And it seems we might add another certainty: inflation.

By now, the worldwide spike in inflation is rounding its second year.

And a three-day weekend, right now, seems a brief respite to fire up the grill, but we cannot stop thinking about how much everything costs.

The simple fact is that we’re learning to live with inflation. Grudgingly, with difficulty in many ways — and yet, with some resignation.

The latest official data on consumer expectations as to where we are and what inflation might look like showed that expectations for inflation are less than sanguine.

Although the general expectations, per recent consumer sentiment surveys, are that inflation will be north of 3% in the months ahead, which would be a strong decline from the peak of 9% seen a year ago, the damage has already been done.

PYMNTS data showed that 72% of consumers said their income has not kept up with inflation — or at best has barely kept up with it. As many as 4 in 10 employed consumers said their current salary does not meet their expectations.

PYMNTS reported over the summer that 83% of individuals said there is at least some reason to be concerned about what lies ahead because prices are rising, and 46% said that it’s getting harder to keep up with monthly bills and obligations.

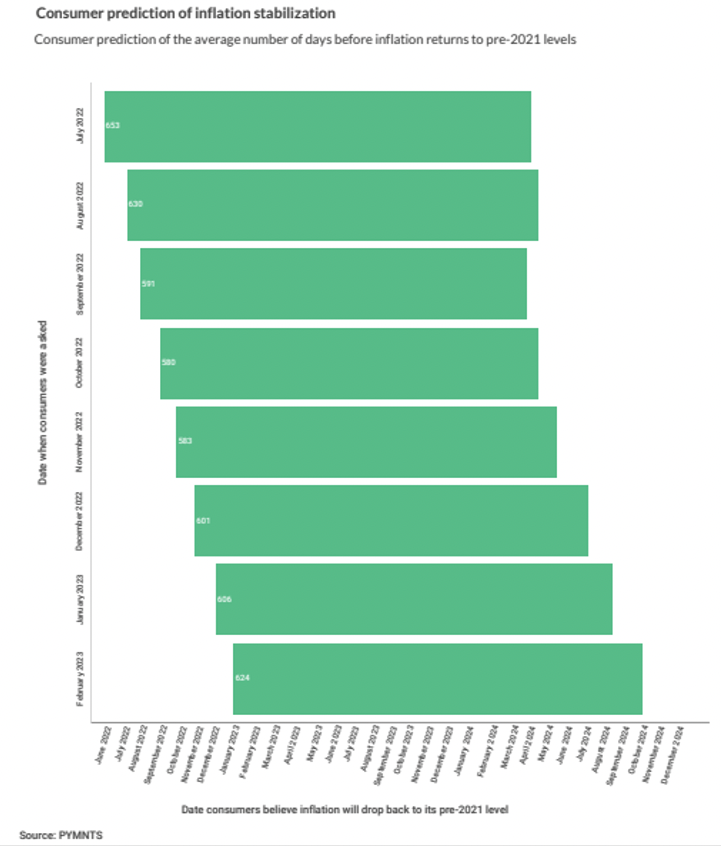

As for girding for the long haul, coming into 2023, PYMNTS found that by and large, individuals did not — and do not — see inflation returning to early 2021 levels for years to come.

How We Cope

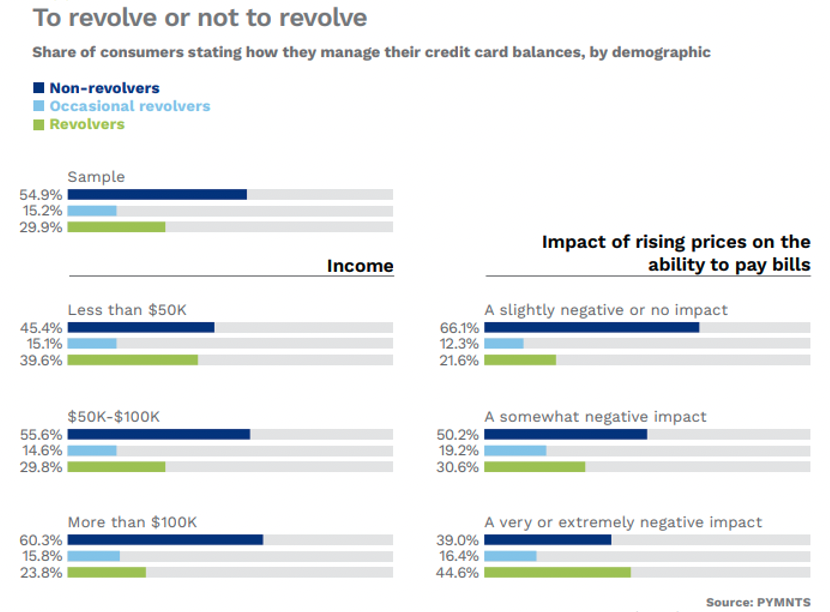

To plug the gaps between what comes in the door (wages) and what goes out to pay for it all, consumers are turning, increasingly, to credit cards to keep things going.

In the report “Credit Card Use During Economic Turbulence,” a PYMNTS and Elan Credit Card collaboration, data showed that 33% of card holders, on average, increased their reliance on credit cards in the last six months, and 15%, on average, decreased that spending. Forty-five percent of card holders carried balances and revolved their obligations, which in turn cut into discretionary spending.

We’re coping, too, by cutting back on nonessential purchases. As many as three-quarters of consumers have cut back on nonessential expenses. About 68% of all consumers have cut down on nonessential grocery shopping; 74% did the same for retail purchases. And nearly half of consumers seek deals as they comparison shop across any number of categories.

The road back to normalcy is long, and inflation’s decline to more palatable levels lies over the horizon — yet to be revealed.