The rise of digital banking and faster digital payment methods has brought about increasingly sophisticated fraud and financial crime.

Against that backdrop, financial institutions (FIs) have had to elevate their systems and processes to combat the growth in fraudulent transactions and resulting financial losses.

According to PYMNTS Intelligence, based on a survey of 200 executives at the largest banks in the U.S., fraud has increased for 43% of FIs compared to 2022, with the average cost of fraud increasing by 65% for FIs with assets of $5 billion or more.

Misuse of account information remains the leading source of fraud, accounting for 38% of fraudulent transactions. Notably, digital wallets like Samsung Pay, Google Pay and Apple Pay, as well as same-day automated clearing house (ACH) and regular ACH payments, have also seen significant increases in fraud rates since 2022.

Overall, FIs face various challenges when combating fraud, including data breaches, increased payment speed and complex regulatory requirements. Per the study, the share of FIs citing data breaches and the increased speed of payments as their top challenges rose significantly in 2023 compared to 2022 figures.

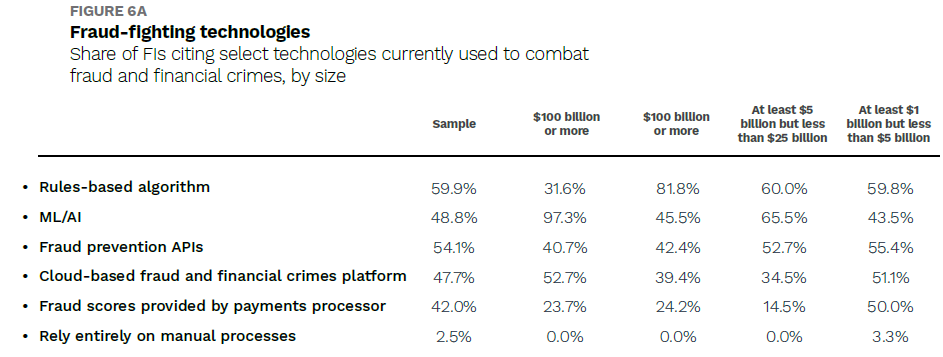

To address this growing threat, banks are ramping up investments and deployments of machine learning (ML) and artificial intelligence (AI) technologies to combat fraud in the next year, and rather than outsourcing fraud detection and protection, they are moving to develop solutions in-house.

And for those that have taken the plunge, it seems to be working.

FIs are already utilizing AI and ML technologies to combat fraud report lower rates of fraudulent transactions and are less likely to experience an overall increase in fraud rates compared to those not utilizing these technologies, making the move all the more worthwhile.

In terms of benefits, AI and ML technologies play a crucial role in helping FIs identify and assess the types of fraud they commonly encounter, not to mention the ability to gain a standardized and holistic picture of fraud. Additionally, FIs can also enhance user authentication protocols and improve efforts to identify unauthorized users earlier with the assistance of these advanced technologies, further keeping scammers at bay.

But banks can’t do it alone, and payment giants are stepping in to lend a helping alone.

In July, Mastercard announced that it had teamed with nine British banks to fight fraud via AI using large-scale payments data to spot real-time payment scams before money leaves the victims’ accounts.

“Organized criminals move ‘scammed’ funds through a series of ‘mule’ accounts to disguise them,” the company said at the time. “To counter this, for the past five years Mastercard has worked with U.K. banks to follow the flow of funds through these accounts, and then close them down.”

The payments giant also noted a rise in impersonation tactics by scammers in the face of increased payments and banking security. This aligns with findings detailed in the PYMNTS Intelligence study, which shows that fraud losses from impersonator scams — think fraudsters posing as bank technicians or the IRS — have doubled for large U.S. banks in 2023.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More