” 2022 report, CUs have access to data and community connections they can leverage to deploy actionable strategies. These strategies may include surveys to assess members’ financial health, behavior modification alerts and other tools.

Giving Consumers What They Want

To aid consumers, CUs need to understand their needs — and develop products accordingly. First and foremost, consumers want personalization, with eight in 10 CU members wanting to work with a business that knows them personally.

For example, according to a survey from the National Association of Federally Insured Credit Unions, 42% of banking customers want “personalized advice and money management support within their mobile banking app.” The survey also found that consumers are interested in helpful suggestions and alerts related to personal finance. These range from proactive tips on money-saving solutions to tailored suggestions for inexpensive loans. In addition, the survey noted that 26% of consumers are interested in reminders for subscriptions they forgot to cancel.

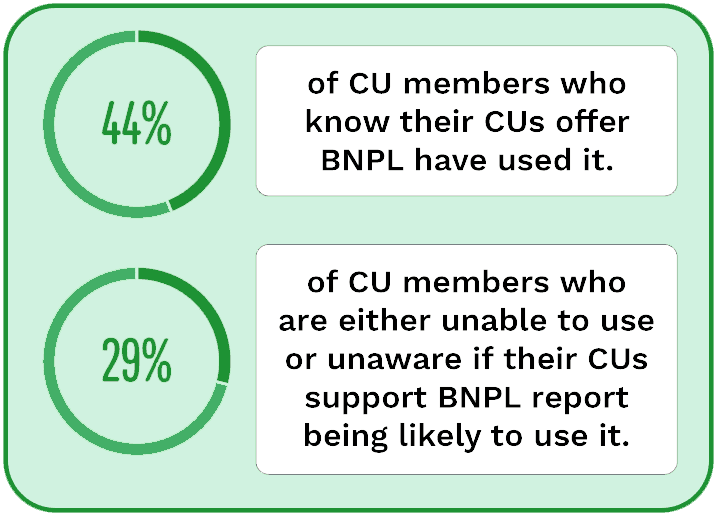

Consumers also want payment choice. PYMNTS data reveals that 66% of CU members are interested in more payment capabilities, up from 60% last year. Given the perilous economic condition, it is more important than ever that FIs help their customers make the purchases they need. Consumers are increasingly interested in buy now, pay later (BNPL) or installment options, for example, to ease their budgets. PSCU data indicates that of those members aware that their CUs offer BNPL functionality, 60% have used it. The same data reveals that of those members who do not know whether their CUs offer it or know they do not, 32% are likely to use it if given the chance — a 39% increase from the year before.