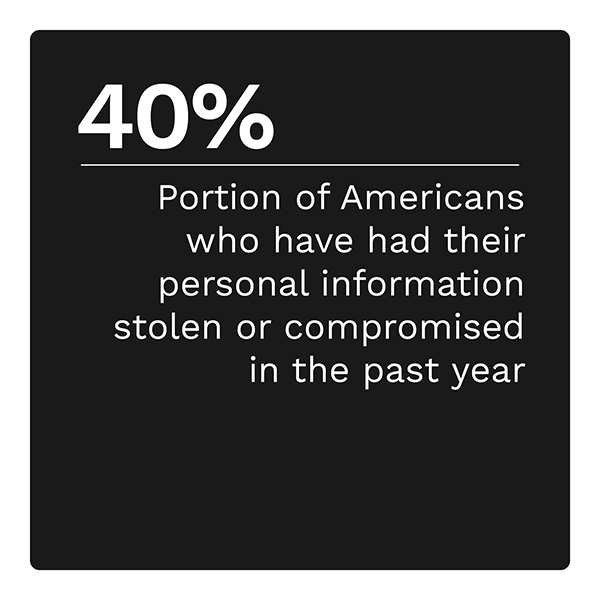

A substantial number of Americans can expect to experience digital fraud at least once in their lifetime. A recent study found that bad actors have stolen or compromised the personal information of four in 10 individuals in the past year. Fifty-one percent of these victims lost personal funds when fraudsters compromised their accounts, and half said these bad actors had targeted them more than once.

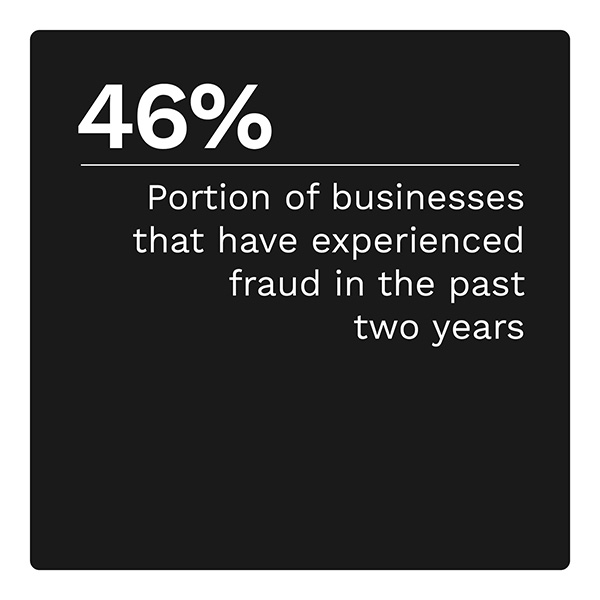

Fraud’s impact on banks and other financial organizations mirrors its effect on consumers. Forty-six percent of organizations in a recent survey said they had experienced fraud in the past two years. Among organizations annually generating more than $10 billion in revenue, 52% experienced fraud. One in five of these organizations said the fraud attacks cost them more than $50 million.

The “Digital-First Banking Tracker®” examines the evolving threat of digital fraud targeting FIs and how banks can leverage cutting-edge technology to protect themselves and their customers.

Around the Digital-First Banking Space

A recent PYMNTS survey found consumers are aware of fraud risks and generally trust banks to keep them safe. More than 58% of consumers said they would entrust their primary banks with vaulting their payment credentials. Smaller shares expressed confidence in payment providers or eCommerce merchants such as PayPal, Amazon or Apple to do the same.

Identity fraud is a particularly dangerous threat to the banking sector. A recent study found that last year’s median loss per bank clocked in at $310,000. Nearly one-third of banks lost $497,000 or more during the same time, while FinTechs lost a median of just $120,000. The median across all surveyed sectors, including aviation, technology, telecommunications and financial services, was $240,000.

Identity fraud is a particularly dangerous threat to the banking sector. A recent study found that last year’s median loss per bank clocked in at $310,000. Nearly one-third of banks lost $497,000 or more during the same time, while FinTechs lost a median of just $120,000. The median across all surveyed sectors, including aviation, technology, telecommunications and financial services, was $240,000.

For more on these and other stories, visit the Tracker’s News and Trends section.

An Insider Explains How the Fraud Threat Continues to Evolve

Fraud is a constant threat for banks, with the Federal Trade Commission reporting that fraud costs consumers nearly $8.8 billion in 2022. This cost is a 30% increase from the year prior. The increasing trend of online commerce has made the fraud threat worse. Bad actors have adopted new techniques to take advantage of the evolving landscape. As customers shift their banking and shopping methods, bad actors do the same to exploit insecurities in whichever method is most popular or vulnerable.

To learn more about the shifting bank fraud portfolio, read the Tracker’s Insider POV.

The Best Anti-Fraud Solutions for Banks and Their Customers

Fraud’s cost goes far beyond the actual amount stolen. A recent study found that every dollar lost to fraud costs FIs approximately $4.36. Moreover, this represents just directly-related expenses such as legal fees and recovery. The true cost of fraud, considering lost customer loyalty, is likely incalculable. Fraud-fighting solutions may be expensive, but they more than pay their freight when considering this cost.

To learn more about these fraud prevention solutions, read the Tracker’s PYMNTS Intelligence.

About the Tracker

The “Digital-First Banking Tracker®,” a collaboration with NCR, examines the evolving threat of digital fraud targeting FIs and how banks can leverage cutting-edge technology to protect themselves and their customers from cybercrime.