Older consumers were able to maintain their purchasing power last year, mainly helped by an 8.7% jump in Social Security benefits that exceeded inflation.

This was the highest increase in four decades, and it allowed seniors to maintain their standard of living despite the high prices persistently impacting consumers. Seniors were able to spend on nonessential items like travel or restaurants and sustain savings.

However, Social Security retirement benefits are slated to increase by only 3.2% this year, which could translate to a slowdown of seniors’ spending power, especially in nonessential categories.

The PYMNTS Intelligence study “New Reality Check: The Paycheck-to-Paycheck Report” examined the impact of nonessential spending on consumers’ ability to manage expenses and put aside savings. Nearly 53% of baby boomers and seniors lived paycheck to paycheck in the United States in November, which is the lowest portion across all age groups. They also reported being more conservative in their spending than other generations, as 12% of them living paycheck to paycheck said nonessential spending influenced their financial lifestyle, while in contrast, 29% of Generation Z said the same.

The study suggested that this age group enjoyed the most financially healthy lifestyle. However, this could now change due to the lower increase in Social Security benefits and the consistently high prices of specific products and services like housing, healthcare, medical equipment and pharmacy items — each a portion of many seniors’ budgets.

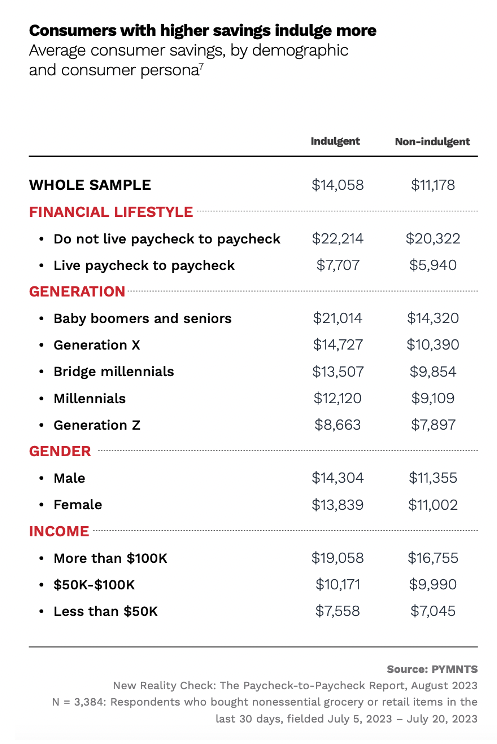

Should these factors lead baby boomers and seniors to dip into their savings to sustain their standard of living, less nonessential spending is likely to follow. The study revealed that consumers generally engage in more indulgent spending when they have more savings. Baby boomers and seniors who engage in indulgent spending have an average savings 47% higher than those who do not engage in such indulgent spending. Baby boomers and seniors who splurge on nonessential items hold savings of $21,014 on average, while non-splurging baby boomers and seniors have savings of $14,320 on average.

The projected smaller increase in Social Security checks this year may lead senior consumers to become more cautious with their spending, especially those in more vulnerable situations. The real impact of this trend, however, remains to be seen.