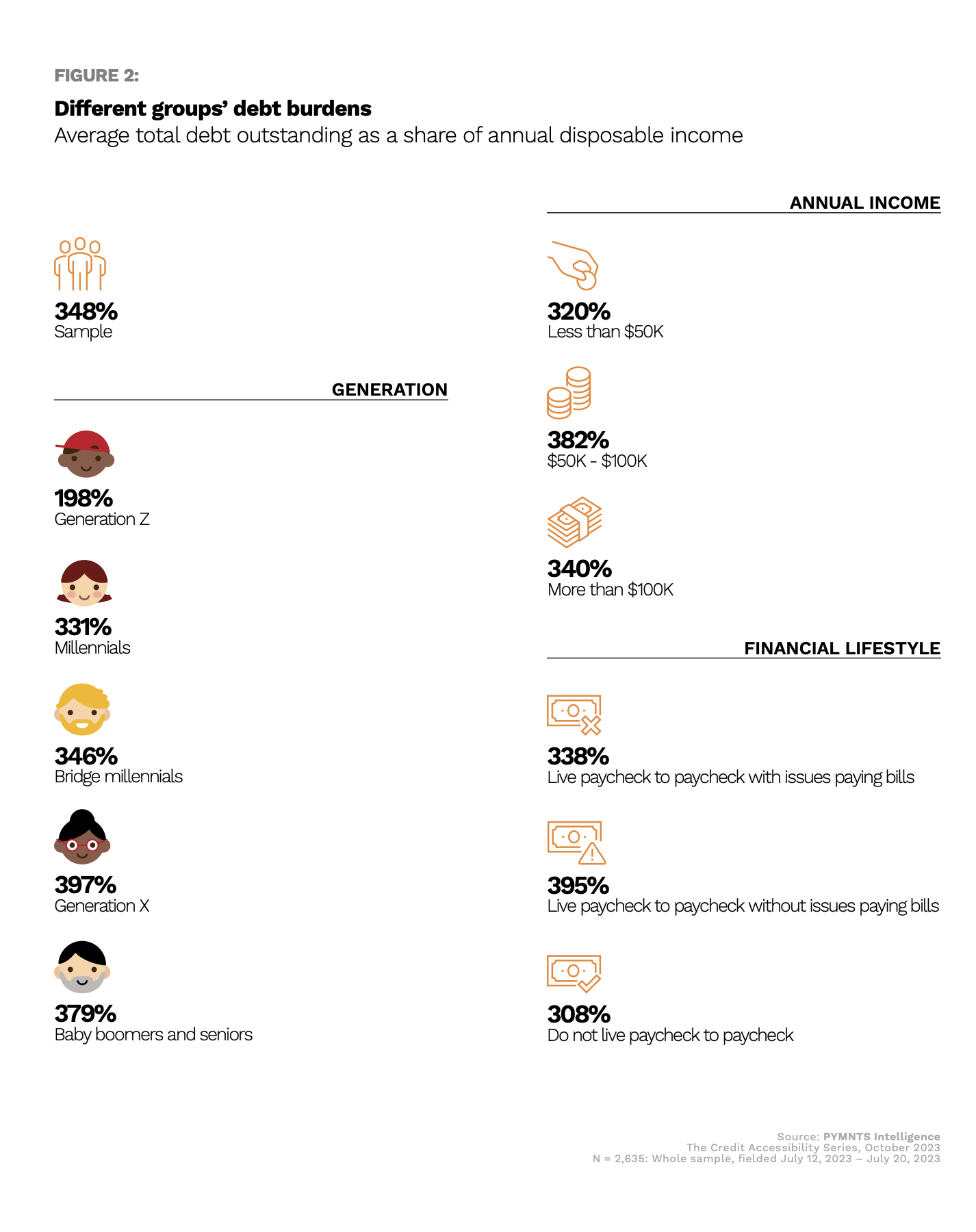

Of all generations, there’s one that has more debt than the rest: Generation X.

A Generation X consumer must work, on average, almost four full years to pay off all outstanding debts, compared to 3.3 years for millennials and two years for Gen Z, the youngest generation, and slightly more than baby boomers and seniors.

Born between the early 1960s and early 1980s, most Gen X consumers have a home mortgage, own a car they pay for in installments, among other consumer loans, and have had several credit cards for years, making this the most indebted generation. Nevertheless, their high income level and relative financial stability make them an attractive segment for certain credit products.

About the Numbers

These are some of the key data and insights drawn from “The Credit Accessibility Series: Economic Malaise Exacerbating U.S. Consumer Debt Levels,” a PYMNTS Intelligence and Sezzle research collaboration that explores the characteristics, sentiments and behaviors of consumers’ debt personas divided by generation, as well as the debt impact on credit accessibility, livelihoods and purchasing power.

How Gen X Manages Debt

On average, each Gen X individual holds a debt burden equivalent to 3.97 years of annual disposable income. By disposable income, we mean the total amount of income an individual has available to cover living expenses, make savings or invest. This includes all wages, bonuses, dividends and other sources of income after deducting taxes and other mandatory contributions.

Despite holding the highest level of debt, Gen Xers do not need to use bank overdrafts as much as other age groups. According to other PYMNTS research, the share of Gen X consumers who attempted a transaction without sufficient funds in the last 12 months before being surveyed was 15%, the second lowest portion among all generations, just lagging baby boomers and seniors. This is because this group, being a mature age in terms of professional development and income generation, owns more financial resources than others.

Likewise, the generation’s specific housing situation reflects similar findings. As illustrated in separate PYMNTS Intelligence research, this age cohort holds the largest share of mortgages, with 45%, compared to 32% of millennials.

Whether it is because of accumulated personal loans or because they have larger mortgages than other generations, 43% of consumers from this generation with low credit scores experienced difficulties or were unable to afford bills due to their lack of credit, a portion that is in line with the overall average. When facing bank overdrafts, credit cards are, for them, the most used product if funds are not available.