According to Goldman Sachs research, as reported by the Wall Street Journal, U.S. households have spent 35% of the “extra” $2.7 trillion in savings accumulated while the pandemic raged, and by the end of the year, that drawdown will have reached 65%. Inflation has forced many of us to dip into savings accounts to offset the loss of purchasing power. The pressures are apparent in the statistics that in 2020, consumers saved nearly 17% of their disposable income. The most recent percentage, as we noted here, was 3.4%.

In the meantime, the savings consumers have on hand, as tracked by PYMNTS, shows a steady downtrend.

It’s a pain point for the paycheck-to-paycheck economy (which, by now, envelops nearly two-thirds of us).

Spending More than We Take In

At the end of last year, joint research from PYMNTS and LendingClub showed that an estimated 31 million — or 12% — of U.S. consumers spent more than they earned in the six months prior to October 2022.

Drill down a bit, and we see the ability to make up for that shortfall has become increasingly out of reach.

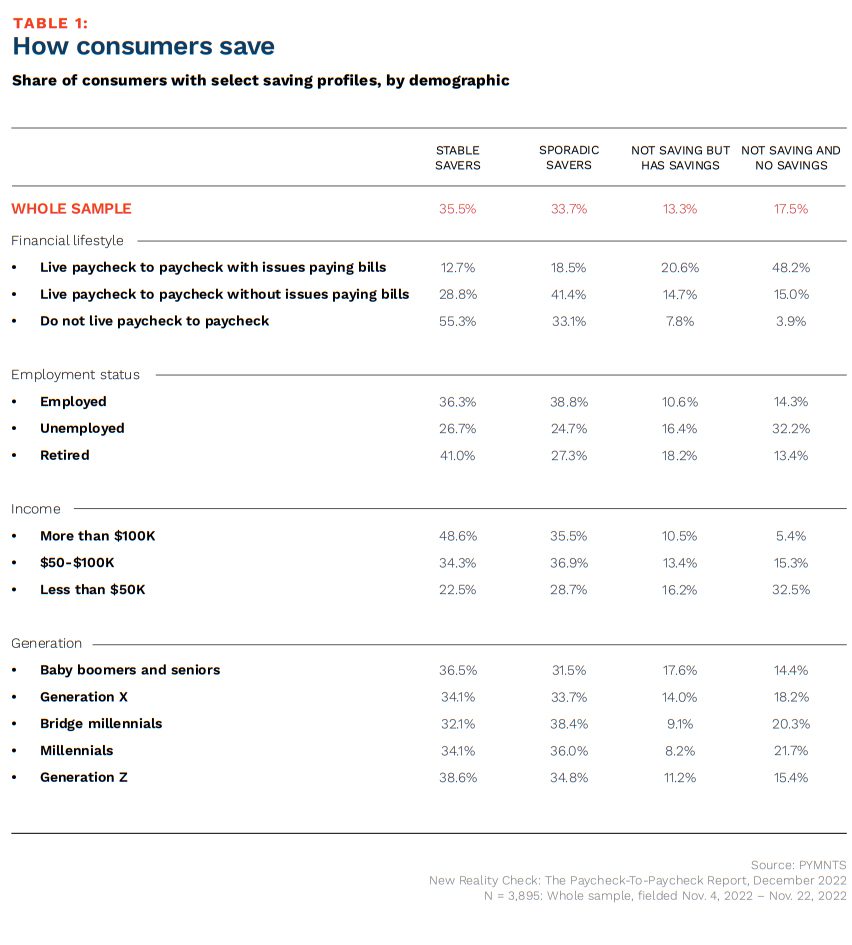

The paycheck-to-paycheck consumers are half as likely to be stable savers and seven times more likely to have neither savings nor saving capacity than those not living paycheck to paycheck.

The data also shows that there are exogenous shocks in the mix that make it hard to pad savings. About 65% of paycheck-to-paycheck consumers have experienced a financially stressful event in the past three years.

Those unexpected events can be cataclysmic to financial well-being, including job loss or a medical emergency. In a world where half of the paycheck-to-paycheck consumers say their salary only covers basic expenses and they can’t afford to save money, the negative ripple effects can be long term.

The chart below shows that 48% of those living paycheck to paycheck with issues paying bills have no savings and cannot save. A third of those who take home $50,000 annually are in that cohort. And at a high level, 17.5% of all respondents have no savings and are not saving.

There are 13.3% who are not saving but have some savings — and we note the stats above show that those savings will likely be drawn down over the coming months.

As to the dollar amounts coming into the new year that were in the proverbial coffers: Consumers living paycheck to paycheck with issues paying bills reported having savings of $2,460, on average, in November 2022. This is nearly one-third of the average savings held by those living paycheck to paycheck without issues ($7,200).

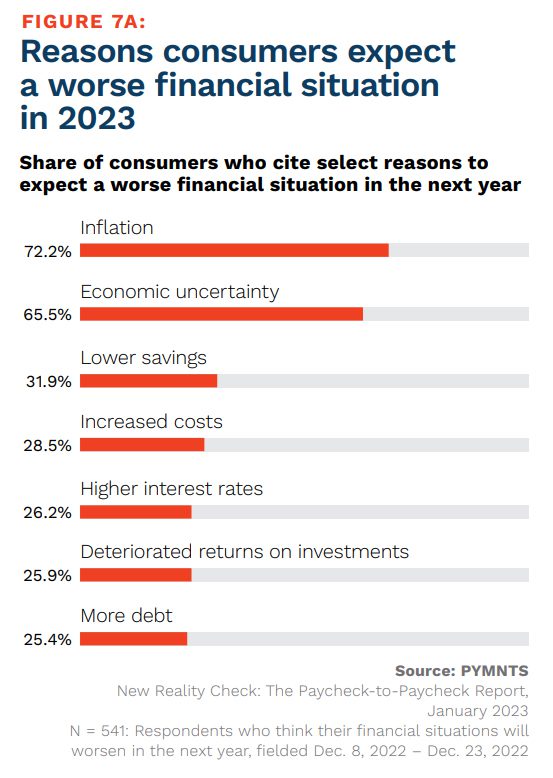

In the January 2023 iteration of the Paycheck to Paycheck report, more than a quarter of U.S. consumers said they expect their financial situations to worsen in the current year. Inflation is the most pressing reason for that outlook, while nearly 32% see lower savings on the horizon.

The most obvious way to alleviate some of the pressures lies in throttling spending.

The latest readings show that only a minority of consumers expect to make significant purchases this year. Among paycheck-to-paycheck consumers, regardless of whether they struggle to pay their monthly bills, 30% plan to spend on leisure travel.

Only about 22% of those living without difficulty and 29% of those struggling said they would purchase expensive electronics or appliances. A relatively anemic 20% of consumers in the middle-income bracket — those earning $50,000 to $100,000 annually — expect to spend money on “big-ticket” electronics, clothing or gifts in the months ahead.