In particular, open banking is boosting consumer payouts. According to PYMNTS Intelligence, 42% of consumers primarily receive payouts directly to their bank accounts, whether from merchants, service providers or government agencies. Open banking enables these customers to link their bank accounts directly using their existing logins and receive funds immediately. However, close to half of consumers still receive payouts without a connectivity tool.

These are some of the key insights drawn from “How Open Banking Can Provide Fast and Easy Consumer Payouts,” a PYMNTS Intelligence and Trustly collaboration, examining how consumers currently receive payouts.

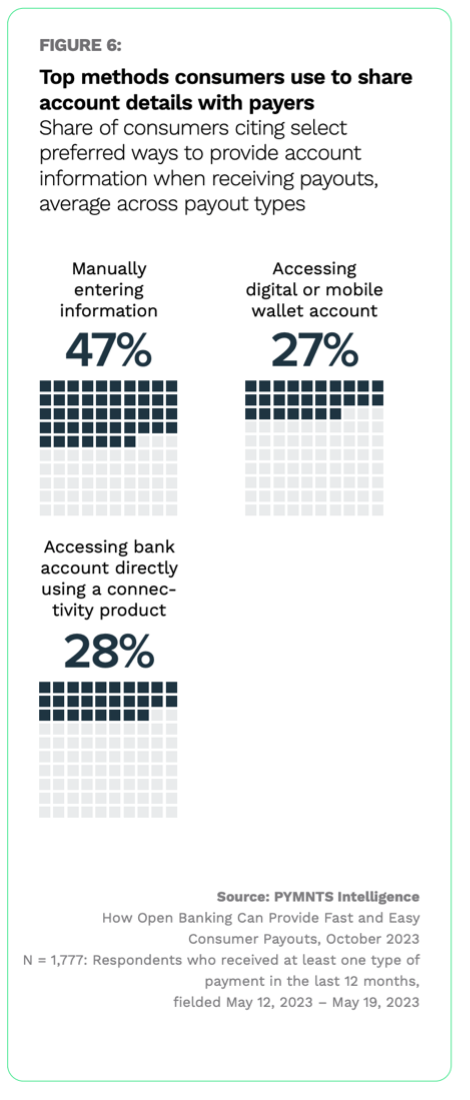

A Preference for Manual Data Entry

Consumers receive payouts in a variety of ways. Direct-to-bank transfer is the most common way consumers get disbursements from public institutions, while checks are most often used for insurance claims payouts, and third-party apps are popular for receiving gaming winnings.

Despite the availability of open banking, almost half of consumers surveyed choose to enter their banking information manually on a website to receive payouts and prefer to continue doing so. Conversely, only slightly more than one-quarter prefer accessing their bank account via a connectivity tool. Consumers who opt for this alternative cite security, ease and convenience as the main reasons to do so.

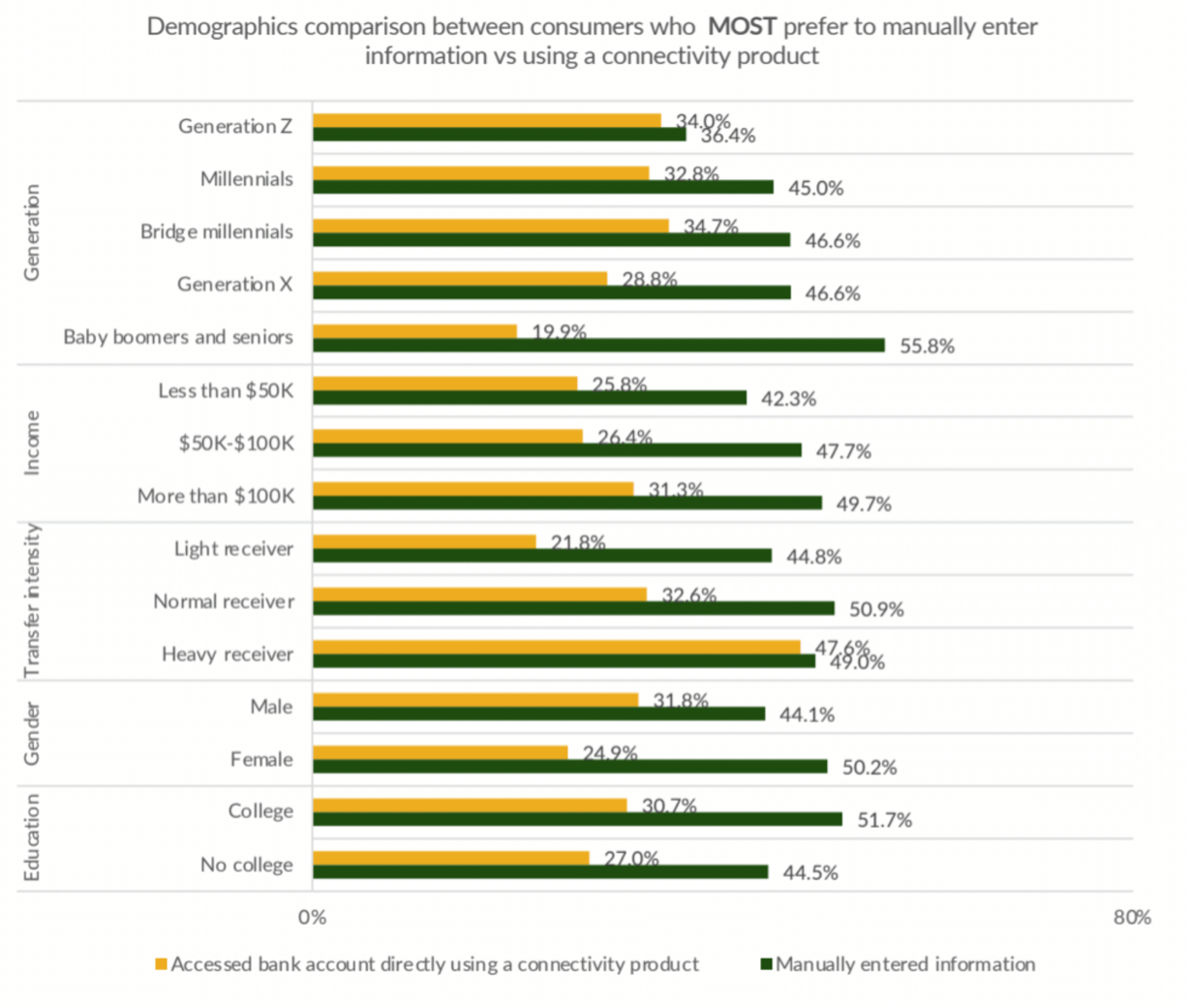

An Opportunity for Connectivity

The gap between preferring to enter information manually and through a connectivity product narrows notably for younger age groups.

Per the study, 56% of baby boomers and seniors prefer manually entering information, compared to 20% who prefer to use a connectivity product, a difference of 36 percentage points. For Generation Z, however, this gap is only 2 percentage points, and it is less than 8 points for millennials, with both generations favoring manual data entry.

Additionally, heavy receivers — those receiving over 50 payouts per year — also exhibit a very small gap (only 1 percentage point), with roughly 48% preferring using a connectivity tool for receiving payouts.

The study also found that frequent receivers and younger consumers prefer directly accessing their bank account using a third-party connectivity app to receive payouts, citing speed, security and convenience. Based on this data, these tech-friendly consumers are typically more comfortable connecting payouts directly to their bank accounts to receive quick and easy transfers.

That connectivity products are more popular with these demographics means that merchants and service providers could benefit if they offer real-time payouts with enhanced connectivity features to stand out in a crowded landscape.