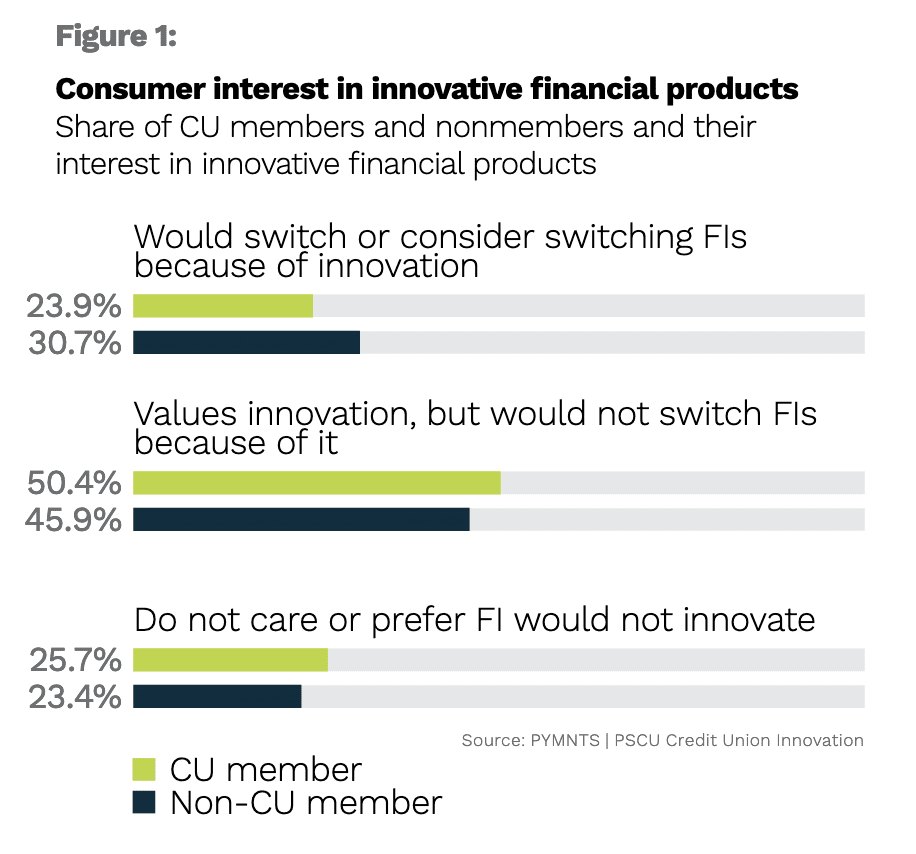

Indeed, about one-quarter of credit union (CU) members said they would be willing to leave their CUs for competitors if those competitors could offer more innovative products, according to “Credit Union Innovation,” a PYMNTS and PSCU collaboration based on a survey of 6,483 U.S. financial institution (FI) account holders, 151 credit union executives and 50 FinTech executives.

Get the report: Credit Union Innovation

CU members are less likely to switch than other financial customers, however. The survey found that while 24% of CU members would switch or consider switching FIs because of innovation, 31% of non-CU members would do the same.

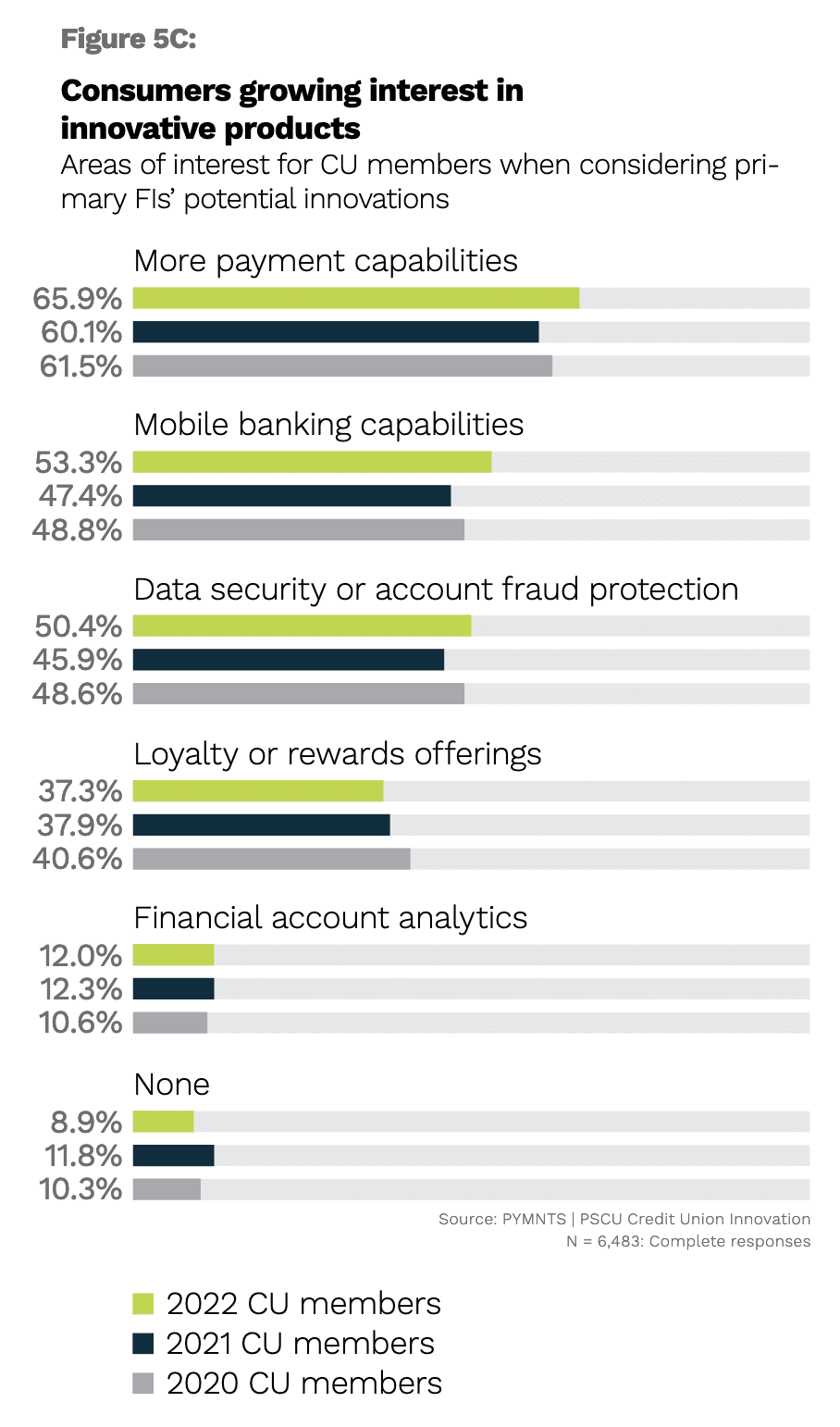

The top innovation that CU members and other financial customers want their FIs to invest in is more payment capabilities, including real-time payments, cardless cash withdrawal and contactless payments.

The top innovation that CU members and other financial customers want their FIs to invest in is more payment capabilities, including real-time payments, cardless cash withdrawal and contactless payments.

Among CU members, 66% are interested in more payment capabilities.

Other top-five innovations that CU members want their FIs to invest in are mobile banking capabilities, data security or account fraud protection, loyalty or rewards offerings and financial account analytics. These potential innovations were cited by 53%, 50%, 37% and 12%, respectively, of CU members.

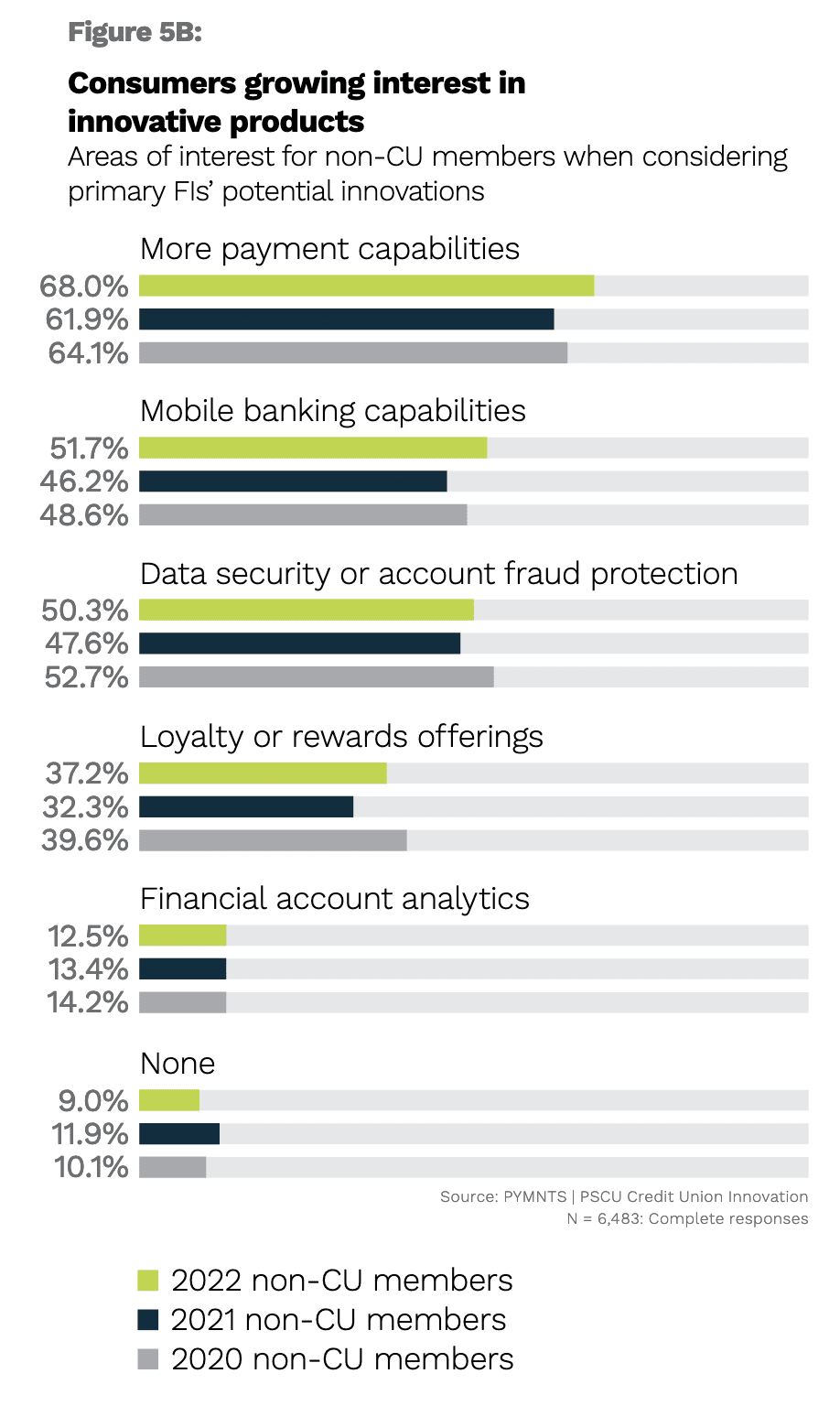

Other, non-CU financial customers rank those top-five areas of interest in the same order, but with different shares of customers selecting each.

Other, non-CU financial customers rank those top-five areas of interest in the same order, but with different shares of customers selecting each.

Among non-CU financial customers, 68% are interested in more payment capabilities, 52% want mobile banking capabilities, 50% want data security or account fraud protection, 37% want loyalty or reward offerings and 13% want financial account analytics.

As CUs increase their investments in innovative products and enhance existing offerings, they will appeal to the members who want access to digital payments, lower their exposure to the risk of member churn and better position themselves to maintain relationships with account holders.

As CUs increase their investments in innovative products and enhance existing offerings, they will appeal to the members who want access to digital payments, lower their exposure to the risk of member churn and better position themselves to maintain relationships with account holders.