![]()

It is no longer enough for credit unions (CUs) to compete with banks within the regions in which they operate. They must now be ready to go toe to toe with digitally savvy financial institutions (FIs) and FinTechs that can offer services accessible anywhere and across any channel. Roughly half of CU members also bank with other FIs, even though many want to do all of their banking with a single institution. More than one-third of CU members would be at least “somewhat” open to leaving their CUs for FIs that offer all the financial products they need, with more than half of millennial members saying this.

CUs that lack digital-first services and innovations must work to change that — fast. Some are losing ground as primary FIs, and member satisfaction has also dipped in recent years alongside the CU market share for auto and personal loans. Easy access to a physical banking touch point is also important for consumers, and 55% choose their FIs based, at least in part, on the convenience of a nearby branch. CU members also tend to be more community-focused in their FI choices and are more likely than other FI customers to look at factors such as teller helpfulness and an institution’s community involvement.

Innovating digital-first banking products, meeting members’ expectations for payment options such as digital wallets and investing in solutions that reinforce CUs’ reputations for personalization are all significant contributors to their success. This month, PYMNTS examines the strategies and opportunities available to CUs that can help them retain members and appeal to new ones in an increasingly digital world.

Payments as a Pathway to Primacy

Credit unions have increased their investments in some digital innovations , such as mobile wallets, in which 80% of CUs said they were investing in 2021 — up from 54% in 2018. During that same time period, the percentage of CUs investing in contactless cards doubled from 21% to 42%. Increased investment in digital options is not ubiquitous, though. Since 2018, the percentage of CUs investing in peer-to-peer (P2P) payments has shrunk from 40% to 4%.

, such as mobile wallets, in which 80% of CUs said they were investing in 2021 — up from 54% in 2018. During that same time period, the percentage of CUs investing in contactless cards doubled from 21% to 42%. Increased investment in digital options is not ubiquitous, though. Since 2018, the percentage of CUs investing in peer-to-peer (P2P) payments has shrunk from 40% to 4%.

Developing digital payment options that draw members back into the financial fold will be vital in helping CUs solidify their positions as members’ primary or sole FIs. Payments account for 80% of consumers’ interactions with their FIs, and 88% of CU members already engage with digital products through an FI — though not always with their CU. CUs are working hard to respond to that demand, however, and around twice as many are investing in contactless cards compared to the share that did so in 2020.

As FIs pivoted to digital channels during the pandemic, CUs faced the challenge of maintaining the personal touch and service that is often a main selling point for members. Social distancing limited the face-to-face interactions for which CUs are typically known, but technology opened numerous avenues for CUs to still offer personalized services. Digital self-service options based on data and analytics can enable CUs to reinforce members’ sense of individualized attention.

Technology investments can also play a crucial role in helping credit unions maintain personalization. For example, interactive teller machines (ITMs) offer services that once were solely the domain of in-person branches — such as money orders or bill payments — and they also provide video call capabilities that link members with employees. CUs can also leverage online and mobile app tools to offer video banking services. These products can augment the digital banking experience, enabling CU members to experience the personalization of face-to-face interactions without stepping foot into branches.

New hardware and software are not the only technologies allowing CUs to innovate. They can also harness digital-first banking practices to encourage loyalty and gain business with targeted products, such as banking solutions for teenagers and young adults that combine mobile banking with financial education. Business banking products, meanwhile, can improve back-office efficiency and give CUs another revenue stream.

Credit Unions Plan for the Future

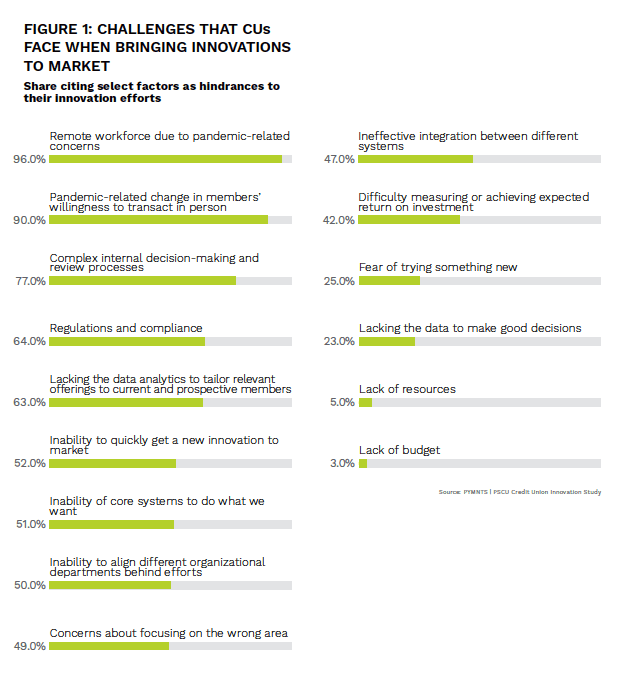

There are encouraging signs that CUs ’ digitization efforts are shaping up. One report projects that just 15% of CUs had yet to unveil digital transformation strategies by the end of 2021, while approximately one-quarter of all banks said the same. CUs are making progress despite rapid and sweeping market changes, laborious bureaucratic processes and inadequate technical resources, and 80% of members agree that their CUs have successfully implemented innovations.

’ digitization efforts are shaping up. One report projects that just 15% of CUs had yet to unveil digital transformation strategies by the end of 2021, while approximately one-quarter of all banks said the same. CUs are making progress despite rapid and sweeping market changes, laborious bureaucratic processes and inadequate technical resources, and 80% of members agree that their CUs have successfully implemented innovations.

Overall, CUs have primarily focused on innovating in loyalty and rewards, security and authentication, customized product offerings and planning and budgeting tools. In fact, 98% of CUs have invested in loyalty and rewards programs in the past year.

Regardless of these efforts, experts in the space agree that most CUs lag behind their peers in innovation. Getting on track with the transformations occurring in the banking sector will require CUs to make significant digital strides, from investments in technology to complete infrastructure rebuilds. CUs will need to take an honest look at the digital experiences they offer and work to eliminate friction points, putting digital architecture in place to consolidate and leverage their data to give members the services and products they want.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More