PYMNTS’ research finds that 83% of consumers made payments for credit products in the last 90 days. Credit, in general, is a significant part of life for most consumers across generations.

Overall, credit use is lower among Generation Z consumers. But PYMNTS’ data shows that millennial and Gen Z consumers are the most likely to have increased their use of credit products in the last year. This increased usage suggests that they may catch up, albeit by using the products that work best for them. In that context, younger consumers’ penchant for buy now, pay later (BNPL) could have massive ramifications for the industry’s future

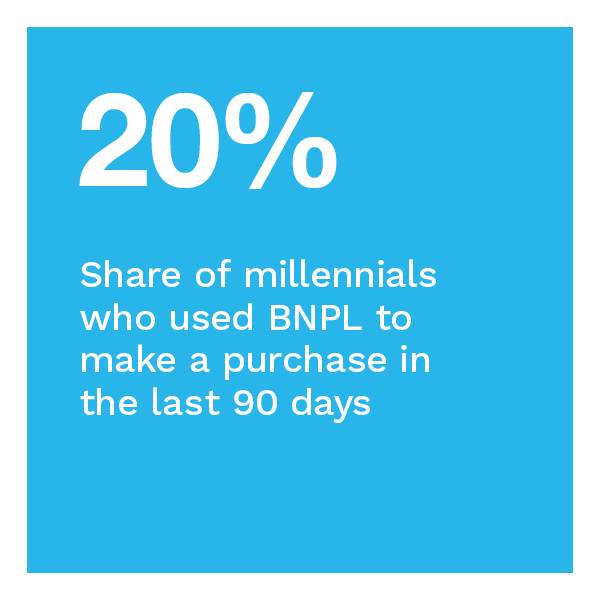

BNPL and credit card use also average the most similar dollar values for millennial and Gen Z demographics. This similarity indicates that these consumers use these products more interchangeably. On the other hand, other consumers primarily use BNPL to pay for big-ticket items. In the three months prior to being surveyed, 20% of millennials used BNPL. Just 5.9% of baby boomers and seniors did the same.

These are just some of the findings detailed in “The Credit Economy: How Younger Consumers Make Credit Decisions,” a PYMNTS and i2c collaboration. This report examines behaviors and attitudes related to credit. We surveyed 3,396 consumers between March 16 and March 21 to explore what drives consumer interest in using credit cards and BNPL for everyday and occasional purchases across generations.

More key findings from the study include the following:

Rewards drive credit card usage for nearly all consumers, but Gen Z diverges by mostly wanting access to a credit product.

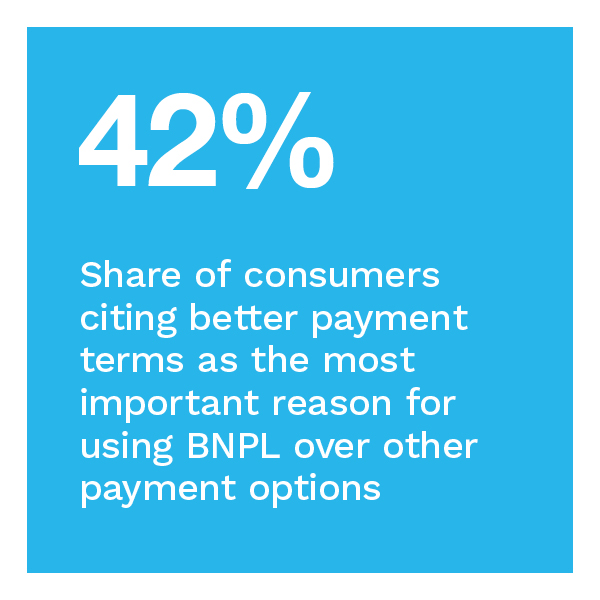

Earning rewards is a key driver of credit product interest and use for consumers of all ages except Gen Z. These youngest consumers’ main interest is getting access to credit to better manage their cash flows. While 47% of credit card holders cite rewards as a reason they use the method, just 24% of BNPL users cite this as an incentive. Factors other than rewards entice consumers to use BNPL, however.

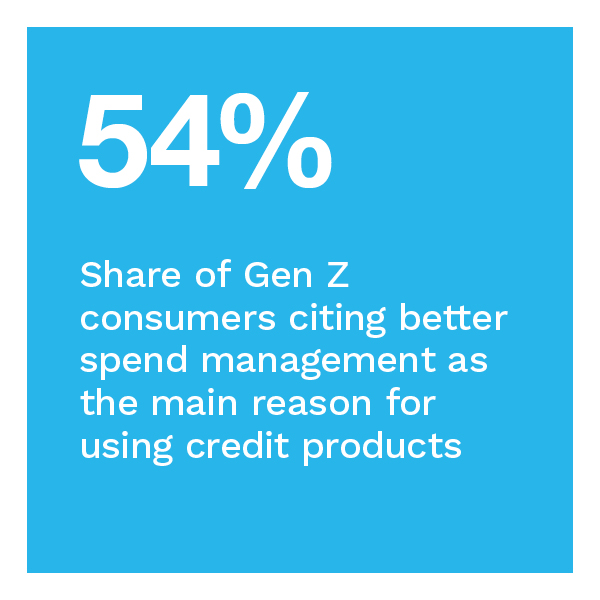

More than half of younger consumers use a credit product for everyday purchases as a way to better manage their cash flows.

Better spend management was a top reason to use credit products for more than half of millennial and Gen Z consumers. Just 38% of baby boomers and seniors said the same. Leading all generations, 42% of millennials increased their use of credit products for everyday purchases in the last year.  Gen Z was next at 30%. Millennial and Generation X consumers are the most likely age groups to use credit products other than cards.

Gen Z was next at 30%. Millennial and Generation X consumers are the most likely age groups to use credit products other than cards.

Fifty-five percent of all consumers now revolve their credit card balances, including those with installment plans linked to cards.

While 45% of all cardholders say they pay off credit card balances every month, one-third say they rarely or never pay balances in full. Baby boomers and seniors are the most likely to pay credit card balances in full, with half saying they do so every month. But paying the balance in full and revolving balances are not the only ways consumers manage their outstanding balances. Thirty-eight percent of all cardholders have installment programs or payments pending on their credit cards, compared to 59% of millennials and 45% of Gen Z consumers.

Important generational differences exist in why consumers use various credit products and at what rates. Download the report to learn more about the trends and nuances of why consumers choose the credit products they do.