Credit unions are meeting the needs of members, especially younger ones, by leveraging technology and an array of modern tools.

These efforts have been strikingly successful so far, with a survey finding that 77% of Americans who use CUs to handle their primary financial needs are the most satisfied with the service compared to users of other financial institution (FI) types. Notably, consumers between the ages of 18 and 26 are the most likely age group to prefer CUs, at 24%.

This is not the end of the story, however. Although CUs have done a good job at meeting member needs, they must keep innovating on new technologies. The financial services landscape is rapidly changing, and members of all ages have an insatiable desire to use the latest digital solutions and tools. CUs need to adopt a policy of perpetual innovation to keep up, and technology is key to these efforts.

Innovation Is Needed to Retain and Attract Members

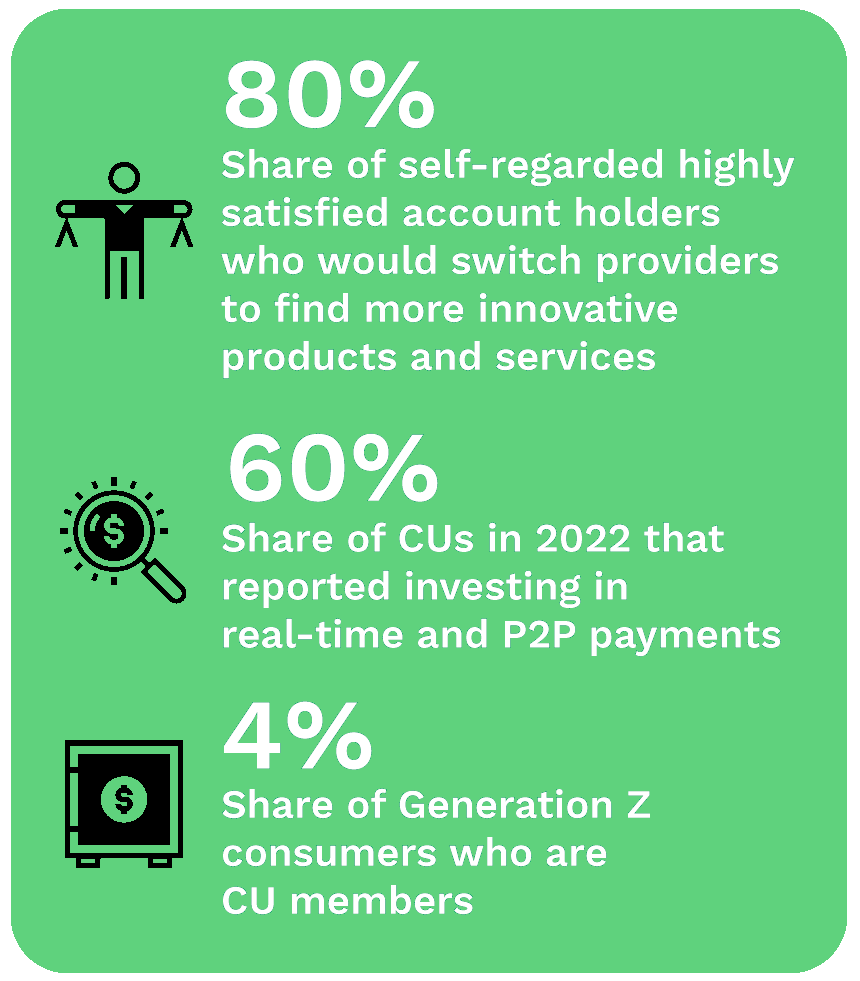

Continued innovation is important to retaining current members. More than 80% of self-identified highly satisfied financial account holders would be open to switching to another provider in search of more innovative solutions and services, according to PYMNTS research. CUs must also keep innovating to attract new members, especially younger demographics, as only 5% of millennials and 4% of Generation Z are CU members.

This is why CUs are actively working on expanding their product and service offerings. In 2022, for example, PYMNTS found that 60% of CUs reported investing in innovations such as real-time and peer-to-peer (P2P) payments, up from approximately 50% in 2021. Such investments will help CUs appeal to Gen Zers and millennials, as 41% of the former and 31% of the latter said mobile payments are an area of interest when it comes to their primary FIs’ potential innovations.

CUs are also working to improve their mobile banking offerings. Among CUs that PYMNTS classified as early launchers — companies at the forefront of technological innovation — 83% were investing in mobile banking, up from 74% in 2021. Such investments are essential because younger members are quite interested in using mobile banking to handle their financial needs. According to a survey, only 6% of Gen Z preferred to visit a physical branch, while the majority elected to use mobile options.

CUs Should Innovate Lending to Meet Young Members’ Needs

CUs can also use technology to meet members’ lending needs and improve product offerings. This is important because 26% of CU members reported being highly likely to borrow from a lender that is not their FI based on the favorability of loan terms, according to a PYMNTS survey. The same survey found that younger members were even more likely to switch, possibly due to these demographics’ higher debt burdens.

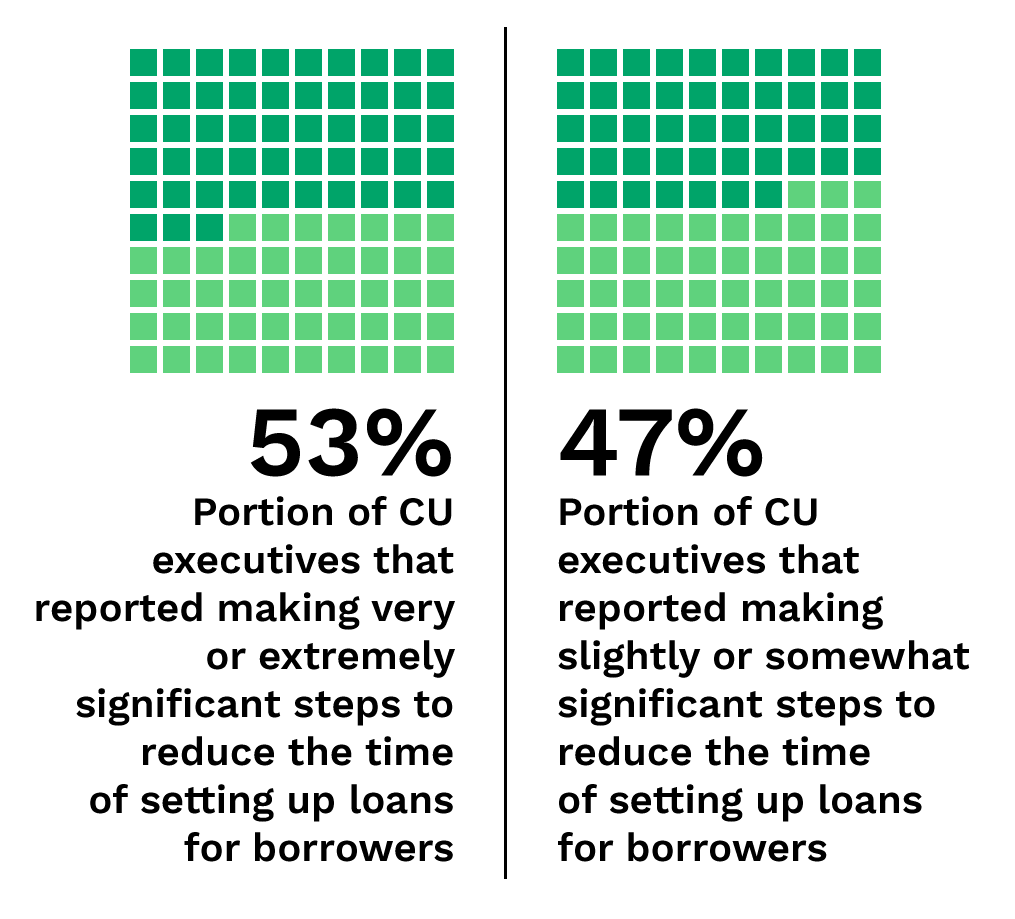

It is no surprise, then, that CUs are heavily investing in their lending capabilities. According to PYMNTS, for example, 53% of CU executives reported making highly significant efforts to reduce the onboarding time for prospective borrowers, while the remaining share of executives characterized their efforts as slightly or somewhat significant.