The scoring model FICO ranges from 300 to 850. A “good” score generally is above 670, a “very good” score is over 740, and anything above 800 is considered “exceptional.” If your credit score isn’t good enough to access the conditions you’d like, there are multiple avenues you can take to improve it, such as via credit-builder applications or keeping old lines of credit open. Improving a rate of 100 points may require some effort and planning, but there are potential savings of thousands of dollars in interest rates.

The report “The Credit Accessibility Series: Declining Purchasing Power Pushes Consumers to Improve Credit Scores” is a PYMNTS Intelligence and Sezzle collaboration that explores U.S. consumers’ success in improving their credit scores and key related variables. Here are some of the key tactics analyzed in the report you might consider boosting your credit position.

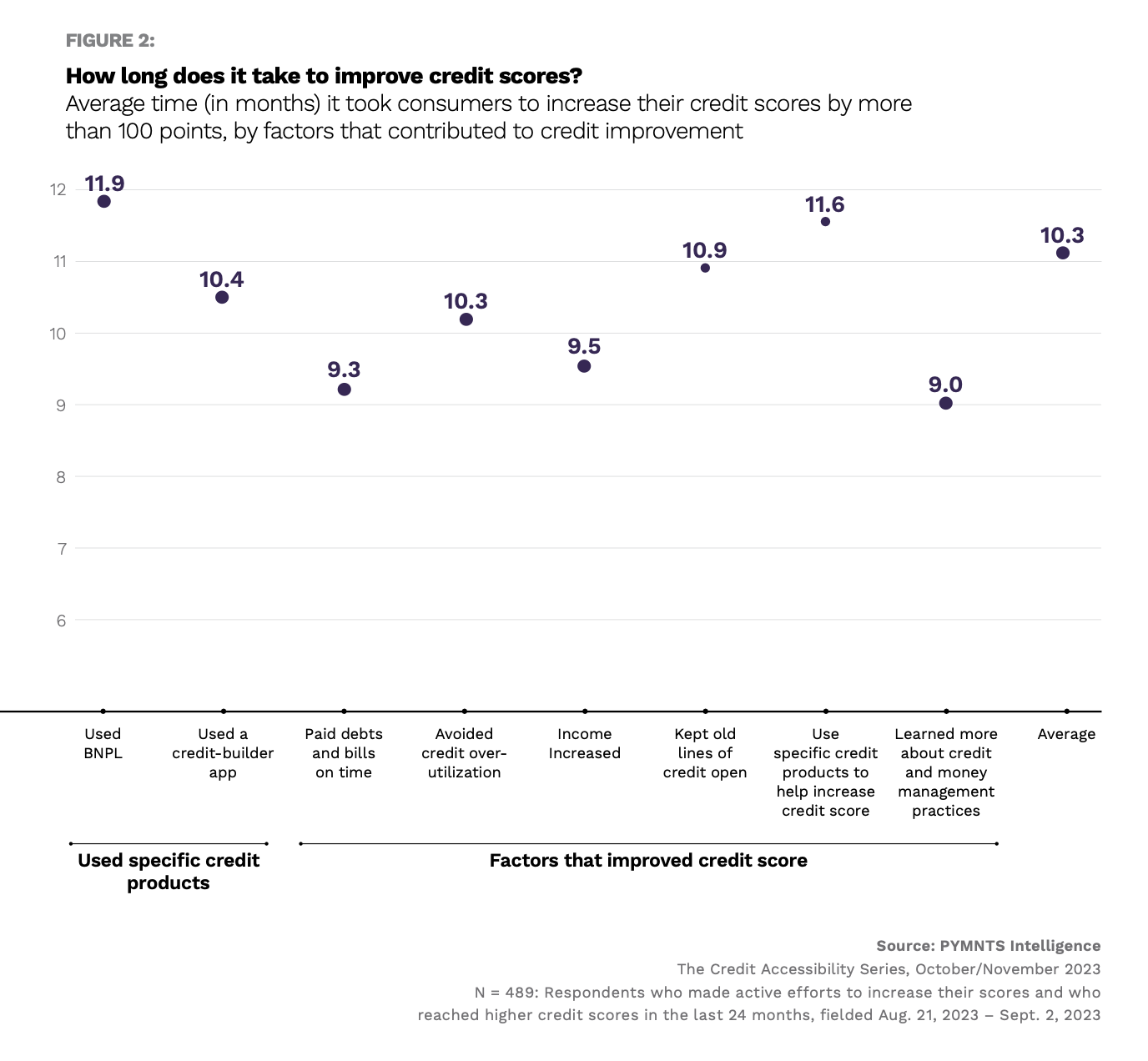

According to the study, the fastest way to increase credit scores by more than 100 points is through learning about credit and money management. Education in this field may help you to combine credit strategies that lead to faster results. Although the average consumer needed from 10 to 12 months to improve their credit score by more than 100 points, consumers who learned more about credit and money management could do it in 9 months, on average.

The second most effective tactic to elevate your credit score is paying your debts and bills on time, even if it’s making the minimum payment due. This is the best way to get your credit score over 800, the highest rate. According to LendingTree’s analysis, 100% of borrowers with a credit score of 800 or higher paid their bills on time every time. Prompt payments make up roughly 35% of a credit score.

The third most important factor, besides an income increase, is to avoid credit-over utilization. On average, consumers following this strategy can experience a 100-point increase in their credit rating in 10.3 months. From mortgages to car payments, having an exceptional score doesn’t mean zero debt but rather a proven track record of managing a mix of outstanding loans. As a general rule, it’s important to keep revolving debt below 30% of available credit to limit the effect that high balances can have.

If your credit score is between 740 and 760, you’re probably already getting the most favorable terms for getting a loan or a mortgage. Reaching a position above that might not be necessary, as there is no practical benefit to scoring any higher. But if it’s below that threshold, every point translates into money. Adopting the most appropriate money tactics depending on your financial profile is key to elevating your credit score and saving money.