Budget-focused FinTechs and innovative financial institutions (FIs) may have a golden opportunity to meet consumer need.

The Federal Reserve released its latest monthly snapshot of the U.S. economy March 10, and consumers’ ability to save seems grim. While the personal savings rate went up from 4.5% in December to 4.7% in January, it remains at about half the pre-pandemic rate of nearly 9%.

While the side-by-side statistics are stark, the news itself may not be a surprise. Consumers’ emergency reserves are dwindling and 401(k) holders are increasingly dipping into their accounts to pay bills. PYMNTS’ latest collaboration with LendingClub, “New Reality Check: The Paycheck-to-Paycheck Report,” reflects similar findings.

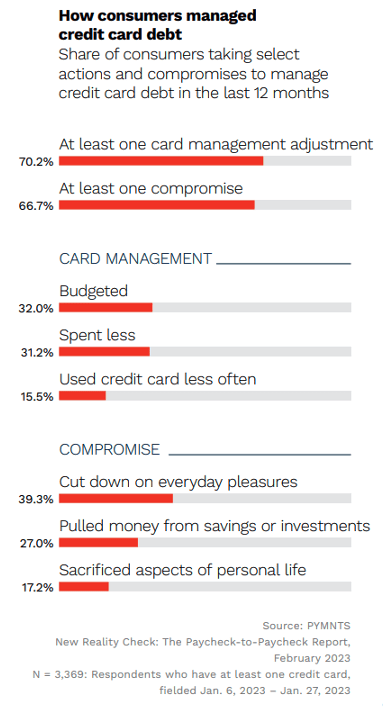

As emergency expenses and other unexpected bills threaten consumers’ savings, 27% of surveyed consumers overall have pulled from savings or investments to pay down their credit cards. Clearly, the current situation is unsustainable. However, while the economy gets sorted, there is also a clear need for consumers who are struggling to get all the assistance they can.

This is where budget focused FinTechs and innovative FIs may step in. Card-issuing banks have a multi-pronged opportunity to assist customers on a path to financial wellness and possibly cut down on delinquencies by offering innovative tools such as payment method recommendations. Broadly based on customer transaction data, payment recommendation tools put that information through algorithms to create personalized advice. The advice might include such options as identifying the best card to use, a merchant-specific deal or other beneficial options such as interest-free buy now, pay later (BNPL) plans.

These programs may be particularly well-received by consumers living paycheck to paycheck, as this segment is three times more likely than others to carry higher balances and revolve their monthly debt. Offering these tools and programs may also increase retention rates, as PYMNTS’ research suggests that customers are hungry for financial innovations.

Digital-first banks that provide consumer assistance tools and programs could gain customer loyalty, especially if they continue to offer savings accounts with higher interest rates than traditional banks. PYMNTS’ research shows 25% of consumers would switch from their current bank for better interest rates, and coupling these offerings with advice and assistance may spur savings-conscious consumers to make the jump.

Some FinTechs are already offering a variety of digital financial wellness tools aimed at assisting customers with a better view of their transactional habits. These include the ability to view current spending habit snapshots, tag purchases to categorize into budget lines and explore historical spending data and trends.

In line with these efforts, Cash App earlier this year launched a feature assisting consumers with their savings. Aimed at first-time savers, Cash App Savings lets customers set savings goals and keep a separate savings balance. The announcement came on the heels BNPL giant Klarna adding Money Story, a financial planning tool, to its app. In an animated format familiar to social media users, the tool provides insights and aims to promote smart spending habits.

The end of high inflation seems increasingly remote, and consumer pain may last longer than expected. FinTechs and FIs may not be able to put more money in consumer pockets, but perhaps they can help customers find better ways to budget.