The latest installment of PYMNTS’ generational mini-series deep dives into Generation X’s digital habits and behavior.

Gen X, born between 1965 and 1980, are used to being caught in the middle. Sandwiched between the more marketed-to baby boomers and millennials, this generation is now caught another way. With the potential of caring for both children and aging parents, Gen X has been most affected by inflation’s pressures.

This sense of being in the middle may also be reflected in the generation’s digital innovation adoption and other behaviors, which sometimes lean toward the attitudes of baby boomers and seniors and other times lean toward younger cohorts. We analyzed five of PYMNTS’ key research themes — healthcare, finances, payment preferences, food and banking security — in order to form a top-down view of how Gen X interacts with the larger ConnectedEconomy™.

Healthcare: Gen X’s preferred channels fall nearly exactly in line with overall surveyed sample size when paying for healthcare, with no strong favor or particular disinterest in these methods. Over one-third pay in person at a physician’s office or hospital, with 27% opting to use a digital portal. Gen X consumers pay for healthcare by mail only 17% of the time, the lowest across generations. Gen X pays more like baby boomers and seniors. Of the age cohort surveyed, 35% opt for a debit card, their most popular method (and just behind baby boomers and seniors’ 37% use for the same). Mostly paying for routine visits in full, 7% have set up a payment plan, although that number rises to 44% for surprise bills. Nearly in line with younger generations, 46% of Gen X spends more on healthcare than they can afford. This could be due to the financial strain from potentially supporting both children and older relatives.

Payment Preferences: Gen X’s digital payment preferences share the same seeming indifference as seen with healthcare channels. Of those surveyed, half have used a new payment method over the past year. Mobile wallets are seen somewhat more favorably, as 48% believe the innovation can replace some physical wallet features, the most of across generations. Another 38% believe mobile wallets can replace most physical wallet features, leaning toward younger age cohorts who feel the same. Although 78% have used at least one mobile wallet feature, more than four in 10 said the digital innovation is less safe than using a physical wallet for the same purposes. This ambivalence mirrors the same overall indifference seen with healthcare preferences, with no strong opinions noted either way.

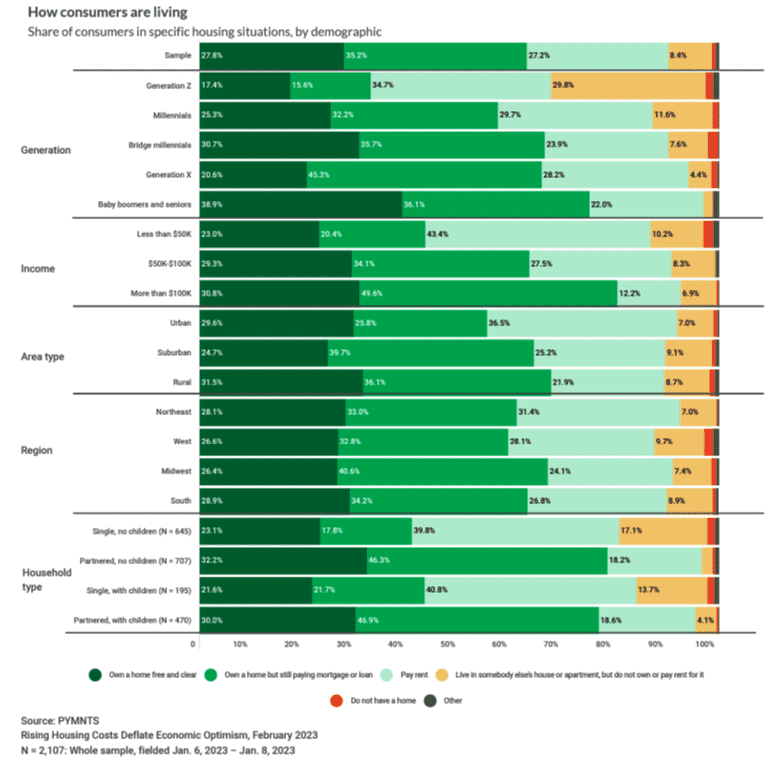

Finances: Gen X has been most affected by inflation, perhaps due to their doubled parent and caretaker duties. The generation has the highest share (37%) of consumers whose ability to save decreased year over year. As 43% said they are their household’s main breadwinner, inflation has put Gen X in a precarious position. The generation’s specific housing situation reflects similar findings, as illustrated in PYMNTS’ February “Consumer Inflation Sentiment Report,” which found the age cohort holding the largest share of both mortgage and rental payments.

Food: To combat inflation, 36% of surveyed Gen X’ers simply eat out less often, although when they do 14% of the generation prefer menus with lower-priced items. This generation’s tipping behavior lies between bookended generations, with nearly all tipping for tableside service, but only 50% of those surveyed tipping at QSRs, compared to 36% of boomers and 61% of bridge millennials. Similarly, 35% have reduced the amount they tip as a result of inflation, compared to 20% of boomers and 55% of bridge millennials. Perhaps reflecting Gen X consumers’ financial difficulties, 30% of those surveyed have traded down both quality and quantity of food items to deal with rising grocery prices. This is the highest share across generations.

Banking Security: Gen X is mostly content with current banking practices. Less than half say they would switch primary financial institutions for an improved digital or mobile experience. Additionally, 36% of the generation surveyed said they strongly agree that their bank provides the highest level of security, with another 47% agreeing with the statement. Nonetheless, over one-quarter would like to see their bank provide more visible security measures.

Gen X, perhaps due to their “sandwiched” status, is experiencing the most difficulty in the current economic climate, if savings rates are any indication. It is difficult to determine if their marked indifference to digital innovations is due to the generation’s more pressing financial concerns or an extension of their stereotypical apathy. As they may potentially care for both children and older adults, any enthusiasm as part of the ConnectedEconomy™ may have been put to the side.