This month, PYMNTS examines the difficulties small- to medium-sized businesses (SMBs) face when making B2B cross-border payments, the solutions businesses are leveraging to address these pain points and how these innovations increase the range of products, services and payment methods available to businesses.

Difficulties of Cross-Border Payments

As with B2B payments in general, efforts to modernize and speed up the B2B cross-border payment experience have lagged behind similar efforts to improve the online payment experience for consumers, resulting in a cross-border payments process that is often complicated and filled with friction. For many businesses, the cross-border payment process is prohibitively complex. SMBs are particularly hard hit, with 27% ranking the complexity of making cross-border payments as one of their top obstacles.

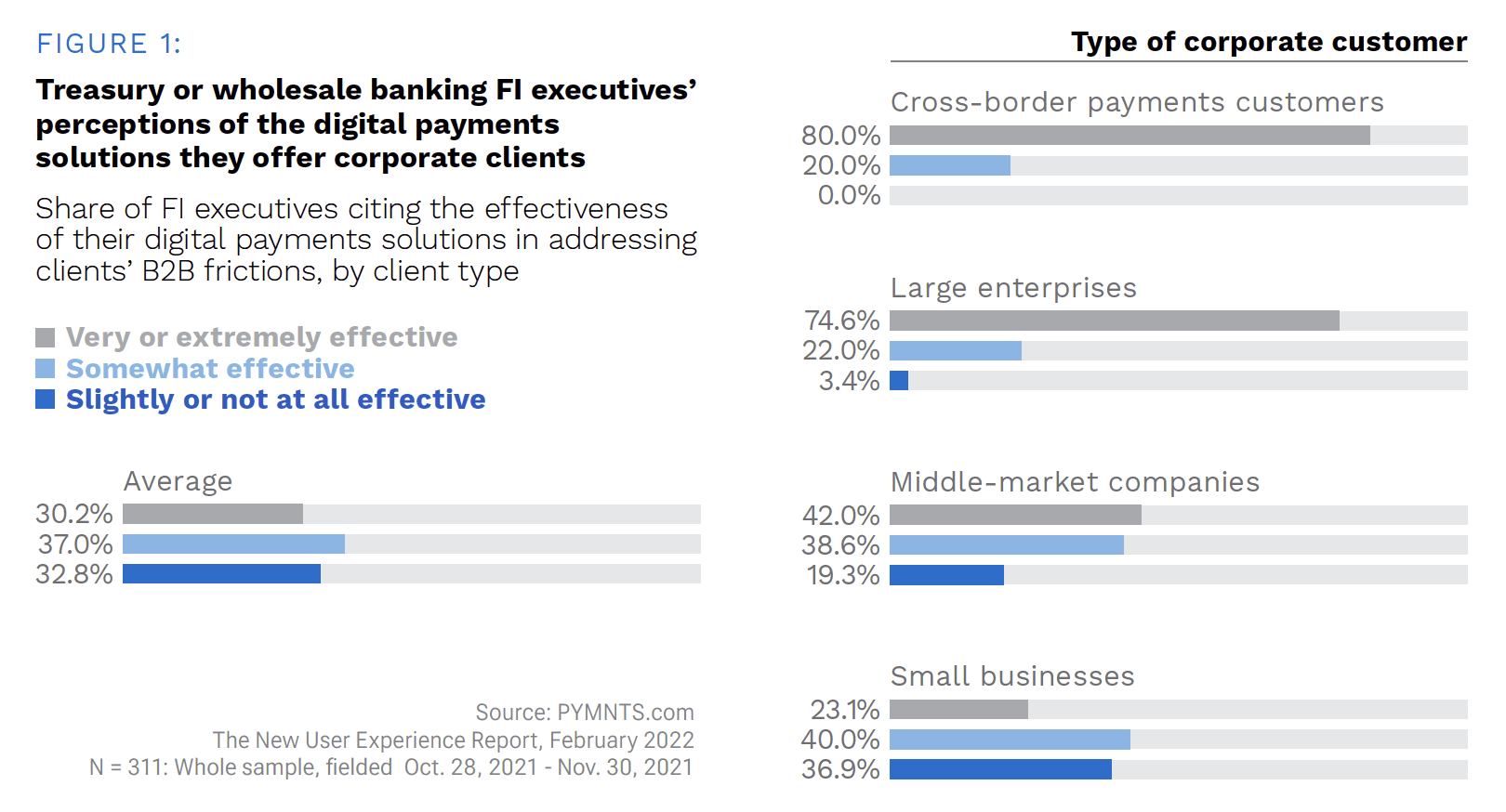

Data from a PYMNTS survey shows that the perception among financial institutions (FI) executives on their digital payment solutions is less positive as the size of the client decreases. For large enterprises, 74% of respondents were very or extremely satisfied with the solutions offered, while this percentage dropped to 23% for small businesses. It is also worth noting that for cross-border payments, around 80% of respondents said they were very satisfied with their solutions, despite the challenges for this type of payment.

Another difficulty in cross-border payments revolves around interoperability and application programming interfaces (APIs). To make payments across borders, information must be shared across different payment networks and systems. APIs are one of the best ways to accomplish this communication, which is why a striking 65% of payment operators currently use APIs and another 20% plan to. API or no API, however, networks and systems can communicate with each other only if they are interoperable.This means they must share the same protocols, formats and other aspects that allow a message from one network to be understood by the other. At present, there is a distinct lack of interoperability and standardization, with only 38% of payment system operators reporting the existence of domestic standards for APIs. Nearly eight in 10 payment operators view this lack of standardization as the biggest barrier to API adoption. Without this adoption, cross-border payments will remain challenging.

Solutions to the Rescue

According to PYMNTS’ data, the most common solution FIs currently provide to reduce B2B payments friction is automated account validation, so FIs not currently offering this product should consider doing so. Faster or real-time payment functionality should be another consideration. The ideal cross-border digital solution should be easy to use and provide customers with important details such as transparent exchange rates and payment delivery dates.

If FIs can provide the right solutions, businesses will benefit in a variety of ways. For example, 64% of United States SMBs view reduced fraud risk as the biggest benefit of cross-border payments innovation. PYMNTS’ data also shows that 56% of overall U.S. businesses view enhanced cash management capabilities as a benefit of cross-border payment solutions. They also believe innovation would reduce errors, improve accounts receivable (AR) efficiency and provide access to a range of new products and services. With all these benefits, it is no surprise that business customers are increasingly seeking cross-border payments solutions. It is now up to FIs to provide them.