With millions of Americans still struggling to access traditional credit options, achieving full financial inclusion will be neither quick nor easy. With an estimated 307 million smartphone users in the U.S., however, the emergence of mobile technologies has created opportunities to expand credit access to underserved households.

FinTechs already are leveraging mobile technology to make credit more widely and easily available, helping those who would otherwise be forced to resort to payday loans and other expensive lending types. FinTechs are also empowering consumers to improve their credit profiles and thus broaden the types of services for which they can qualify.

FinTechs are helping subprime consumers improve credit scores

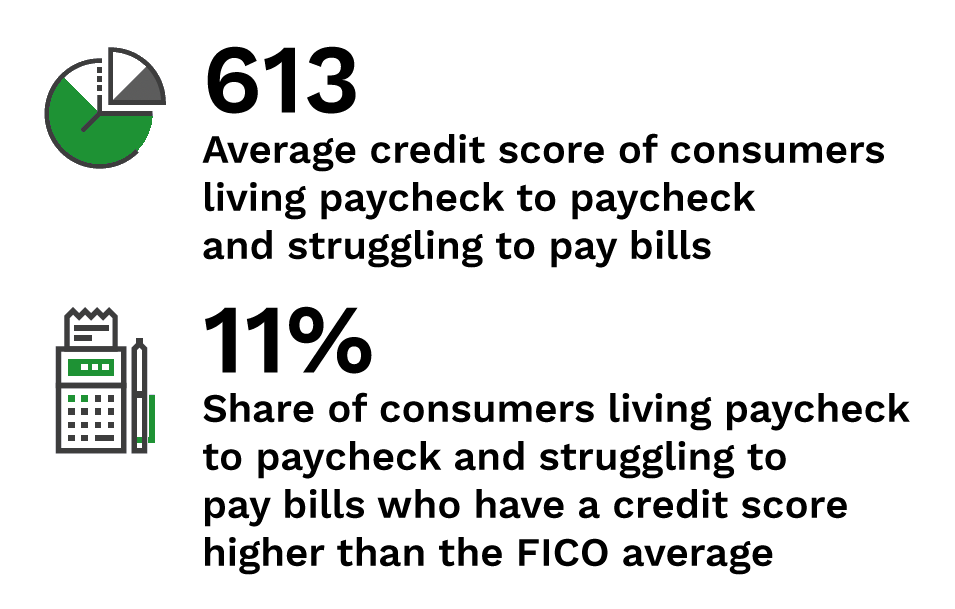

As FinTechs work to promote financial inclusion, there has been a major focus on addressing the role of bad credit scores. PYMNTS found that consumers who live paycheck to paycheck and are struggling to pay their monthly bills have a below-average credit score of 613, making them subprime borrowers and thus largely unable to access normal credit products.

The impact of poor credit scores on credit access is especially conspicuous among younger consumers. As recently as Q2 2022, for example, millennials’ average credit score was nearly 30 points below the national average, limiting their ability to qualify for traditional credit options. Indeed, while 25% of Americans were denied a credit card in the past year, that share rose to 36% among millennials.

The products that underserved populations can access, such as prepaid cards and payday loans, do not typically count toward credit-score calculations, so it can be a challenge for these consumers to improve their credit profiles. To solve this problem, many FinTechs are offering ways for consumers to boost their credit scores, mainly by considering payments that had not traditionally been counted toward credit profiles. The Jay-Z-backed FinTech Altro, for example, is helping people build credit scores when they make recurring payments to services such as Netflix and Spotify. Other FinTechs are working to provide customers with financial education resources and tools to keep tabs on their scores.

BNPL can help underserved consumers access affordable credit

FinTechs are also providing more affordable and convenient lending options, with buy now, pay later (BNPL) services as a prime example. Unlike payday loans and other nontraditional lending types, BNPL services typically have low interest rates, and unlike traditional bank credit products, they are available to consumers with weak credit profiles.

FinTechs are also providing more affordable and convenient lending options, with buy now, pay later (BNPL) services as a prime example. Unlike payday loans and other nontraditional lending types, BNPL services typically have low interest rates, and unlike traditional bank credit products, they are available to consumers with weak credit profiles.

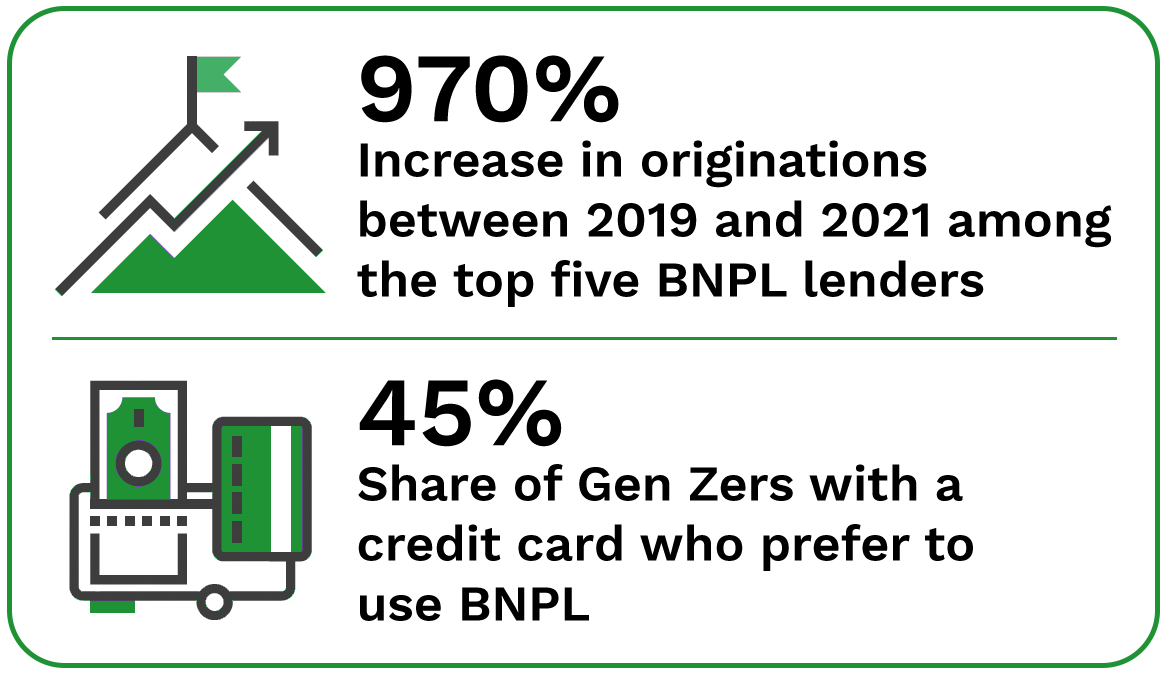

As a result, BNPL has become immensely popular. By the summer of 2022, the share of adults reporting use of a BNPL service at least once in the last month had not dropped below 14% in the previous year. This lending type is especially popular among younger consumers, to the extent that 45% of Gen Zers with a credit card prefer to use BNPL.