Credit unions, like all financial institutions (FIs), have set their digital innovation agendas to meet consumers’ needs, but consumers’ requirements are constantly changing as the digital-first economy evolves. CU members have been especially eager for digital and remote banking options, but they no longer see digital banking as the emergency stopgap it was at the beginning of the pandemic. Features that were once regarded as cutting-edge have become a given, and members may be tempted to leave their CUs when other FIs beckon with newer — or preferred — innovations.

PYMNTS’ latest research shows that half of all CU members in the United States are more interested in touchless technologies — contactless cards, mobile wallets, card-on-file options and QR code-enabled payments — than they were when the pandemic began. This spike in interest is even more pronounced among digital-first banking generations, such as millennial and Gen Z consumers, who have grown up using connected devices to conduct their daily lives. Many CUs are failing to realize the value their members have come to place on touchless innovations, however — and they often fail to invest in members’ favorites even when they do. Another recent PYMNTS study showed that 44 percent of Gen Z consumers would consider switching FIs because of innovation, so the danger for CUs is very real.

The following Deep Dive examines where CUs are currently missing the mark in meeting their members’ digital wish lists and explains how they can check these boxes to keep members engaged.

The CU Member Innovation Divide

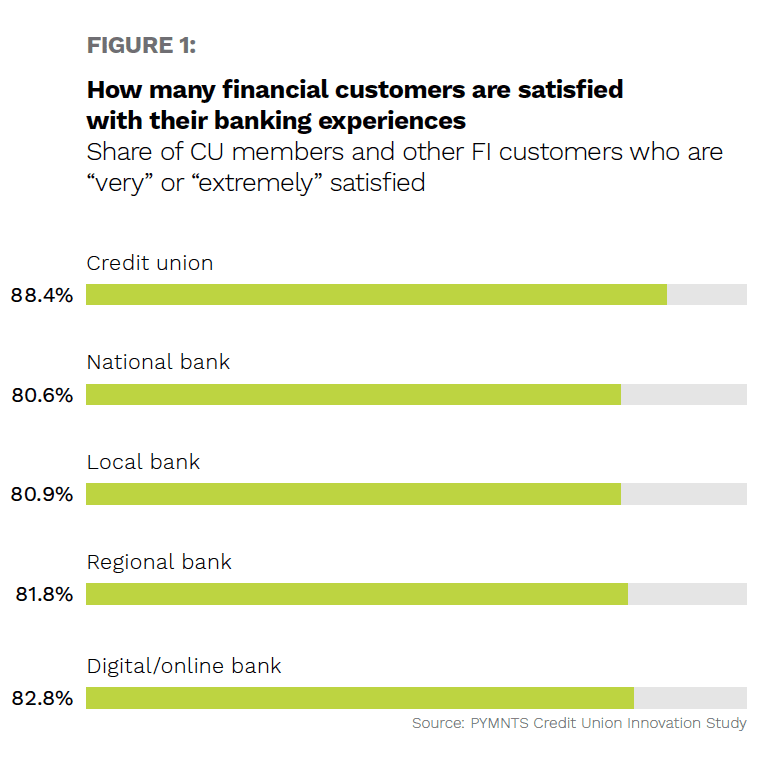

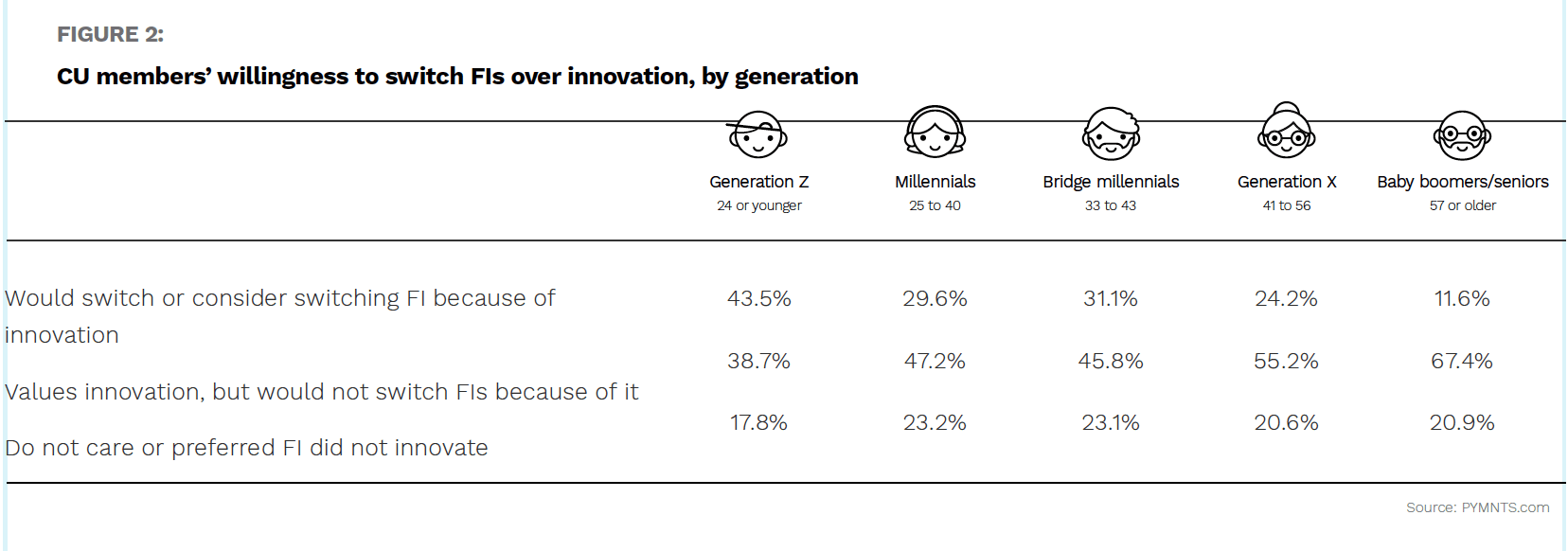

PYMNTS research shows that while credit union members’ satisfaction overall surpasses that of traditional bank customers, one in five would still leave their credit unions for banks that offer greater innovation, with millennials and bridge millennials leading the pack. Failure to innovate is the most common reason members cite for unhappiness with their CUs, in fact, outnumbering their bank and FinTech customer counterparts three to one with this complaint. Credit unions have responded by accelerating the pace of their innovation agendas, with almost 50 percent more saying they beat the competition in launching new products in 2020 than in 2019. There is one problem, however: CUs and their members do not always see eye to eye on the definition of innovative products and services as members often view CUs’ innovations more as basic requirements rather than desired advancements.

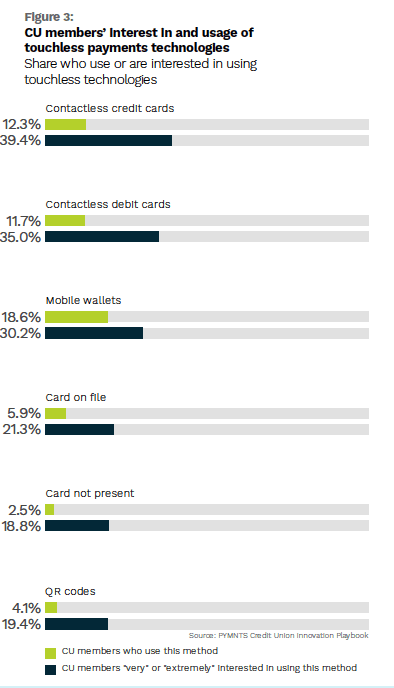

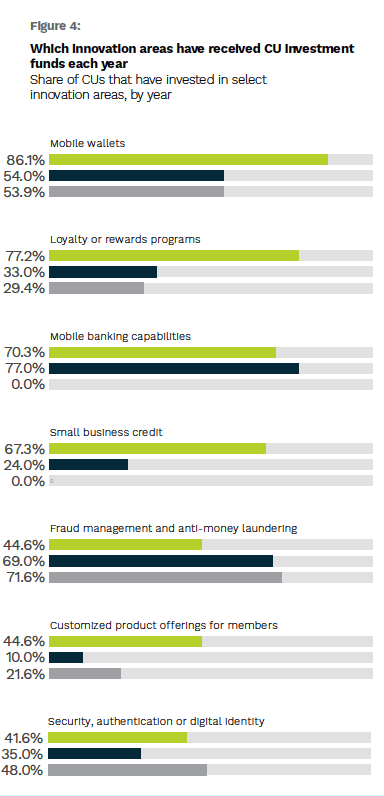

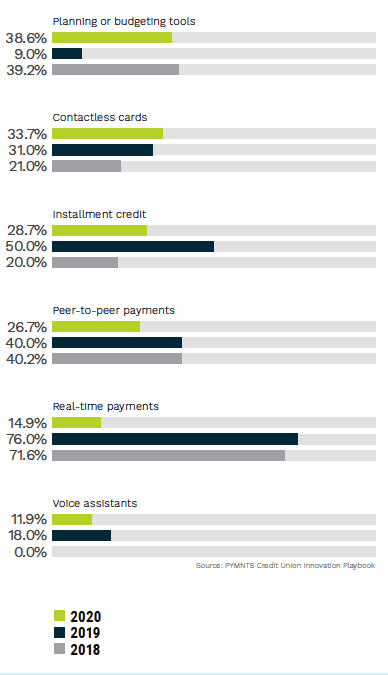

CUs recognize the need to offer their members touchless payment options, but they may get their touchless priorities mixed up, meaning few of their members have access to the touchless methods they actually wish to use. CU members in PYMNTS’ most recent study report contactless credit and debit cards as their top two preferences when it comes to touchless payment options, with 39 percent and 35 percent saying they are “very” or “extremely” interested in using these cards, respectively. Only about one-third as many members as would like to are actually using contactless cards, however, and the method represents only the ninth-most common innovation area in which CUs invested in 2020.

Mobile wallets were CUs’ top innovation area last year, with 86 percent of all CU decision-makers saying they invested in mobile wallet innovations. Only 34 percent of CUs invested in contactless card innovations despite the fact that their members expressed more interest in using contactless cards than in using mobile wallets.

Getting Innovations Right

The divide between the innovations in which CUs are investing and the ones members actually want offers fertile ground for sowing the seeds of member discontentment and potential abandonment. PYMNTS research indicates that 15 percent of CU members would be “very” or “extremely” likely to leave their current CUs to bank with competitors if the latter offered touchless payment options — presumably the ones they wish to use — with an additional 21 percent being “somewhat” likely to switch FIs for touchless payments.

The risk that CUs could lose members over these innovations is realistic because many FinTechs are innovating the very touchless methods CU members want to use, often with the full intention of selling these options to them. Sixty-four percent of FinTech executives say they would be “very” or “extremely” likely to circumvent their bank and credit union clients to sell touchless payment features directly to end users. CUs are thus in an innovation race against FinTechs for touchless payment capabilities whether they realize it or not.

Enabling specific touchless payment innovations will thus be key to attracting and retaining members — particularly those in younger, more digitally savvy age groups — going forward, and CUs should act on this knowledge with a swift but methodical approach. This begins with opening up a dialogue with members to learn which innovations interest them and following through with investments. It is important for CUs to invest in a wide assortment of these capabilities, however, and avoid putting all their eggs into one basket. CU members may be more interested in contactless credit and debit cards than other touch-free payment experiences right now, but diversification of investment can help ensure that CUs can pivot to meet their members’ needs should they shift again in this rapidly changing digital ecosystem. CUs can also seek help from third parties, such as CUSOs, to strategize and obtain ways to speed their innovations to market without risking losing their members to FinTechs. CUs should keep the dialogue with their members open and inform them of their innovations’ progress to ensure members are aware of their options and can make the most of any innovations as they roll out.

Credit unions have an opportunity to keep and grow their memberships in key demographics by providing the right digital banking tools — or risk losing members if they do not.