National banks dominate the U.S. consumer credit card industry, with a strong position that is unlikely to be challenged anytime soon.

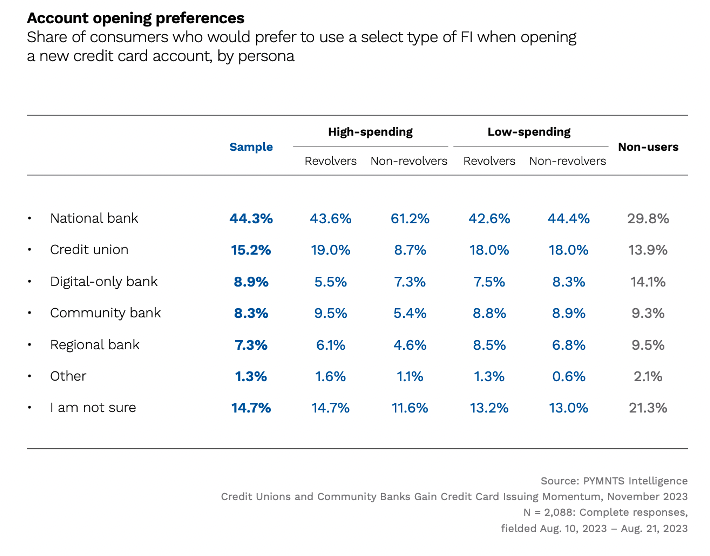

However, smaller financial institutions (FIs) are slowly gaining ground. The study “Credit Unions and Community Banks Gain Credit Card Issuing Momentum,” a PYMNTS Intelligence and Elan Credit Card collaboration, revealed that 15% of overall consumers would most likely turn to credit unions (CUs) for their next credit card application. This share went up to 19% in the segment of high-spending revolvers, consumers paying more than 40% of their expenses by credit card who usually carry a revolving balance between statements. Although this group represents only 10% of all segmented personas, it is one of the most profitable.

CUs saw their share of primary credit cards rise from 6% in 2020 to 8.3% in 2023. In contrast, national banks experienced a decline from 76% to 68% in the same period.

CUs are setting up alliances to continue gaining credit card users. United Community Credit Union, for instance, partnered in October with credit union service organization (CUSO) and FinTech solutions player PSCU, which will provide credit card processing services and support beginning in 2024.

“We look forward to working with United Community to elevate and enhance their card offerings, while also meeting member expectations and needs for years to come in today’s continuously evolving payments industry,” Scott Wagner, chief revenue officer and executive vice president of PSCU, said at the time.

In November, Elan Credit Card announced an agreement with VolCorp, a nonprofit cooperative that works with more than 1,200 FIs across the U.S., to launch a credit card program for credit unions.

“By partnering with Elan, we can now offer a credit card solution to support growth and deeper member relationships,” VolCorp President and CEO Jeff Merry said at the time.

Despite their advances in popularity, CUs still face challenges in attracting clients from specific segments, in particular, high-spending non-revolvers. These are consumers paying more than 40% of their expenses by credit card who rarely or never carry a revolving balance between statements. As revealed in the study, only 9% of this group would likely choose a CU for a new credit card account, representing the lowest share among all the segmented personas.

To compete effectively and further expand, smaller FIs could provide additional services, including rewards programs and split-pay options, two features valued by cardholders.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More