Credit offers consumers the flexibility to buy cars and houses and access college educations, yet data shows that 31% of U.S. consumers — about 80 million individuals — are on the outside looking in.

PYMNTS’ research finds that consumers fall into two categories: the credit secure, who can reliably access new lines of credit, and the credit insecure, who lack access, have fewer options to repair their finances and risk opting out of credit altogether.

Credit insecure consumers can be further divided into two personas: the credit marginalized, who credit providers have rejected at least once when applying for credit products in the past year, and the credit avoidant, who do not use credit products and have no interest in applying for any.

These are a few key findings in “How Credit Insecurity Is Changing U.S. Consumers’ Borrowing Habits,” a collaboration with Sezzle. This report is based on a survey of 2,678 consumers conducted from Feb. 22 to March 1 that assessed consumers’ access to credit, use of credit products and experience in applying for or being rejected for credit products, as well as the financial impact of life events and the alternatives available to them based on their credit access.

This is what we learned.

• Major life events can detrimentally impact personal finances, especially those of credit insecure consumers.

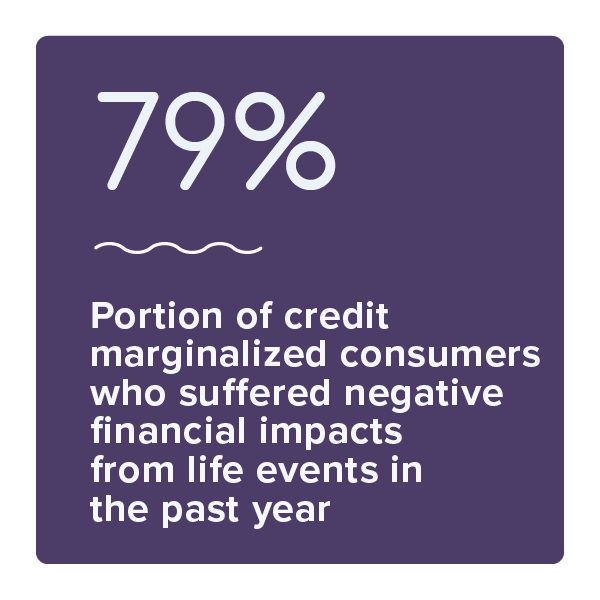

In the past year, major life events such as a change in employment, illness or death of a loved one have negatively impacted the finances of 79% of credit insecure consumers who credit providers have rejected. This correlation is not a coincidence. Consumers exist along a credit continuum, and one adverse life event could be enough to lead a consumer to become credit avoidant.

• Myriad concerns can cause credit marginalized consumers to become credit avoidant.

Even when facing financial hardships, concerns about making monthly payments can cause credit marginalized consumers to hesitate to apply for new credit products. Other significant reasons these consumers shy away from applying for new credit were low credit scores and fear of rejection. There is a risk of credit marginalized consumers becoming credit avoidant if they fail to find ways to improve their credit scores, potentially shrinking the addressable market for vendors of new credit products.

• Few consumers know how credit products such as BNPL can help improve their credit score.

Very few consumers in our survey were knowledgeable about how credit works. Judging by their responses to questions about whether nine different credit-related actions improved credit scores, more than two-thirds of consumers have a shaky understanding of the credit score system. We also found that few consumers understand how products like buy now, pay later (BNPL) can help them improve their credit scores.

Our key findings reveal that consumers exist along a credit continuum, and multiple factors can push consumers away from credit security. Those who believe they have no other choice may use predatory products, and credit providers have the opportunity to develop products that can help even more consumers become credit secure.

Download the report to learn more about how credit insecurity is affecting U.S. consumers’ credit access and borrowing habits.